Is Amazon’s massive AI investment cycle a smart long-term bet or the start of a painful cash-flow squeeze for shareholders?

Is Amazon’s AI splurge hurting the stock?

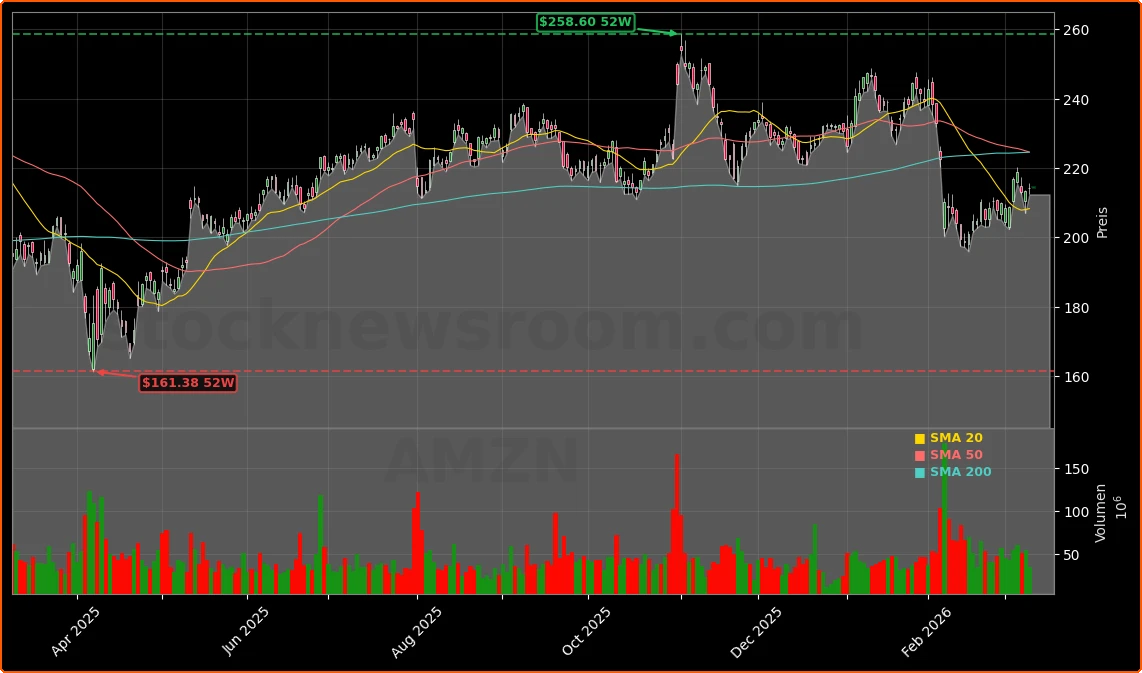

Amazon.com, Inc. (AMZN) shares have slipped about 7% so far in 2026, lagging a roughly flat S&P 500, even as the stock trades near $214.33 after a modest rebound. Investors are digesting a powerful mix of double‑digit revenue growth and a sharp drop in free cash flow, largely tied to the ongoing Amazon AI Investment build‑out across AWS data centers and infrastructure.

In the fourth quarter of 2025, net sales climbed 14% year over year to $213.4 billion, underscoring that both e‑commerce and cloud remain solid. AWS was the standout: revenue growth reaccelerated to 24% from 20% in Q3, giving the cloud unit an annual run‑rate north of $140 billion, fueled by demand for training and running large AI models. Operating income rose to $25.0 billion, or about $27.4 billion excluding special items, signaling that underlying profitability is improving even amid heavy capex.

The pressure point is free cash flow. Trailing 12‑month free cash flow fell to $11.2 billion from $38.2 billion a year earlier as capital expenditures, net of incentives, jumped by more than $50 billion. Management has been explicit that this is the price of seizing what it sees as a once‑in‑a‑generation AI infrastructure opportunity and that new capacity is being monetized as fast as it comes online.

How big is the Amazon AI Investment cycle?

The Amazon AI Investment push places the company alongside Microsoft and Alphabet in the hyperscaler arms race, with the three collectively pouring hundreds of billions of dollars into AI‑ready data centers, networking and chips. For Amazon, that has translated into trailing 12‑month operating cash flow of about $139.5 billion, up 20% year over year, much of which is being recycled into capex rather than returned to shareholders.

