Is Alphabet’s massive AI capex gamble setting up years of cloud dominance or the next big risk for investors?

How is Alphabet trading after the AI run?

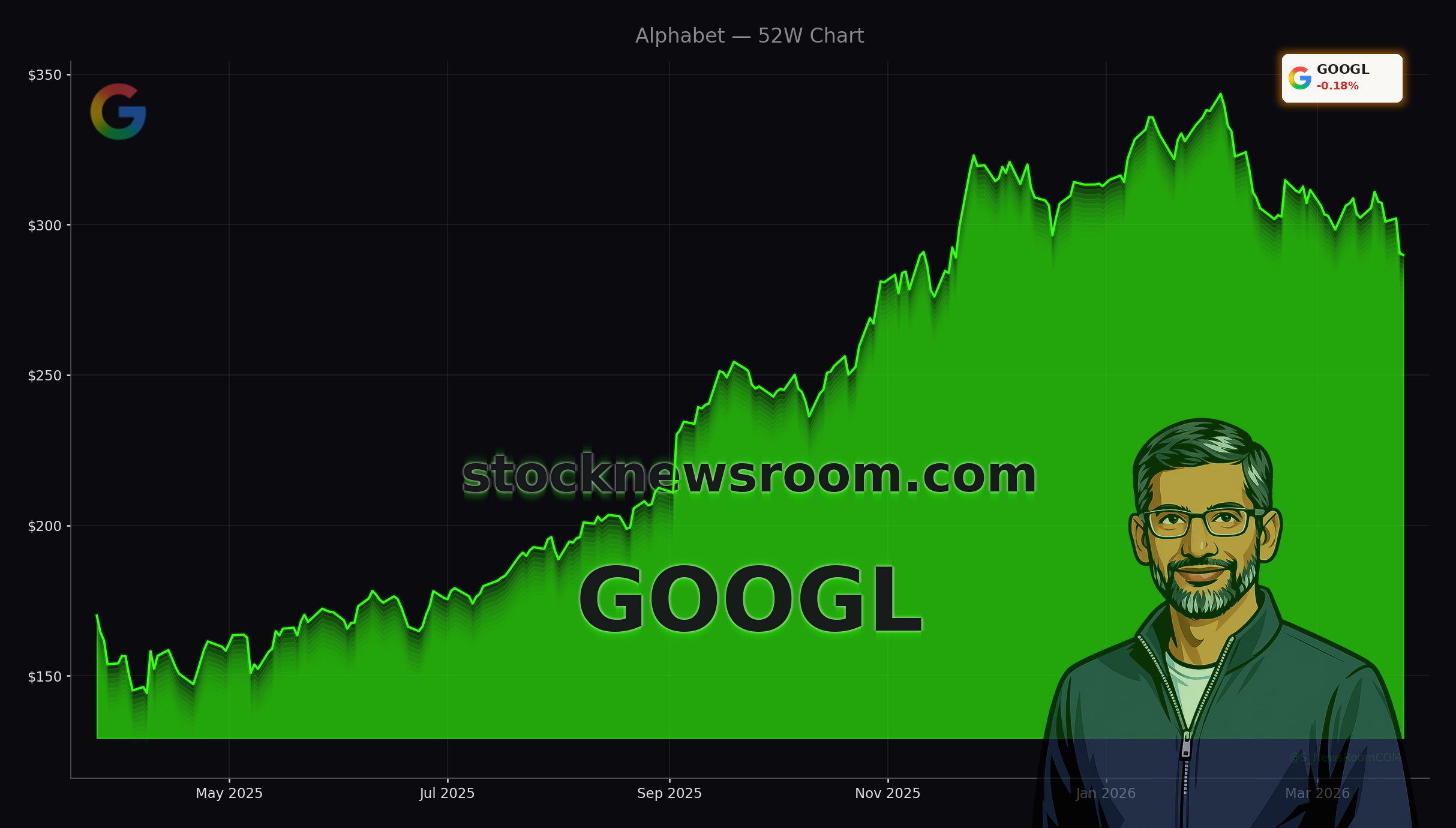

Alphabet Inc. (Google) continues to trade like a core AI blue chip, even after a sharp rally over the last 12 months. Class A shares are changing hands around $290.60, up a modest 0.06% on the day, while Class C GOOG shares sit at $288.52, down 0.24%. Both classes remain well below the 52‑week high near $349, giving Wall Street some breathing room after a gain of roughly 73%–76% over the past year highlighted by multiple institutional letters calling Alphabet a top contributor.

Despite a choppy start to 2026 for the “Magnificent 7,” Alphabet has crossed $400 billion in annual revenue for the first time, powered by core Search, YouTube and a resurgent Google Cloud. Several growth managers, including Renaissance Investment Management and RiverPark Advisors, cite Alphabet as a top holding tied directly to AI and cloud demand, arguing that at about 25x forward earnings it is one of the cheaper mega‑cap AI leaders alongside NVIDIA.

What defines the Alphabet AI Strategy now?

