Is Amazon’s $200 billion AI infrastructure bet the next great growth engine for AMZN or a risky capex overload?

How big is Amazon’s new AI and capex push?

Amazon.com, Inc. is signaling that its next phase of growth will be defined by infrastructure for generative AI. Jassy told shareholders that Amazon plans to invest about $200 billion in capital expenditures in 2026, the bulk of it earmarked for AI‑ready data centers, networking and energy. He framed AI as a “once‑in‑a‑generation” shift that will touch everything from e‑commerce to healthcare, and stressed that the company is “not investing that money on a hunch.”

Early revenue traction is already visible. Amazon Web Services (AWS) is now running at an annualized AI revenue rate of around $15 billion, mainly from training and inference workloads that rely on both Amazon’s own silicon and GPUs supplied by NVIDIA. Jassy argued that as AI infrastructure becomes more efficient and cheaper, adoption will broaden and innovation should accelerate, supporting the overall Amazon AI Strategy well beyond the current hype cycle.

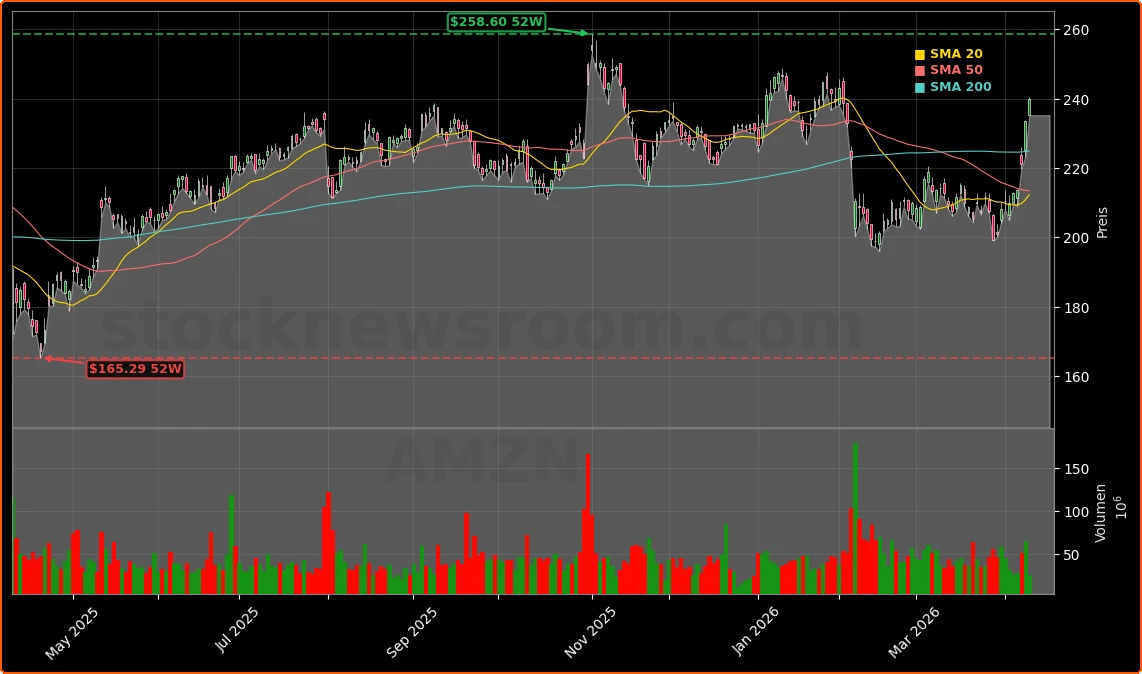

The stock has responded positively. After stabilizing near the psychologically important $200 level earlier this year, AMZN has rebounded and now trades roughly 10% below its 52‑week high, leaving room for upside if execution on AI continues to impress. Technical analysts at Barron’s see a potential path toward $300 in the second half of 2026 if the uptrend holds.

What role do Amazon chips play versus NVIDIA?

A cornerstone of the Amazon AI Strategy is reducing dependence on external GPU suppliers by scaling its own chip business. Jassy disclosed that Amazon’s custom semiconductor unit – which includes Graviton, Trainium (often described in German sources as “Gravitation” and “Granium”) and Nitro – has reached an annualized revenue run‑rate of more than $20 billion and is growing at triple‑digit rates. Two large customers have already locked up essentially all of the available Graviton capacity for 2026.