CEO Andy Jassy has emphasized that AWS has deep experience reading demand signals and converting capacity into strong returns on invested capital. The bet is that the current capex bulge will lead to durable high‑margin cloud and AI services revenue, from foundation model hosting to custom silicon like Trainium and Inferentia, which have recently gained traction with major AI players such as OpenAI on AWS.

This scale of spending has raised bubble concerns across AI‑linked equities, with some strategists warning that hyperscalers could be overbuilding. Yet institutional flows tell a more nuanced story. Headwater Capital Co Ltd recently initiated a roughly $22 million position in Amazon, making it the firm’s fifth‑largest holding, while K.J. Harrison & Partners boosted its stake by 17.3%, turning Amazon into its third‑largest position. Other investors, like Intech Investment Management and Parametrica Management, have trimmed holdings, but Amazon still remains among their top positions, reflecting both portfolio risk management and long‑term conviction.

Why turn to bonds to fund cloud and AI?

To finance the Amazon AI Investment program without overly diluting shareholders, the company has tapped the debt markets at scale. Amazon just completed the fourth‑largest U.S. corporate bond sale on record, issuing debt in 11 tranches, including a 50‑year bond. The deal was reportedly 3.4 times oversubscribed, with especially strong demand from European fixed‑income investors seeking exposure to U.S. AI infrastructure growth they cannot easily access through local equities.

Even with the new issuance, Amazon’s leverage looks conservative compared with some tech peers. Net debt to EBITDA stands near 0.3x, versus around 4x for legacy software names like Oracle, giving Amazon ample balance‑sheet flexibility. The trade‑off is a somewhat wider spread versus Treasuries amid today’s risk‑premium environment, but the company effectively locks in long‑dated capital to fund data centers, fiber, and chip development through multiple AI cycles.

Rating agencies and Wall Street banks have generally treated Amazon’s bonds as high‑quality paper. Equity analysts at major firms such as Goldman Sachs and Morgan Stanley continue to highlight AWS and AI as core drivers of long‑term earnings power, even as they flag that heavy capex and rising interest expense could cap margin expansion in the near term.

How does Amazon stack up against rivals?

For U.S. investors comparing AI exposure across the megacap complex, Amazon’s profile is distinct. Unlike Apple, which is more consumer‑hardware driven, or Tesla with its auto and energy tilt, Amazon’s AI story is anchored in cloud infrastructure via AWS and supported by a massive retail and advertising platform. That puts it closer to Microsoft Azure and Google Cloud under Alphabet than to chip suppliers such as NVIDIA.

In addition to cloud, Amazon is pushing AI into logistics, search, advertising and autonomous mobility. Zoox, its autonomous vehicle unit, just announced a multi‑year partnership with Uber to roll out driverless robotaxis in Las Vegas this summer and Los Angeles next year, potentially opening a new, AI‑enabled mobility revenue stream. At the same time, geopolitical risks are rising: Iranian authorities have named the infrastructure of Amazon, Google, Microsoft and others as potential targets in an expanding regional conflict, reminding investors that hyperscale data centers can be caught up in national‑security tensions.

Despite these headwinds, Amazon’s valuation around 30 times earnings looks reasonable to many growth investors given 24% AWS growth and the scale of operating cash flow funding the Amazon AI Investment effort. The main risk remains that capex stays elevated longer than expected or produces lower‑than‑hoped returns, which could force a reset in earnings expectations and capital‑allocation priorities.

We have deep experience understanding demand signals in the AWS business and then turning that capacity into strong return on invested capital.

— Andy Jassy, CEO, Amazon.com, Inc.

Conclusion

For now, the stock’s roughly 17% pullback from its 52‑week high, combined with strong institutional interest and a fortress balance sheet, suggests that the market is already pricing in much of that uncertainty. For long‑term investors comfortable with AI‑driven volatility, Amazon AI Investment spending positions the company as one of the central infrastructure providers of the next decade. The next few quarters will show whether AWS monetization keeps pace with capacity additions and whether Amazon can translate this AI super‑cycle into sustained earnings and cash‑flow growth.

Further Reading

- Amazon.com, Inc. (AMZN) Stock Price, News, Quote & History (Yahoo Finance)

- Amazon.com, Inc. $AMZN Shares Bought by K.J. Harrison & Partners Inc (MarketBeat)

- Headwater Capital Co Ltd Takes $21.96 Million Position in Amazon.com, Inc. (National Today)

- The Zacks Analyst Blog: Amazon, Micron, Bank of America, Waterstone and Crown Crafts (Zacks Investment Research)