Can the latest AMD AI Forecast and a $1.3 trillion chip boom call really justify the stock’s renewed rally?

Can AMD ride the $1.3T AI compute wave?

Bank of America’s upgraded 2026 semiconductor revenue target to $1.3 trillion underscores how central AI compute has become for the sector. The bank explicitly named Advanced Micro Devices, Inc. as one of the leading AI compute drivers alongside heavyweights like NVIDIA and Broadcom, arguing that data‑center AI workloads in compute, networking, and memory will capture most of the incremental gains. For the AMD AI Forecast, that implies a far larger addressable market for GPUs, CPUs, and full rack systems over the next several years.

Bank of America’s long‑term model now envisions the chip industry reaching $2 trillion in annual sales by 2030, implying around 20% compound annual growth—more than double the historical pace. To hit those numbers, global cloud capital expenditure would likely have to exceed $1 trillion by 2027, versus current consensus around $872 billion. That gap highlights both the upside and execution risk embedded in the AMD AI Forecast: the opportunity is enormous, but it depends on hyperscalers and enterprises sustaining aggressive AI infrastructure spending.

How is AMD positioned in server CPUs and AI?

Beyond macro forecasts, AMD is gaining tangible share in key data‑center segments. Recent market share data show AMD’s server CPU share climbing to about 41.3% in Q4, reinforcing its role as a leader in high‑performance EPYC processors for cloud and enterprise workloads. That strength is critical for AI, because advanced AI agents and large language models increasingly depend not just on GPUs, but also on powerful, scalable CPUs to orchestrate training, inference, and data pre‑processing.

Analysts at Citi have flagged this dynamic, putting AMD on an “upside catalyst watch” list based on rising demand for server CPUs tied to so‑called “agentic AI” and AMD’s ongoing share gains. In practice, that means cloud providers seeking alternatives to NVIDIA’s dominant GPUs may pair AMD’s AI accelerators with its own CPUs in tightly integrated platforms. The AMD AI Forecast therefore extends well beyond GPUs: full AI racks that bundle CPUs, accelerators, and high‑bandwidth memory could become multi‑billion‑dollar businesses as datacenters standardize around new architectures.

