Can Advanced Micro Devices AI Chips keep powering a data center rally just as Arm decides to crash the party?

How important is AMD in the AI chip cycle?

Advanced Micro Devices im KI-Chip-Investitionszyklus und neuer Konkurrenz durch Arm is increasingly a story about data centers and acceleration hardware rather than PCs. Most artificial intelligence development runs in massive cloud data centers, where clusters of GPUs, CPUs and high‑bandwidth memory train and serve large models. NVIDIA still dominates with roughly 80% share in AI accelerators, but AMD has steadily gained ground with its EPYC data center CPUs and Instinct GPU lineup, which now spans the MI300 and MI350 generations.

Demand for Advanced Micro Devices AI Chips is being driven by hyperscalers such as Meta, Microsoft and other cloud providers that need alternatives to NVIDIA for cost and supply reasons. Recent commentary across Wall Street points to accelerating data center revenue growth, with AMD’s AI server business now a primary driver of its top line. A recent analysis from The Globe and Mail highlighted strong uptake of EPYC and Instinct products among hyperscalers and on‑prem customers, even as it warned that the stock’s price‑to‑sales multiple screens as expensive compared with historical norms.

For U.S. investors, the key takeaway is that AMD is firmly embedded in the AI infrastructure stack alongside NVIDIA and Micron. The three names together account for a major weight in AI‑heavy semiconductor ETFs, meaning any broad AI hardware up‑cycle tends to pull AMD higher as capital flows into the sector.

What changes with Arm challenging AMD?

The competitive picture shifted again after Arm announced it will design and sell its own physical AI chips, targeting CPUs for AI data centers and projecting as much as $15 billion in annual revenue within five years. That move puts Arm in more direct competition with both Intel and AMD’s server CPU franchise. Rather than punishing incumbents immediately, the news initially lifted the whole chip complex, with Intel up more than 3% and AMD higher by over 1% as investors read the step‑up in AI chip ambitions as a validation of long‑term demand.

Still, Arm’s new strategy raises the stakes. Its plan to build an “AGI CPU” in collaboration with partners like Meta means the fight for AI data center sockets will only intensify. AMD’s EPYC platform today is a key x86 alternative to Intel’s Xeon, especially in cloud environments optimized for AI inference and agentic AI tasks that require fast, parallel CPU processing. If Arm can turn its dominant intellectual property in mobile and embedded markets into a credible server CPU, it could chip away at incremental growth that AMD is counting on.

That said, the AI compute market is so large and growing so fast that Arm’s entrance may expand the pie rather than simply stealing share. SoftBank, Arm’s majority owner, has emphasized that the addressable market is massive enough for multiple winners. For AMD, the priority remains execution: scaling Advanced Micro Devices AI Chips, securing long‑term supply through foundry partners like TSMC, and deepening customer relationships with hyperscalers and large enterprises.

Are Advanced Micro Devices AI Chips gaining real share?

Evidence continues to build that Advanced Micro Devices AI Chips are capturing incremental share, even if NVIDIA remains firmly in the lead. Reports from The Motley Fool and Seeking Alpha highlight growing deployments of AMD accelerators in cloud AI clusters and note that AMD is shifting from selling standalone chips toward full rack‑scale systems. That systems approach, with integrated CPUs, GPUs and networking, has helped secure wins with major AI players including OpenAI, Meta and Oracle, with broader deployments expected to ramp in the second half of 2026.

On the CPU side, AMD’s EPYC line has already eaten into Intel’s dominance over the last several years, especially in cloud workloads and high‑core‑count servers. The rise of agentic AI — systems that act on behalf of users with minimal oversight — increases parallel CPU needs, reinforcing the role of EPYC as a companion to both AMD and NVIDIA accelerators in data centers. As more AI agents and copilots run continuously in the background, the demand for both GPU and CPU capacity supports a multi‑year investment cycle in which AMD participates across several product categories.

Institutional investors are taking notice. Traders Union recently pointed to mixed but generally bullish technical momentum, with AMD trading above its 20‑ and 200‑day moving averages, even as it contends with resistance near the low‑$210s. At the same time, structured products like Royal Bank of Canada’s 17.1% coupon autocallable notes linked to AMD signal ongoing appetite for yield‑enhanced exposure tied to the stock’s volatility.

What’s the near-term setup for AMD stock?

