Can the ambitious AMD AI Forecast for 60% data center growth really hold up against Nvidia’s dominance and rising valuation risks?

Is AMD’s AI growth story getting ahead of itself?

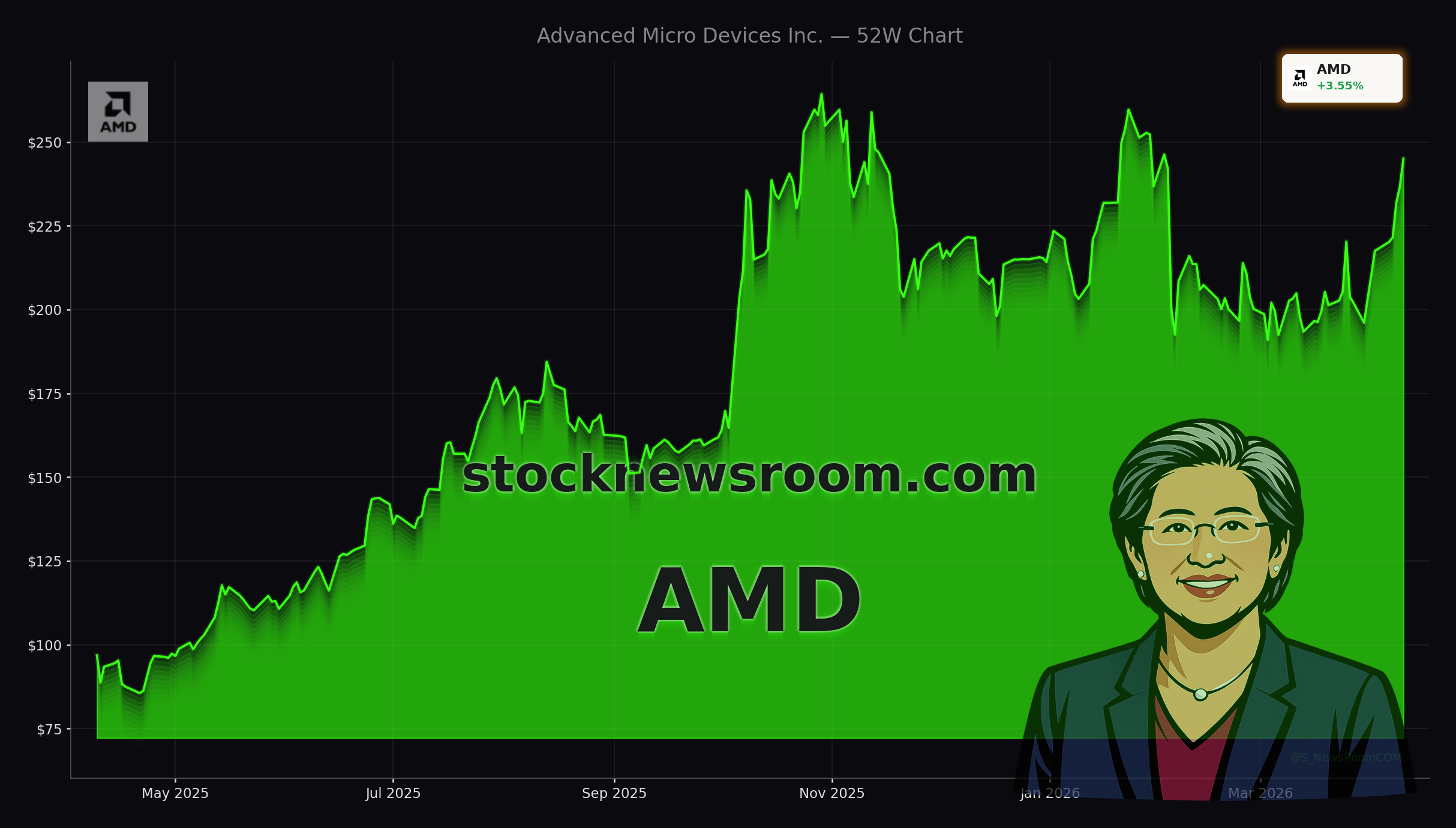

AMD climbed about 3.5% on Friday to roughly $245.04, modestly below the prior close of $245.55, and is slightly lower in pre-market trade on Monday. The move came alongside broad strength in chipmakers after a strong quarterly revenue update from TSMC underscored resilient AI infrastructure spending. AMD continues to trade well above key moving averages, a sign that bullish momentum in the name remains intact even after a huge multi-quarter run.

Underpinning the rally is the AMD AI Forecast that calls for a five-year compound annual revenue growth rate of around 35%. Management projects more moderate 10% annual expansion in client, gaming and embedded, but an aggressive 60% CAGR in its data center division, driven by AI GPUs and accelerators. If those numbers materialize, AMD’s business mix would tilt far more heavily toward AI compute, looking much more like today’s NVIDIA than the diversified CPU-GPU-embedded portfolio investors know now.