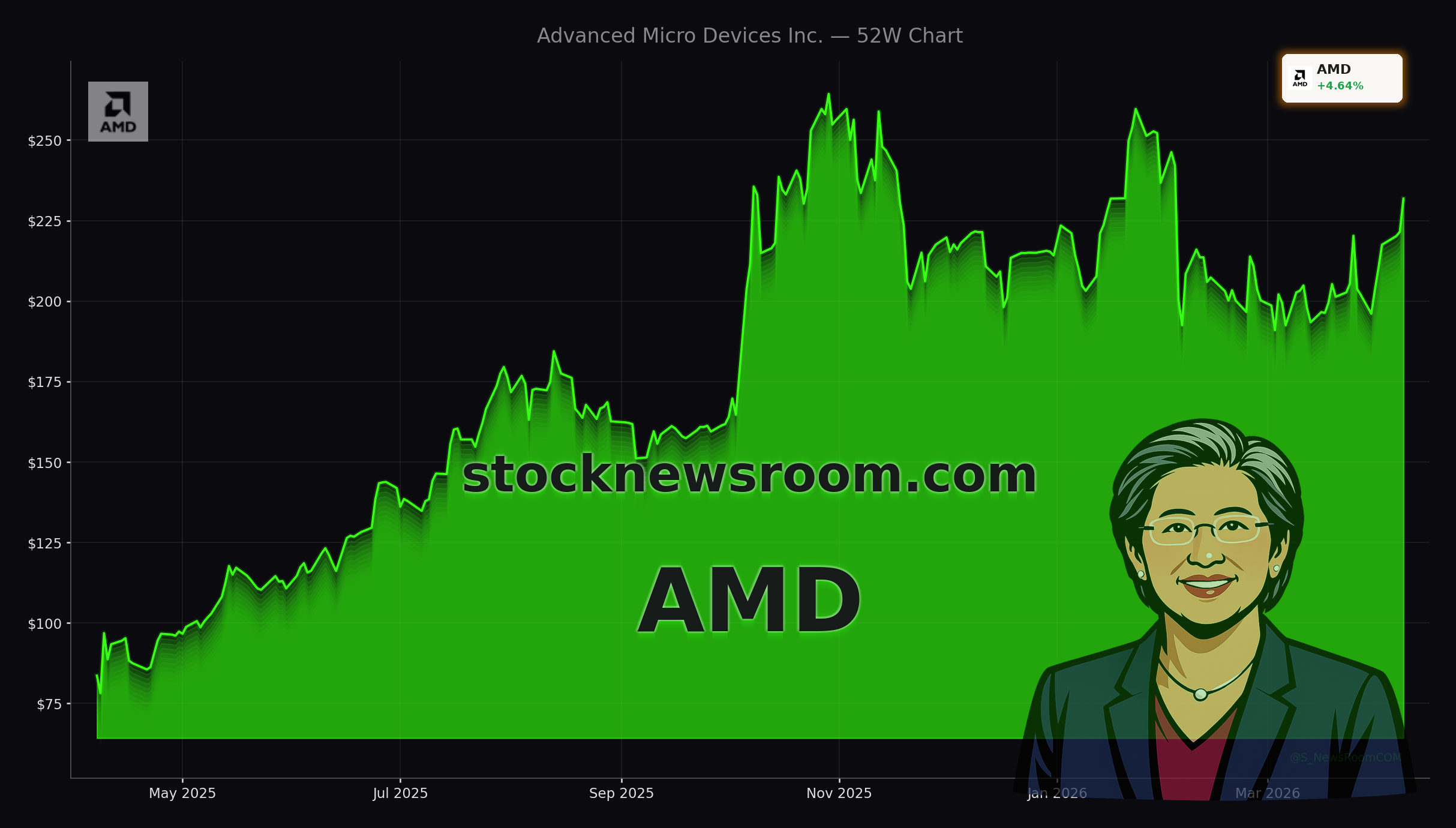

Technically, AMD’s stock backdrop supports this bullish narrative. The shares remain in a medium‑term uptrend, have broken back above key moving averages, and recently logged a five‑day winning streak with a roughly 13% gain. Short‑term indicators are approaching overbought territory, but the underlying pattern of higher highs and higher lows fits a market that is repricing long‑duration AI growth.

What are traders and technicians watching now?

Options markets are echoing the optimism around the AMD AI Forecast. Recent whale activity shows elevated call buying in AMD, signaling that sophisticated traders are positioning for continued upside rather than hedging downside risk. This options flow has coincided with AMD’s strong price momentum, suggesting that speculative capital is increasingly aligned with the long‑term AI compute thesis.

From a chart perspective, technical analysts highlight that AMD has pushed through resistance associated with its 50‑day simple moving average and is now targeting the $237 region as the next upside level, as long as it can hold support near $206. The current spot price around $231.82 places the stock closer to that near‑term target than to its support floor, reinforcing a constructive risk‑reward picture for short‑term traders. However, the rally has also left the shares trading at a premium valuation on forward earnings, something fundamental investors must weigh against the AI‑driven growth outlook.

On the fundamental side, earnings expectations for the current quarter have edged slightly lower, but full‑year and next‑year estimates still point to robust double‑digit revenue and EPS growth. AMD has a track record of beating consensus on both metrics, which keeps sentiment positive heading into upcoming quarters. Mixed analyst views—Wells Fargo and UBS staying bullish, while Citi trims its price target—reflect normal debate over near‑term execution rather than a fundamental break in the AI story.

How does AMD compare across the AI ecosystem?

The broader AI semiconductor ecosystem is in a powerful capital expenditure cycle, with hyperscalers investing more than $200 billion to scale out next‑generation data centers. NVIDIA remains the clear leader with an estimated 80% market share in AI accelerators, but AMD is steadily catching up, while TSMC and Samsung play crucial roles as leading‑edge manufacturers. Samsung, for example, is ramping HBM4 high‑bandwidth memory for AMD’s future accelerators, emphasizing how intertwined the supply chain has become.

Other chipmakers like Marvell, Broadcom, and Micron are key beneficiaries in networking and memory, while EDA players such as Cadence and Synopsys offer “picks and shovels” exposure to the AI design boom. For diversified US portfolios exposed to the NASDAQ and S&P 500, AMD sits at the intersection of several of these themes: data‑center CPUs, AI accelerators, and even premium PC and gaming chips, as illustrated by new AM5 bundle deals highlighted by PC‑hardware outlets. This breadth helps differentiate AMD from more narrowly focused peers and supports a constructive AMD AI Forecast despite macro and valuation risks.

Related Coverage

For a deeper dive into how AMD’s product stack across GPUs, CPUs, and full racks could translate into tens of billions of dollars in data‑center revenue, readers can explore this detailed look at the Advanced Micro Devices AI strategy. It analyzes how EPYC, Instinct accelerators, and platform‑level solutions may reshape AMD’s long‑term growth profile. Investors following the broader AI trade may also want to read about Meta’s latest AI push in the Meta Platforms Muse Spark stock surge, which highlights how rising AI workloads at hyperscalers can reinforce secular demand for chips from suppliers like AMD, Apple, and others.

Overall, the AMD AI Forecast is strengthening as major Wall Street banks and options markets converge on AI compute as the dominant growth engine for semiconductors. For US and global investors, AMD now sits squarely in the slipstream of a potential $2 trillion chip industry, with server CPU share gains and expanding AI platforms acting as key catalysts. The next few quarters of data‑center demand and cloud capex will determine whether this optimism solidifies into sustained earnings power, but for now AMD remains one of the most closely watched AI names on Wall Street.