Can the Alphabet AI Strategy turn heavy data-center spending into lasting earnings growth while rivals race to dominate the cloud?

Is Alphabet’s market pullback a buying chance?

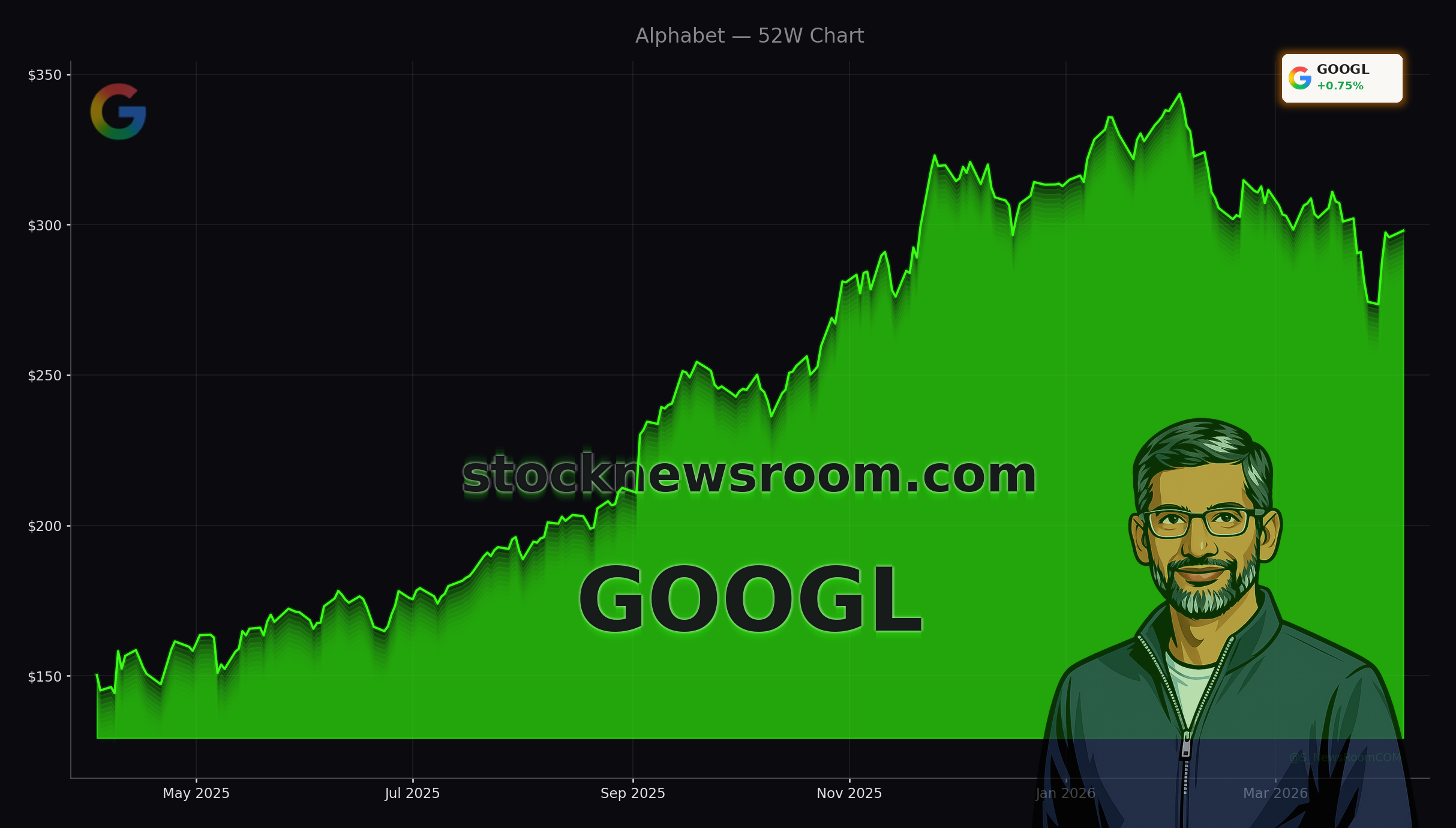

Alphabet Inc. Class A shares trade near $297.47, modestly above the prior close of $295.86, while Class C sits around $295.57. That’s roughly 20% below recent highs after a correction driven more by concerns over AI capex intensity than by deteriorating fundamentals. Recent quarters showed around 18% revenue growth, 31% EPS growth, and net margins above 30%, keeping Alphabet firmly among the most profitable names in the NASDAQ and S&P 500.

Institutional flows are mixed rather than outright bearish. Some managers like Cooper Investors and Clarius Group have trimmed positions, but large asset owners including Norges Bank and Berkshire Hathaway have increased stakes, leaving institutional ownership just above 40%. Technical analysts see the recent two down gaps as an overreaction and highlight a high statistical likelihood of a rebound toward the $300–$315 area in the near term, supported by solid earnings and accelerating cloud revenues.

