Can the Amazon AI Strategy turn a $200 billion capex wave into lasting cash-flow growth before investors lose patience?

Is the Amazon AI Strategy overdone on capex?

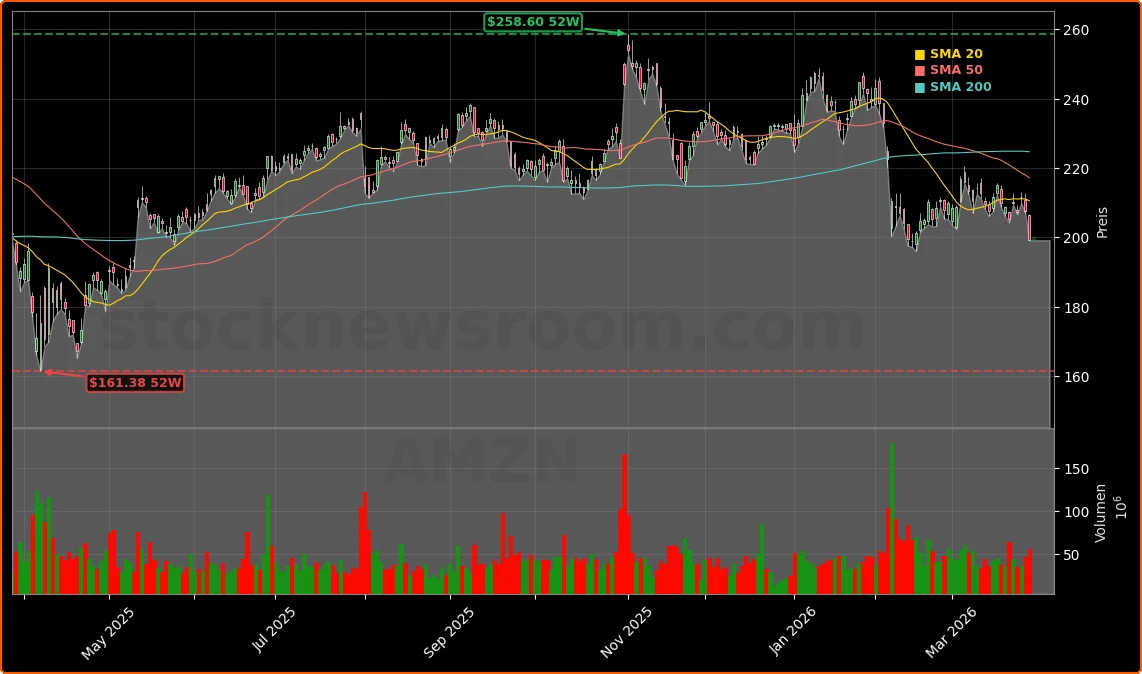

Amazon.com, Inc. is under pressure after estimates for 2026 capital expenditures tied to its Amazon AI Strategy and broader cloud build‑out swelled toward roughly $200 billion. That figure, spread across data centers, networking and accelerator hardware from suppliers like NVIDIA, has fueled worries that free cash flow could stagnate just as the S&P 500 sits near record territory. Technical traders on TradingView note the stock is hovering near key resistance around $200, with rising‑wedge patterns hinting at short‑term downside if sentiment on AI spending sours further.

Fundamentally, the bear case is straightforward: if AI demand in AWS and retail automation ramps more slowly than planned, return on invested capital could compress, leaving Amazon trading like a capital‑heavy utility rather than a high‑growth platform.

Does Amazon still offer a valuation discount?

Despite those fears, long‑term investors point to valuation. Within the “Magnificent Seven”, Amazon’s forward price‑to‑cash‑flow multiple near 9.7 screens as one of the cheapest alongside Meta. Analysis of 2027 cash‑flow estimates suggests the current multiple implies roughly a 48% discount to Amazon’s average over the past five years, even as AWS margins have nearly quadrupled since 2023 and remain the company’s profit engine. A recent Seeking Alpha study comparing NVIDIA and Amazon found AWS could sustain margins above 40%, underlining how the Amazon AI Strategy in cloud services is already monetizing through generative‑AI and large‑language‑model offerings.

Bullish strategists at firms such as Morgan Stanley and Goldman Sachs have argued that market worries about AI capex are overblown, grouping Amazon with Microsoft and Alphabet as prime rebound candidates after the latest pullback.

Can Amazon AI Strategy withstand Walmart and legal risks?

The competitive front is tightening. Walmart’s global e‑commerce revenue has surged past $150 billion with its ad business growing 46% in 2025, more than double Amazon’s 22% ad growth rate. While Amazon still generated a dominant $68.6 billion in ad revenue last year, Walmart’s lower ad penetration gives it more runway, echoing how Apple and other ecosystem players are pushing deeper into services. At the same time, a recent court ruling increased Amazon’s liability for addiction‑style harms from social‑media‑driven purchases, aligning it more closely with regulatory scrutiny faced by Alphabet and Meta.

For U.S. portfolios, the question is whether Amazon can keep converting its Amazon AI Strategy into higher‑margin AWS, ads and subscription income fast enough to offset capex, competitive pressure and legal risk. Compared with richly valued peers like Tesla, Amazon still looks like a discounted AI platform – but the market is demanding clearer proof that its spending spree will translate into durable cash‑flow growth.

Related Coverage

Investors focused on streaming, gaming and media should also examine how Amazon’s entertainment bets interact with its AI roadmap. Our deep dive in Amazon Entertainment Strategy +2.7% Rally Shocks Wall Street looks at whether Prime Video, music and sports rights can enhance customer data and monetization as AI personalizes content and advertising. For a broader view of defense and government AI demand, Palantir Government Contracts -3%: Defense AI Boom Warning analyzes how rising U.S. security spending may spill over into cloud, data and edge‑AI workloads, a trend that could indirectly support AWS.

In summary, the Amazon AI Strategy sits at the intersection of heavy capex, a rare valuation discount and intensifying Walmart competition, making the stock a high‑conviction but higher‑volatility AI play. For long‑term investors willing to stomach short‑term cash‑flow pressure, Amazon remains a core vehicle for exposure to cloud and retail AI at a relative discount. The next quarters will be crucial in proving that AI‑driven AWS, ads and subscriptions can more than pay for today’s spending surge and keep Amazon at the forefront of Wall Street’s AI trade.