Even with this in‑house push, Amazon continues to buy substantial volumes of NVIDIA chips for AWS customers that prioritize maximum performance or compatibility. The strategy is to offer a lower‑cost alternative for many workloads while still giving enterprises access to the latest GPUs. Jassy has openly floated the idea of selling Amazon’s AI chips bundled into full servers to third‑party customers, which would move the company closer to competitors like Apple and Microsoft that are also commercializing custom silicon.

Investors worry that large capex programs can compress free cash flow, and critics note that megacaps such as Amazon, Alphabet and Microsoft are already outspending their current free cash generation and tapping debt markets. But bulls argue that if AWS operating income scales toward the $40‑$45 billion range over time, as some Wall Street models suggest, the returns on this silicon and data‑center buildout could be compelling for long‑term shareholders.

How do satellites and logistics fit the Amazon AI Strategy?

Beyond chips and cloud, Jassy highlighted Project Kuiper – described in his letter as “Amazon Leo,” a low‑Earth‑orbit satellite constellation – as a long‑duration bet on global connectivity. The network, set to begin service later this year, aims to deliver reliable broadband to underserved rural regions worldwide. Recent reports indicate Amazon is in acquisition talks with satellite and private‑5G specialist Globalstar to reinforce Kuiper’s spectrum and enterprise offering, underlining the strategic importance of space infrastructure within the broader Amazon AI Strategy.

In parallel, the company is pouring AI into its core logistics engine. More than one million robots already operate in Amazon fulfillment centers, where machine learning optimizes routing, picking and safety. Same‑day and ultra‑fast services like Amazon Now in India and the UAE, plus the Prime Air drone program, are designed to maintain Amazon’s delivery edge over rivals such as Tesla’s experimental logistics initiatives and traditional carriers. Management says rural customers receiving same‑day delivery almost doubled year over year in 2025 after more than $4 billion of investment in remote networks.

AWS’s importance is reinforced by marquee wins like a roughly $50 billion multi‑year cloud and AI agreement with OpenAI. Smaller partners are also leaning into the ecosystem: Latin American payments provider EVERTEC, for example, just achieved AWS Premier Tier Partner status via its Nubity cloud arm, underscoring AWS’s reach into emerging markets where e‑commerce and digital payments still have long runways.

What does this mean for AMZN on Wall Street?

On Wall Street, the debate now centers on valuation versus growth durability. AMZN trades on a forward price‑to‑earnings multiple around 30, a premium to the S&P 500 but roughly in line with other “Magnificent Seven” names. Some portfolio managers frame Amazon as a relatively safer compounder compared with more narrowly focused AI plays, with exposure across e‑commerce, cloud, advertising and now satellites.

While recent commentary has highlighted rising debt and heavy capex across megacap tech, large investors including Bill Ackman and Stanley Druckenmiller have been adding AMZN, viewing the stock as an AI beneficiary that has not yet fully rerated. Short‑term, the shares are sensitive to macro factors like digital ad spending, which tends to be cyclical, but the multi‑year thesis hinges on whether the Amazon AI Strategy can turn today’s infrastructure spending into tomorrow’s higher‑margin cloud, software and connectivity revenue.

Most major brokerages maintain positive ratings on Amazon, with price targets commonly clustered between $260 and $300, implying double‑digit upside from Friday’s price around $240 if execution remains on track.

Related Coverage

For a deeper dive into the capex side of the story, this analysis of Amazon’s AI Strategy and the potential $200 billion capex boom explores how incremental AI revenue could offset near‑term free‑cash‑flow pressure. Investors comparing big‑tech AI bets can also read how Meta is positioning itself in infrastructure through Meta’s AI Strategy and its surprising $21 billion CoreWeave deal, which sets up a useful contrast to Amazon’s in‑house chip and data‑center approach.

We’re not investing that money on a hunch; we’re doing it because we can already see strong customer demand and compelling early returns from our AI infrastructure.— Andy Jassy, CEO of Amazon.com, Inc.

In sum, the Amazon AI Strategy now stretches from in‑house chips and hyperscale cloud to robotics and low‑Earth‑orbit satellites, creating multiple avenues for monetizing AI over the next decade. For U.S. investors, AMZN offers diversified exposure to some of the strongest secular trends in tech, albeit with the usual execution and macro risks attached to such an ambitious spending plan. The next few earnings reports and customer wins will show whether this bold strategy can convert heavy 2026 investment into the next leg of profit growth.