That vision has drawn substantial interest from U.S. growth managers who want exposure to the AI megatrend without betting solely on a single platform. But it also raises the bar for execution: sustaining 60% data center growth for years would require AMD to consistently win share, ramp new AI products on time, and secure enough advanced manufacturing capacity from foundry partners.

How does AMD stack up against Nvidia today?

While AMD and NVIDIA both supply GPUs for AI training and inference, their current positions are very different. Since 2023, Nvidia’s stock has surged more than 1,100%, reflecting dominant market share and explosive AI demand, while AMD is up about 240% over the same period. Over the last 12 months, however, AMD has outperformed, rising roughly 165% versus Nvidia’s 82%, as investors started to price in a catch-up story.

Fundamentally, AMD remains more diversified. Alongside data center GPUs, it sells x86 CPUs for servers and PCs, consumer gaming chips and embedded products via the Xilinx acquisition. In its most recent reported quarter, AMD delivered about $10.3 billion in revenue, up 34% year over year, with the data center segment contributing $5.4 billion, up 39%. Those are impressive numbers, but they still trail Nvidia’s AI-fueled growth rates and margins.

Valuation is where the AMD AI Forecast really gets tested. On a forward price-to-earnings basis, AMD trades at a premium of more than 50% to Nvidia, despite Nvidia growing faster and owning a far larger slice of current AI accelerator demand. For investors in the S&P 500 and NASDAQ looking for pure-play AI exposure, that setup makes it hard to argue AMD is the clear value choice today, even if its long-term roadmap is compelling.

What are analysts saying about the AMD AI Forecast?

Wall Street remains broadly constructive on AMD, but recent calls show a more nuanced stance. According to a compilation of Street views, 45 of 56 analysts rate the stock a Buy, with a median price target near $300, implying more than 35% upside from current levels. Citigroup recently cut its AMD target from $248 while maintaining a Neutral rating, citing the need to reconcile the ambitious AMD AI Forecast with already-stretched valuation and intense competition in data center GPUs.

On the other side, Erste Group upgraded AMD to Buy, arguing that accelerating demand for both CPUs and GPUs tied to next-generation “agentic AI” workloads in data centers supports the company’s multi-year growth story. Meanwhile, Cathie Wood’s ARK Invest has been trimming its AMD position, selling roughly $10.5 million worth of shares as it rotated capital into Palantir, a move that some traders interpret as a near-term valuation call rather than a verdict on AMD’s technology.

For U.S. investors, the split in opinions underscores that the AMD AI Forecast is not being dismissed, but it is being heavily discounted to reflect execution risk. Any stumble in upcoming product launches or a slowdown in AI spending could force analysts like Citigroup and others to reassess their growth models.

Can AMD’s data center ambitions reshape the AI landscape?

Beneath the headline CPU and GPU battle, AMD is also plugged into the broader AI infrastructure build-out. The proliferation of hyperscale data centers is driving demand not only for compute, but also for optical interconnects, power delivery and supporting components. AMD’s partnerships around its Helios platform and embedded offerings position it as a key silicon provider in that expanding ecosystem, even when it is not the obvious winner in top-tier AI accelerators.

Still, the center of gravity for the AMD AI Forecast remains its data center roadmap. Management’s target of 60% annual growth in this segment effectively assumes that hyperscalers and enterprise customers will increasingly diversify away from Nvidia’s CUDA stack and adopt AMD’s alternative platforms at scale. If that scenario plays out, AMD would justify its premium multiple and could even compress the valuation gap with Nvidia. If not, today’s price may already reflect much of the good news.

In the near term, investors will watch the upcoming Q1 2026 earnings report on April 28 for clues on data center order trends, AI GPU ramp progress and updated guidance. Implied volatility on AMD-linked ETFs indicates the options market is bracing for sizable post-earnings moves, highlighting just how central the AI narrative has become for the stock’s path on the NASDAQ and in AI-focused portfolios.

Related Coverage

For a deeper dive into how the latest AMD AI Forecast ties into a projected $1.3 trillion AI chip boom and what that might mean for future rallies, readers can explore AMD AI Forecast +4.6% Rally: Can It Own the $1.3T AI Boom?. That analysis looks more closely at long-term demand scenarios and competitive dynamics in the accelerator market.

Investors comparing AMD’s trajectory with other major U.S. chip players should also read Intel Strategy Boom: Irish Fab Buyback Marks Bold AI Pivot, which examines whether Intel’s manufacturing-heavy AI strategy can spark a real comeback. Taken together, these pieces help frame how AMD, NVIDIA and Intel might coexist in an AI-centric semiconductor cycle that increasingly shapes broader NASDAQ and S&P 500 performance.