Can Amazon’s aggressive AI spending spree turn a looming $200 billion capex wave into its next big profit engine?

Is Amazon’s AI Capex Wall Street’s Next Test?

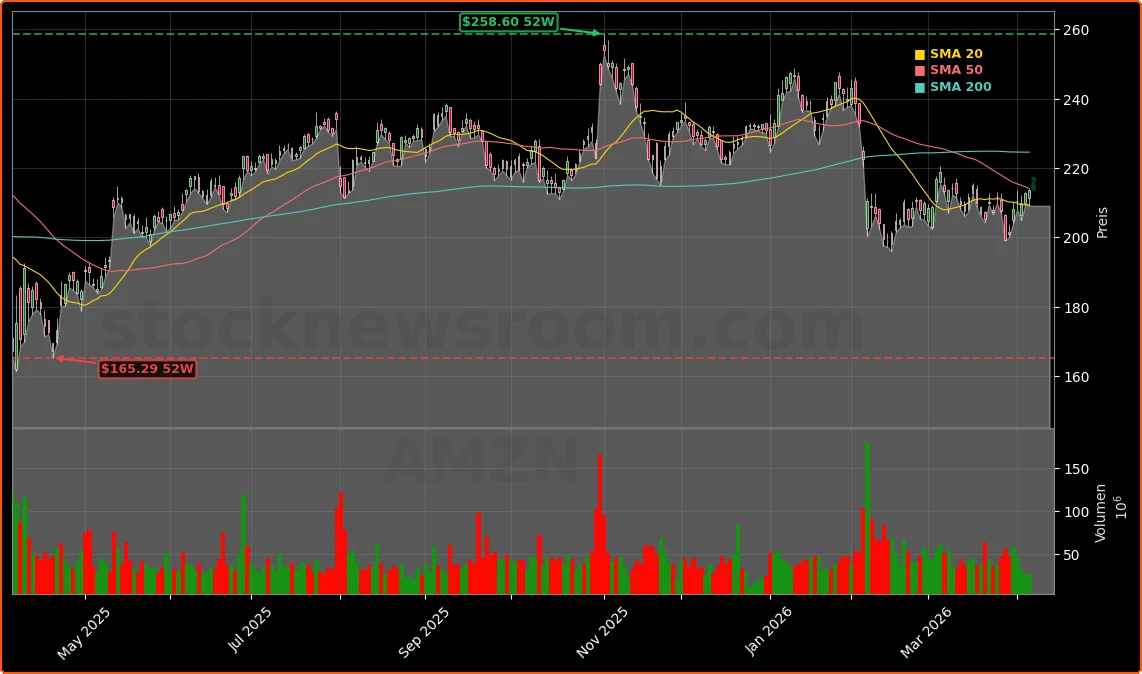

Amazon.com, Inc. (AMZN) closed at $213.77 on Tuesday, up 0.46% on the day, before ticking higher to about $217 in after‑hours trading. The move comes as investors digest an aggressive Amazon AI Strategy that could push total AI‑related capex toward the $200 billion range over the next few years. JPMorgan Chase CEO Jamie Dimon recently highlighted that hyperscalers like Amazon, Microsoft, Alphabet, Meta and Apple may collectively lift AI‑driven capex from roughly $450 billion in 2025 to $725 billion in 2026, underscoring the scale of the race.

Some investors worry the spending could pressure margins just as the “Magnificent Seven” basket posts one of its weaker quarters in recent years. Yet several Wall Street analysts argue the market is misreading the story. MarketWatch reported that at least one major analyst believes Amazon’s stock could climb as much as 50% if the AI build‑out in Amazon Web Services (AWS) translates into faster backlog growth and rising utilization of its in‑house Trainium and Graviton chips, which are increasingly used to run and train AI workloads more cheaply than third‑party GPUs from players like NVIDIA.

Invezz also emphasized that while the Amazon AI Strategy front‑loads costs into data centers, custom silicon and power infrastructure, indicators like AWS backlog and operating leverage across the group suggest long‑term upside if management executes. That’s one reason high‑profile investors such as Bill Ackman and Stanley Druckenmiller accumulated positions recently, even after Amazon’s more than 200,000% gain since IPO.

How Is Amazon AI Strategy Playing Out in the Cloud?

The heart of the Amazon AI Strategy sits inside AWS. The cloud unit already generates more than half of Amazon’s operating income, and AI is deepening that moat. Uber Technologies recently disclosed that it is expanding its use of AWS’s latest Graviton4 CPUs and Trainium3 accelerators to speed rider and delivery matching, where every millisecond matters. That deal is a live example of how Amazon’s custom chips can lock in enterprise workloads and differentiate AWS from Microsoft Azure and Google Cloud.

