Can the AMD AI Strategy built around OpenAI, Meta and Helios really justify a premium valuation in the next AI cycle?

How is AMD AI Strategy reshaping data-center growth?

The heart of the AMD AI Strategy is a pivot from selling standalone accelerators to capturing broader system-level revenue in data centers. AMD’s Instinct accelerators have gone from niche to mainstream, now in production at eight of the top 10 AI companies, making the business far more material to the company’s P&L than in prior AI cycles.

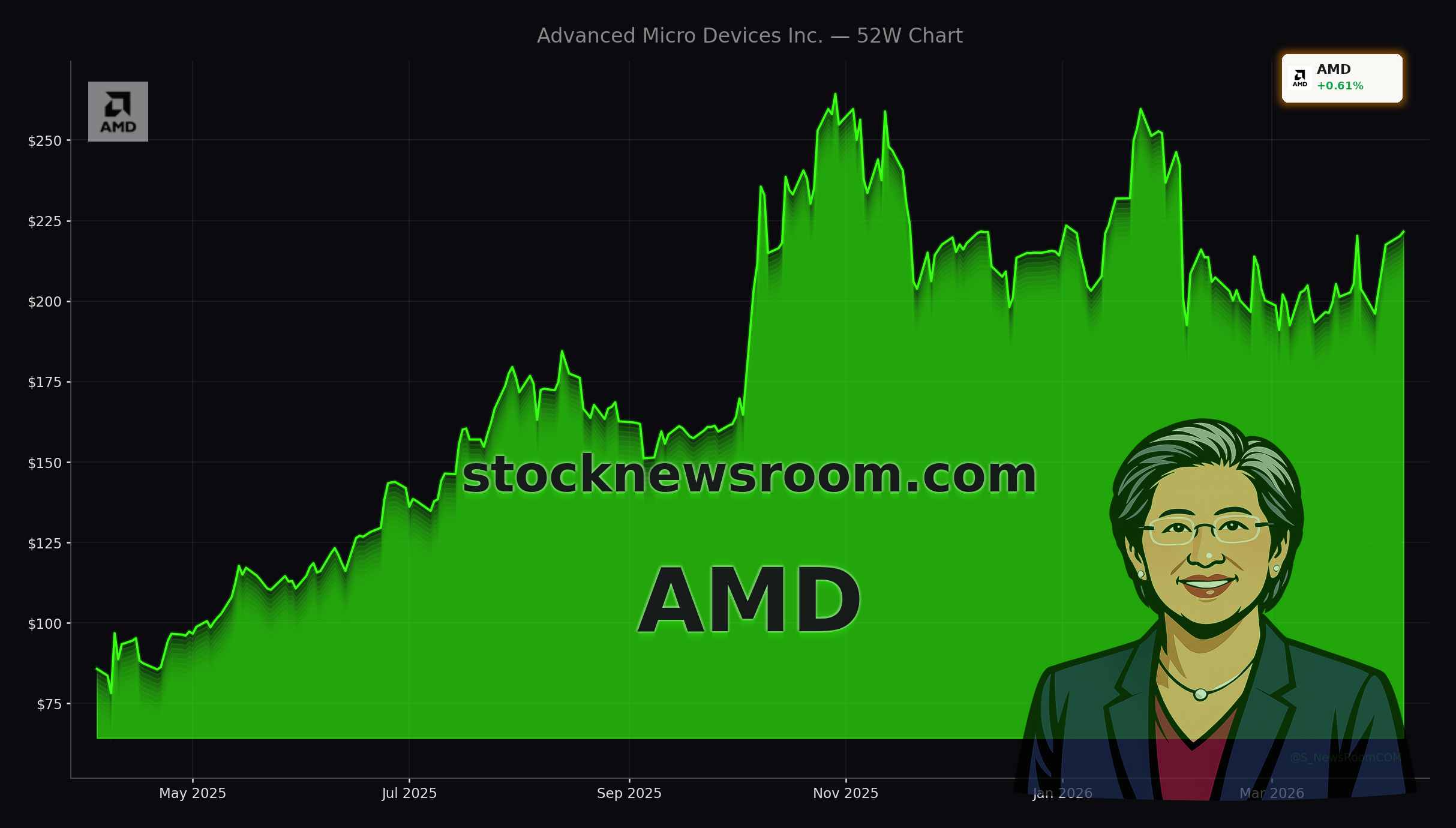

In Q4 2025, AMD delivered $10.3 billion in revenue, including a record $5.4 billion from its Data Center segment, and guided Q1 2026 revenue to roughly $9.8 billion. Importantly for investors tracking margin quality, AMD guided to a 55% gross margin for Q1, showing that AI-driven mix shift is lifting profitability rather than diluting it. With the stock up modestly to $221.53 (+0.61%) and only slightly softer at $221.19 after hours, Wall Street is watching whether this data-center base can support the premium multiple as the next wave of AI products arrives.