The Alphabet AI Strategy rests on building a fully integrated stack: custom chips, frontier models, global-scale infrastructure and massive consumer distribution. On the infrastructure side, management guided 2026 capital expenditures to an eye‑popping $175–$185 billion, nearly double the roughly $91 billion spent in 2025. That capex is aimed at expanding data centers, networking and tensor processing unit (TPU) capacity to support Gemini, Google Cloud and autonomous driving unit Waymo.

On the model layer, Gemini is now embedded across Search, Workspace and YouTube, with CEO Sundar Pichai pointing to over 10 billion tokens processed per minute via API and 750 million monthly active users on the Gemini app. Alphabet is also renting TPUs at scale, including a headline deal with Anthropic for access to one million chips built by TSMC, underscoring how the Alphabet AI Strategy positions the company as a core infrastructure partner rather than just a consumer platform.

Distribution remains Alphabet’s ace. Its Android ecosystem, Chrome browser, and default search deal with Apple give Google unmatched reach, while YouTube’s more than $60 billion in annual revenue and 325 million paid subscriptions provide a second AI monetization channel beyond search ads.

How big is TurboQuant for memory and cloud?

A new element of the Alphabet AI Strategy is TurboQuant, a Google Research algorithm that claims to cut AI memory requirements by as much as sixfold. This compression breakthrough rattled memory stocks midweek, with Micron Technology sliding as investors recalibrated expectations for long‑term AI-driven DRAM demand. MarketWatch and 24/7 Wall St. both flagged TurboQuant as a key reason why the recent memory rally is under pressure, as it could allow cloud customers to run large models with less high‑priced memory.

For Alphabet, TurboQuant is a competitive weapon. Lower memory requirements can reduce internal AI infrastructure costs, improve margins in Google Cloud, and make its TPUs more attractive versus GPU‑centric rivals. Q4 2025 numbers already showed Google Cloud growing 48% year over year to $17.66 billion with operating income more than doubling to $5.31 billion, after a growth cadence that accelerated from 28% to 48% over four quarters. If TurboQuant-driven efficiency lets Alphabet price AI training and inference more aggressively, the cloud unit could continue to win share from Amazon Web Services and Microsoft.

What risks are rising around AI and social platforms?

The bolder the Alphabet AI Strategy becomes, the more scrutiny it attracts. This week a Los Angeles jury found Google’s YouTube and Meta’s Instagram liable in a landmark youth social media addiction case, awarding a 20‑year‑old California woman $3 million in damages, with roughly 30% assigned to Google. Coverage from Reuters, Bloomberg Technology, CNET and Forbes framed the verdict as a potential template for thousands of similar lawsuits targeting addictive design, infinite scroll and algorithmic recommendations.

Financially, the award is trivial for a company worth about $3.5 trillion, and Alphabet stock barely moved on the news. Strategically, though, the case signals rising U.S. legal risk for recommendation engines that underpin YouTube and other ad businesses. Any forced design changes to reduce engagement could modestly weigh on ad revenue growth, even as AI-driven personalization has been a key tailwind. Regulators in Europe and the U.S. are also watching how AI models surface content to minors, adding another layer of potential friction for YouTube’s AI‑powered growth.

How are Wall Street and big investors reacting?

On Wall Street, sentiment around the Alphabet AI Strategy remains broadly constructive but more selective after the stock’s massive run. TradingKey highlighted a 3.33% single‑day drop in GOOG on March 25 tied to investor concerns over aggressive AI capex, cooler enthusiasm for the AI trade in early 2026, and ongoing regulatory uncertainty, even as fundamental profitability metrics remain among the strongest in the software and IT services sector.

Yet demand from professional investors is still robust. Brendan Caldwell, CEO of Caldwell Investment Management, named Alphabet among his top picks on BNN Bloomberg, emphasizing its AI and cloud leverage. Multiple growth and value funds report that Alphabet has been a top contributor since mid‑2025, when shares traded at a steep discount to the S&P 500 despite the company’s deep AI capabilities. Many see Alphabet, Amazon and Tesla as core positions for long-term exposure to the AI and automation cycle, with some arguing Alphabet is better diversified across ads, cloud and self‑driving than pure-play chip makers.

Related Coverage

Investors looking for a deeper dive into the capital-intensity of the Alphabet AI Strategy can explore how the company’s record $185 billion capex plan might reshape its balance between growth and risk in Alphabet AI Strategy Boom: Inside the $185B Bet Warning. For a sector‑wide view of how TurboQuant is reverberating through the memory supply chain and what it could mean for AI hardware suppliers like Micron, see Micron Earnings -3.5%: Record AI Boom Meets TurboQuant Shock, which examines whether the current AI memory upcycle can withstand compression-driven efficiency gains.

Overall, the Alphabet AI Strategy is shifting the company from a dominant search and ad platform into a full-stack AI infrastructure and applications powerhouse, backed by unprecedented capex and technical depth. For U.S. investors, the trade‑off is clear: near‑term free cash flow pressure and rising legal scrutiny versus the potential for Google Cloud, Gemini and TurboQuant to entrench Alphabet at the center of global AI workloads. The next earnings report on April 24 and management’s commentary on capex, cloud growth and regulatory risk will be critical in showing whether this strategy can keep powering both Silicon Valley’s innovation engine and long‑term portfolio returns.