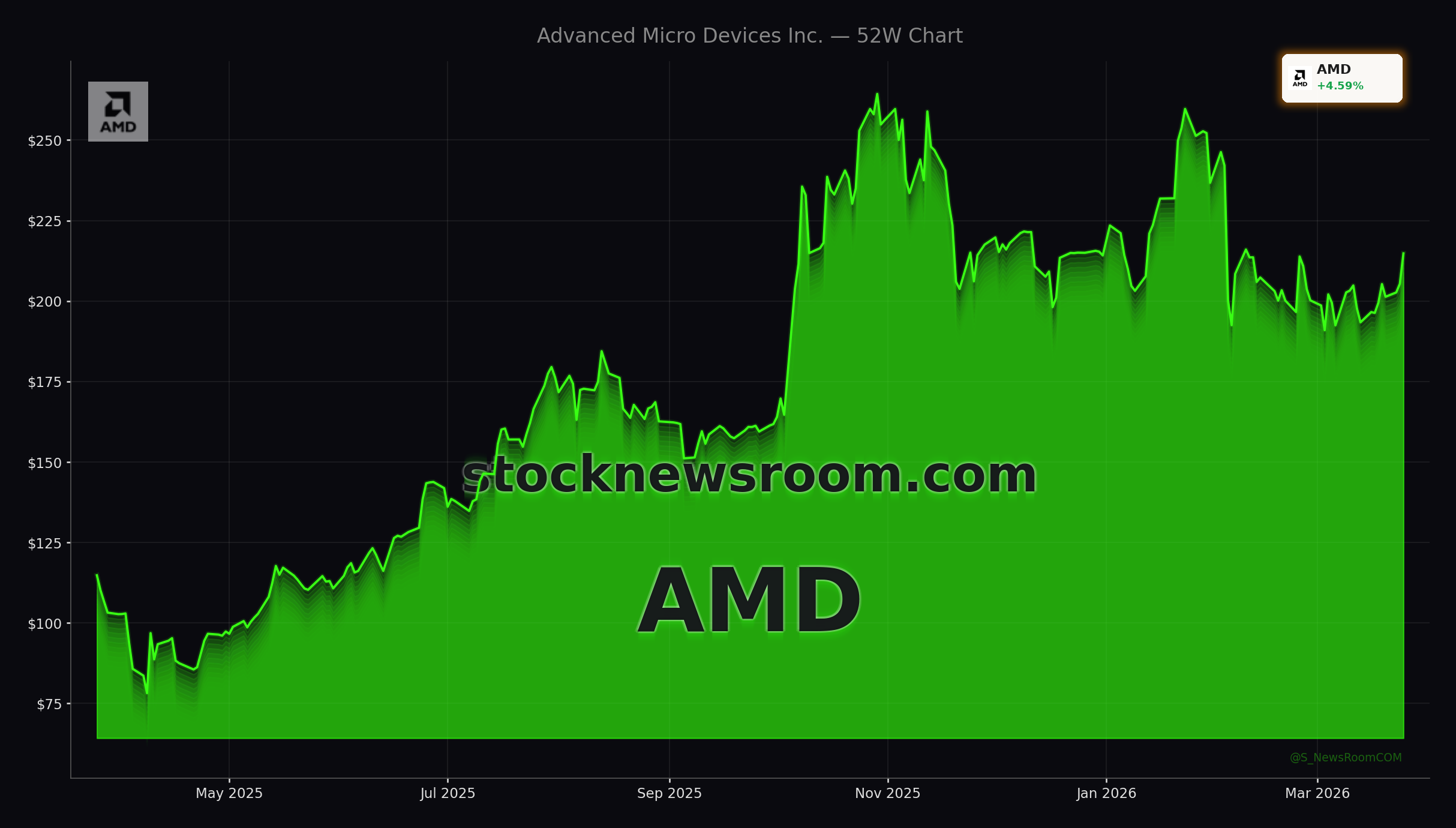

On Wednesday afternoon in New York, AMD shares trade around $218.85, up roughly 6.6% on the day and extending their rebound off recent lows near $189. Technically, reclaiming the 50‑day moving average after bouncing at the 200‑day has eased concerns about a potential “death cross” scenario, at least for now. Bulls are watching a gap in the chart around $219 and a prior swing high near $226.69 as the next upside markers, while a break back below recent lows could open room toward the $170 area.

Fundamentally, Wall Street remains split between enthusiasm over AMD’s 30%‑plus AI‑driven growth outlook and caution over valuation. Zacks Investment Research recently flagged AMD’s outperformance versus the broader market and ongoing data center strength, while also highlighting that the stock trades at a premium on key multiples. Other institutional holders, such as Salem Investment Counselors, have modestly trimmed positions but still treat AMD as a core long‑term AI holding.

Compared with megacap rivals like Apple or non‑AI cyclicals, AMD offers more direct leverage to the AI infrastructure story, but also higher volatility. Commentators at Insider Monkey and other outlets argue that if investors insist on owning a high‑beta AI underdog rather than NVIDIA, AMD may offer more upside than more mature semiconductor names like Broadcom.

Related Coverage

For a deeper dive into how big cloud customers could reshape AMD’s AI trajectory, readers can explore AMD AI Partnerships +1.7%: Can Deals Fuel an AI Surge?, which examines whether major collaborations with Meta and OpenAI can meaningfully close the gap with NVIDIA in next‑gen data centers. Investors interested in the broader tech and China exposure backdrop can also read PDD Earnings +7.9% Surge as Temu Faces Margin Warning, where we analyze how rising regulatory and margin pressures on e‑commerce platforms can ripple through high‑growth tech allocations.

Ultimately, Advanced Micro Devices AI Chips place the company near the heart of the global AI build‑out, with hyperscaler demand, rack‑scale systems and EPYC servers all pointing to sustained growth. For U.S. investors leaning into the AI hardware theme, AMD offers leveraged exposure with the added twist of new competition as Arm pushes into data center silicon. The next few quarters of deployment wins and AI spending trends will determine whether today’s premium valuation is justified, but AMD’s position in this investment cycle keeps it squarely on Wall Street’s radar.