What role do OpenAI and Meta play for AMD?

A central plank of the AMD AI Strategy is two landmark GPU partnerships with OpenAI and Meta Platforms. Each deal is structured around commitments for 6 gigawatts of GPU capacity, effectively locking in large deployment footprints over multiple years. In return, AMD granted both customers warrants worth up to 10% of the company, tied to delivery milestones and share price performance—an aggressive but strategic move that hardwires ROCm software into their ecosystems.

These partnerships matter beyond headline capacity. Historically, AMD lagged NVIDIA because most AI code was written on CUDA, while AMD’s ROCm platform arrived a decade later and was viewed as buggy. Today, more AI workloads are built on open frameworks like OpenAI’s Triton, vLLM and SGLang, lowering switching costs and giving AMD a genuine opening. As inference workloads grow faster than training, total cost of ownership and energy efficiency become more important than absolute peak performance, and AMD’s typically lower GPU pricing could help it win incremental share if it continues closing the performance gap.

Can Helios and MI450 change the competitive landscape?

Analysts increasingly see the MI450 accelerator and the Helios rack-scale platform as the next major inflection for AMD’s AI business. Management has framed this product window, beginning in the second half of 2026 and extending through 2027, as the phase when AMD stops being judged solely on chip specs and starts competing directly on integrated AI infrastructure.

Helios allows AMD to ship pre-configured racks—combining Instinct accelerators, EPYC server CPUs and interconnect—rather than just components. That could significantly increase revenue per deployment and make AMD a more direct rival to full-stack offerings in the market, while also deepening lock-in once customers standardize on an architecture. Seeking Alpha recently highlighted this transition, noting that despite a roughly 50x forward P/E, AMD’s forward PEG near 0.8 suggests the market may still be underestimating data-center revenue compounding above 60% as these platforms scale.

How critical are CPUs and agentic AI for AMD?

Another underappreciated leg of the AMD AI Strategy is the focus on agentic AI and the resurgence of CPUs in AI data centers. As AI agents move from content generation to taking actions, reasoning and orchestrating tools, they need strong CPU resources alongside GPUs. GPUs provide the raw compute “muscle,” but CPUs coordinate workflows, handle logic and manage external tools—areas where AMD’s EPYC processors already have a strong position versus Intel.

The ratio of CPUs to GPUs in AI data centers is expected to narrow as agentic workloads scale, which could tighten CPU supply and support higher pricing. AMD has begun designing new CPU architectures explicitly for agentic AI, and its acquisition of ZT Systems bolsters its ability to ship racks tuned for these emerging workloads. For portfolios, this means AMD’s AI story is not just a GPU bet; it’s a hybrid CPU-GPU platform play that could provide a more diversified earnings base than single-product rivals.

What are analysts on Wall Street pricing into AMD?

Wall Street views remain constructive but not unanimous. Wells Fargo recently reiterated an Overweight rating and a $345 price target on AMD, pointing to strong demand for EPYC server CPUs, growing Instinct deployments, and the upcoming MI450 and Helios launches as reasons the stock could have more upside. UBS also maintains a Buy rating with a $310 target, citing confidence in AMD’s ability to secure additional gigawatt-scale AI deals beyond OpenAI and Meta.

Not every bank is fully convinced on near-term upside. Citigroup has trimmed its price objective in recent weeks, reflecting concerns about pacing of AI revenue recognition and potential volatility in China AI sales, even as it stays optimistic on short-term stock performance and highlights AMD alongside Analog Devices and Apple-linked supply chains as attractive technology exposure. Other coverage from Erste Group upgraded AMD to Buy from Hold, pointing to record 2025 revenue of $34.6 billion and the coming MI450 series as key growth drivers. Overall, the consensus “Moderate Buy” stance leaves room for estimate revisions if AMD executes cleanly on its AI roadmap.

Related coverage on AI and tech positioning

For a deeper dive into how AMD’s AI narrative is shaping sentiment, investors can review the analysis in Advanced Micro Devices Forecast +4.2% Rally Shakes AI Leaders, which explores whether the recent rally is backed by fundamentals or just crowded hedge fund positioning. To place AMD’s data-center and cloud ambitions in a broader platform context, it is also worth reading Amazon Logistics Deal Warning reshapes USPS and fees, which looks at how Amazon’s logistics and AI cloud strategies could influence competition and infrastructure demand across the tech landscape.

In conclusion, the AMD AI Strategy is evolving from catching up in GPUs to building a full-stack, CPU-plus-accelerator platform anchored by OpenAI and Meta deals, Helios systems and agentic AI. For U.S. investors, that shift offers a more tangible data-center earnings base to justify today’s valuation and potential upside if MI450 and Helios rollouts stay on track. The next few quarters and the 2026–2027 product window will show whether AMD can turn design wins into durable AI infrastructure share and cement its role alongside NVIDIA and other mega-cap tech leaders in the NASDAQ and S&P 500.