Is Alphabet TurboQuant just another AI tweak, or the software shock that could upend chip demand and Google’s cost base?

How did Alphabet’s move hit Wall Street?

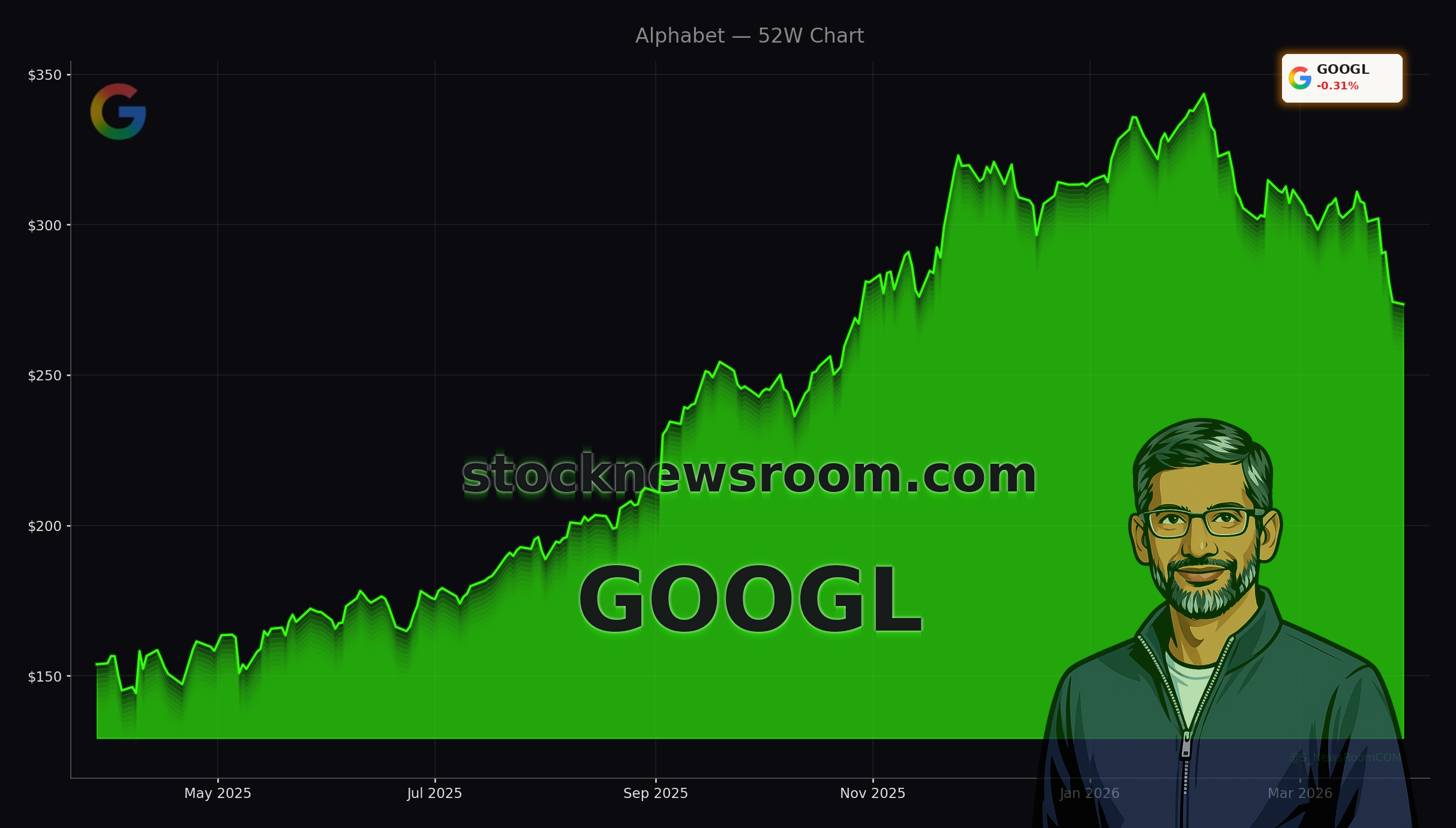

Alphabet Class A shares closed Monday at $273.50, down modestly on the day and roughly 14% year-to-date, while Class C shares ended at $273.14. Both lines trade well below recent highs, in line with a broader pullback in the “Magnificent Seven” as the NASDAQ and S&P 500 digest last year’s AI-driven gains. At the same time, Google’s unveiling of its TurboQuant algorithm has injected fresh volatility into the semiconductor complex, slamming memory stocks even as large‑cap tech buyers hunt for bargains.