For long-term US investors, the key question is whether the Alphabet AI Strategy can sustain double-digit earnings growth while funding an aggressive build‑out of data centers and custom silicon. Consensus S&P 500 earnings expectations run mid‑single digits; by contrast, Wall Street still models roughly 15% annual EPS growth for Alphabet through 2029, suggesting the stock could continue to outperform if that trajectory holds.

How is Google Search using AI offensively?

Just a year ago, many on Wall Street feared that ChatGPT-style agents could disrupt Google Search. Instead, the Alphabet AI Strategy has turned Gemini into a catalyst rather than a threat. Google has rolled out AI Overviews and an AI Mode in search, both powered by its Gemini models. Management reports higher search usage, and AI Mode queries are typically about three times longer than traditional text searches.

Longer, more conversational queries create more surface area for commercial answers, richer shopping units, and new ad formats. That is critical because advertising across Google properties still provides about 72% of Alphabet’s total revenue. Rather than cannibalizing this cash machine, generative AI is being embedded to deepen engagement and improve monetization. Strategists at Citizens and other Wall Street banks have recently reiterated constructive price targets for GOOGL, arguing that search remains a durable moat, not a melting ice cube.

The long‑term wildcard is regulatory risk. US and European antitrust authorities are scrutinizing search and digital ad practices, and AI‑driven personalization could invite fresh scrutiny. But for now the market appears more focused on growth and profitability than on worst‑case regulatory scenarios.

Why Google Cloud sits at the core of Alphabet AI Strategy

The most visible proof point for the Alphabet AI Strategy is Google Cloud. In Q4 2025, Google Cloud revenue surged 48% year over year to $17.7 billion, while the unit’s remaining performance obligations swelled to about $240 billion. That backlog gives multi‑year visibility that few cloud providers can match and positions Alphabet as the clear number‑three public cloud behind Microsoft Azure and Amazon Web Services.

Demand is coming from enterprises that want full‑stack AI solutions: Gemini models, managed data platforms, and specialized chips. Forrester recently ranked Google Cloud as the leading AI infrastructure provider, highlighting its breadth from training and inference to data governance. This is key for US portfolio managers who increasingly see Alphabet as a dual‑engine story: mature ad cash flows plus a high‑growth, higher‑margin cloud business.

On valuation, Alphabet trades at roughly 26–27 times forward earnings—only a modest premium to the S&P 500 despite its faster expected growth. Several sell‑side desks, including analysts cited by The Wall Street Journal, place their median price target near $385, implying about 30% upside from current levels if the cloud and AI thesis plays out.

Chips, partners and the fight with NVIDIA and Microsoft

A less appreciated pillar of the Alphabet AI Strategy is hardware. Alphabet’s tensor processing units (TPUs) started as internal accelerators but are now being commercialized across Google Cloud. High‑profile AI names such as Anthropic, Meta Platforms and OpenAI have signed deals to rent TPUs, and Meta is considering deploying them in its own data centers by 2027. Alphabet has also set up at least one joint venture with a large investment firm to expand TPU‑based cloud services, effectively monetizing its silicon R&D as a platform.

This puts Alphabet in a different strategic lane than NVIDIA, whose GPUs dominate merchant AI silicon, and more in line with hyperscaler peers like Microsoft and Amazon that are building custom accelerators to control costs and performance. Memory suppliers such as SK Hynix are reportedly negotiating multi‑year DDR5 contracts with both Microsoft and Google, underscoring just how capital‑intensive this AI build‑out will be—and how serious the big three cloud players are about securing supply.

Alphabet is also an important customer for chipmakers like Broadcom and is reportedly exploring advanced packaging options with Intel for next‑generation AI systems. Alongside these efforts, the company’s 2015 near‑$1 billion investment in SpaceX could become more visible when the space company eventually goes public, though even a large gain there would be relatively small versus Alphabet’s trillion‑dollar market cap.

Beyond core businesses, projects such as Waymo’s autonomous ride‑hailing and Google Quantum AI could evolve into additional growth legs later in the decade. For now, however, Wall Street is primarily valuing Alphabet on the strength of ads, cloud, and its AI technology stack.

Related Coverage

Investors who want to dive deeper into regulatory and chip‑related risks can read “Alphabet AI Strategy Warning: TPU Edge, SpaceX Upside and Legal Risk”, which explores whether Alphabet’s AI moat could invite tougher oversight. For a sector‑wide look at the memory side of the AI boom, “Micron Technology Outlook After Record Boom and TurboQuant Shock” examines how Google’s AI workloads are influencing demand trends at Micron and other chipmakers.

The Alphabet AI Strategy now rests on three pillars: defending and monetizing search with Gemini, scaling Google Cloud’s AI infrastructure, and leveraging custom chips and ecosystem partnerships to contain costs and drive performance. For US and global investors, that combination offers a compelling mix of growth and resilience, with valuation still below many mega‑cap peers. The next few quarters of cloud bookings, AI product rollouts and capex disclosures will show whether Alphabet can convert its ambitious roadmap into sustained shareholder returns.