On the security front, Anthropic has invited Amazon and Apple into “Project Glasswing,” giving them early access to the new Mythos AI model to probe products for cyber vulnerabilities before public release. Reuters noted that Amazon, Microsoft and Apple are among the partners using the model’s red‑teaming and bug‑finding capabilities, a sign that major cloud and device ecosystems increasingly rely on shared, cutting‑edge AI tooling to harden their platforms.

At the hardware layer, Intel has been in advanced talks with both Google and Amazon around advanced packaging for custom AI chips. That would add another lever for Amazon to optimize cost per compute while tightening integration between AWS’s software stack and its silicon roadmap. For long‑term investors, these moves show that the Amazon AI Strategy is not just about renting GPUs; it is about owning the full AI infrastructure stack from chips to global data center footprint.

Logistics, USPS Deal and Pricing Tensions at Amazon

Beyond the cloud, Amazon’s core retail and logistics engine is shifting in ways that matter for both margins and policy risk. USA Today reported that Amazon and the U.S. Postal Service have struck a new package‑handling agreement that secures roughly 80% of Amazon’s existing USPS volume, preserving a key revenue stream for the cash‑strapped postal agency while giving Amazon continued access to nationwide last‑mile coverage it cannot fully replicate with its own vans and planes.

At the same time, Amazon has been pushing back on suppliers’ attempts to pass through higher costs. PYMNTS highlighted growing frustration among some brands after Amazon reportedly rejected requests from wholesalers to raise prices, effectively forcing many sellers to absorb higher customs duties, energy and logistics costs. While that supports Amazon’s low‑price value proposition to consumers, it risks driving some brands off the platform and feeds into broader debates about Amazon’s marketplace power.

For investors, the tension is clear: Amazon is leveraging its scale to manage inflationary pressures and protect consumer demand, but any perception of heavy‑handed pricing tactics could draw regulatory scrutiny, particularly as Washington watches Big Tech more closely in both AI and e‑commerce.

Will Robotics Make Amazon a Leaner Giant?

Another under‑appreciated strand of the Amazon AI Strategy is robotics. Amazon has quietly acquired multiple robotics startups, including Rivr, which builds dog‑like quadruped robots capable of climbing stairs and dropping packages at customers’ doors, and Fauna Robotics, whose “Sprout” humanoid‑ish robot is designed for safe interaction and complex warehouse tasks. Add in Zoox, Amazon’s self‑driving robotaxi and delivery unit, and a long‑term picture of heavily automated logistics begins to emerge.

Publicly, Amazon insists these robots will work alongside people to improve safety and productivity rather than simply replacing jobs. Internal discussions, however, reportedly consider the potential to automate hundreds of thousands of roles by the early 2030s to solve persistent labor shortages and wage inflation. That would place Amazon in more direct competition with humanoid robotics efforts such as Tesla’s Optimus, as well as industrial automation vendors across the S&P 500.

For the stock, robotics could act as a second‑order AI catalyst. If Amazon can blend computer vision, planning models and autonomous hardware into a unified logistics platform, unit costs per package and per order could fall sharply over time. That would amplify the earnings impact of any topline acceleration driven by AWS and AI services, a dynamic many valuation models have yet to fully incorporate.

Related Coverage

For a deeper dive into how the USPS agreement and fee structure fit into the broader Amazon AI Strategy and logistics revamp, see “Amazon Logistics Deal Warning reshapes USPS and fees”, which analyzes whether the new postal deal is routine housekeeping or a strategic reset of delivery economics. Investors interested in AI‑driven enterprise software beyond hyperscalers may also want to read “ServiceNow AI Partnership: -1.8% Shock Tests Bull Case”, which looks at how ServiceNow’s collaboration with DXC Technology could mirror some of the same AI adoption tailwinds that Amazon is targeting in the cloud.

In summary, the Amazon AI Strategy is reshaping everything from AWS silicon and cybersecurity partnerships to USPS logistics and warehouse robotics, forcing Wall Street to rethink near‑term margins against long‑term dominance. For U.S. investors, the stock’s current consolidation within the NASDAQ and S&P 500 looks less like a late‑cycle blow‑off and more like a pause before the next leg, provided AI‑driven cloud demand and automation gains materialize. The coming quarters, including fresh commentary on capex and AWS growth, will show whether Amazon can convert its AI and robotics bets into the kind of compounding cash flows that have rewarded shareholders for nearly three decades.