The backdrop is a historic investment cycle in AI infrastructure. Capital expenditures across the big hyperscalers — Alphabet, Microsoft, Amazon, and Meta Platforms — are projected to surge more than 60% in 2026 to over $650 billion, close to 90% of their combined cash flow. That kind of spending has investors worried about margin pressure, but it also underscores how central AI has become to the earnings power of the entire mega‑cap tech cohort.

Against this backdrop, Alphabet TurboQuant has raised a new question: if software can dramatically shrink AI memory needs, does the physical chip build‑out suddenly look overdone?

What exactly is Alphabet TurboQuant?

Alphabet TurboQuant is Google’s newly disclosed advanced quantization and memory‑compression algorithm for large language models and vector search engines. According to the company’s research team, integrating TurboQuant can shrink key‑value (KV) cache memory size for AI inference workloads by at least 6x, with up to 8x speedups, while maintaining “zero accuracy loss” in benchmark tests. In practical terms, that implies a potential 80%‑plus reduction in DRAM and high‑bandwidth memory requirements for certain inference tasks.

The algorithm targets one of the most expensive bottlenecks in AI: fast memory sitting close to compute. For hyperscalers like Alphabet, NVIDIA-class accelerators and HBM stacks have been the biggest cost centers in building and running generative AI services. By squeezing more tokens and larger contexts into the same on‑chip and near‑chip memory footprint, Alphabet TurboQuant promises to bend the cost curve in Alphabet’s favor, especially when combined with its in‑house tensor processing units (TPUs).

This is not Alphabet’s first efficiency play. Management has already disclosed more than a 90% reduction in machine cost per search query during the rollout of AI Overviews. TurboQuant pushes that logic further: use better math and software so that every incremental dollar of AI infrastructure delivers more usable inference capacity.

Why did memory stocks panic?

The immediate market response came not in Alphabet’s stock, but in memory names. Micron Technology and Lam Research saw sharp declines after TurboQuant was announced, with Micron dropping double digits over the week as traders rushed to price in the idea of “demand destruction” for HBM and high‑end DRAM. A widely circulated interpretation of Google’s claims highlighted the possibility that optimized models might need up to 83% fewer memory chips for similar work.

Wall Street’s fundamental analysts, however, have largely pushed back on the most bearish scenarios. J.P. Morgan, for example, has maintained an aggressive $550 price target and Buy rating on key memory suppliers, arguing that Micron’s HBM supply for calendar 2026 is already effectively sold out, including industry‑leading HBM4 parts tied into NVIDIA’s next‑generation Vera Rubin platform. The core thesis: algorithmic efficiency tends to expand use cases and total AI adoption rather than permanently shrinking demand for memory.

Even within the chip complex, the view is that TurboQuant is more likely to slow pricing blowouts and stretch capacity than to collapse the long‑term TAM. But for now, Alphabet TurboQuant has become a convenient headline for traders looking to de‑risk after a huge run in semiconductor names.

Is Alphabet stock now a coiled spring?

While chip stocks sold off, **Alphabet Inc. (Google)** has quietly slipped into technically stretched territory. At around $273, GOOG/GOOGL trades below its 50‑day and 100‑day simple moving averages and is hovering just above the 200‑day SMA near $263, a level many technicians view as a key dividing line between a healthy correction and a potential longer‑term downtrend.

Momentum indicators are even more extreme. The 14‑day Relative Strength Index (RSI) for Alphabet has fallen to the high teens — roughly 18.2 — a level typically associated with capitulation in large‑cap growth. Historically, when Alphabet’s RSI has dipped below 20, it has often preceded sharp relief rallies as institutional buyers step back in. Some chart‑based forecasts are calling for a mean‑reversion move back toward the $310–$315 area by the end of April, particularly with Q1 2026 earnings scheduled for April 23 acting as a potential catalyst.

From a fundamental perspective, the setup looks very different from a classic value trap. Alphabet continues to benefit from a robust digital ad market, with Google and YouTube ad revenue growing at double‑digit rates and AI‑driven features such as AI Overviews and Circle to Search creating new surfaces for monetization. Google Cloud remains the third‑largest hyperscale provider but is growing revenue faster than Amazon Web Services and Microsoft Azure, while running at a solid profit.

How does TurboQuant fit into Alphabet’s AI edge?

For long‑term investors, the bigger story is how Alphabet TurboQuant reinforces the company’s structural AI advantages. Alphabet controls the dominant search engine with roughly 90% global share, the world’s most widely used browser in Chrome, and the Android mobile OS with close to 70% share. It also sits at the center of the consumer hardware ecosystem via a lucrative search revenue‑sharing deal with Apple, keeping Google as the default search gateway on iOS devices.

On top of this distribution, Alphabet has built Gemini, a competitive family of large language models that is steadily taking consumer share from rival chatbots while embedding deeply into search, Workspace, and YouTube. Under the hood, TPUs optimized for Alphabet’s own software stack deliver cost and performance advantages compared with generic GPU‑based solutions, a point that has been emphasized repeatedly by management as it ramps capex.

Alphabet TurboQuant adds another layer of moat: if Google can run similarly powerful models with significantly less memory, its marginal cost per query can drop even further. That’s especially important as hyperscalers including NVIDIA’s biggest customers face skepticism about the sustainability of current AI infrastructure spend. More efficient inferencing means Alphabet can offer more aggressive pricing to enterprise clients on Google Cloud, while still protecting margins — a dynamic that could pressure rivals as competition in AI platforms intensifies.

What are analysts and institutions doing?

Despite near‑term volatility, Wall Street’s fundamental stance on **Alphabet Inc. (Google)** remains broadly positive. Consensus ratings across major firms such as Goldman Sachs, Morgan Stanley, and Citigroup sit in the Buy or Overweight camp, with price targets generally implying upside from current levels over a 12‑ to 24‑month horizon. Analysts highlight Alphabet’s reasonable valuation — often cited around the low‑20s forward P/E for 2027 estimates — relative to expected mid‑teens annualized earnings growth.

Institutional flows support that view. Curated Wealth Partners LLC recently increased its position in Alphabet by more than 90% in the fourth quarter, making the stock one of its top holdings even after a roughly 16% pullback from highs. Ferguson Wellman Capital Management also added to its GOOG stake, pointing to confidence in Alphabet’s earnings resilience and AI road map despite rising regulatory and legal noise. On the technical side, some research shops flag the Ichimoku Kijun line around the high‑$290s as a key resistance level; breaking above that zone could confirm any post‑earnings rebound.

There are, however, dissenting voices. Some bearish technical analyses expect Alphabet to consolidate between the mid‑$260s and mid‑$280s for a time, citing the recent loss of key moving averages and ongoing macro uncertainty. Regulatory setbacks — including antitrust rulings and fines — remain a headline risk that could limit multiple expansion even if earnings performance stays strong.

How does this reshape the AI landscape?

The broader strategic question for U.S. investors is what Alphabet TurboQuant means in the context of the AI arms race among hyperscalers. Alongside Microsoft and Amazon, Alphabet is pouring tens of billions of dollars into data centers, networking, and custom chips, while also signing major distribution deals such as the integration of Gemini AI across Apple’s ecosystem and other large platforms. At the same time, the entire “Magnificent Seven” — including Tesla and Meta — have seen double‑digit drawdowns from all‑time highs, as markets reassess just how durable AI growth will be if efficiency gains accelerate.

Efficiency breakthroughs like TurboQuant cut both ways. They can temper the near‑term pricing power of memory suppliers and slow some of the most aggressive bull cases in semiconductors. But they also make AI cheaper to deploy at scale, especially at the edge and in specialized, energy‑efficient agents where Alphabet and Anthropic are seen as particularly strong. That in turn can widen the addressable market for AI‑enhanced search, productivity tools, and cloud services — areas where Alphabet already has massive installed bases and proven monetization levers.

Related Coverage

For a deeper dive into how Alphabet’s record AI capex program could shape the next several years of cloud competition, read “Alphabet AI Strategy Boom: $185B Capex Shock for Cloud”, which examines whether the spending surge sets up durable dominance or raises new risk for shareholders. For a broader sector view, including how a key rival is navigating similar questions, see “Microsoft AI Investment Record CapEx Shock Explained”, which analyzes whether Microsoft’s own AI build‑out is a smart long‑term bet or a costly detour.

In the end, Alphabet TurboQuant underlines why Alphabet is not just another mega‑cap tech name but a core architect of the AI stack itself. For long‑term investors, the combination of oversold technicals, resilient ad and cloud fundamentals, and a growing portfolio of efficiency‑enhancing tools makes the current pullback a pivotal moment to reassess exposure. The next earnings report and the first real‑world deployments of TurboQuant will show whether Google can turn its latest algorithmic win into sustained shareholder gains.