Can Apple’s new AI strategy with Gemini-powered Siri and fresh hardware really ignite the next growth phase for the stock?

Apple as a market anchor in an AI-driven S&P 500

At about $263.85, Apple remains one of the heaviest weights in the S&P 500 and NASDAQ, and its moves around artificial intelligence now have index‑level implications. While the broader tech complex has been driven by data‑center AI leaders like NVIDIA and Microsoft, Apple’s earnings power still comes primarily from iPhones, Macs and a fast‑growing services segment. The market’s focus has shifted to how those devices will become AI platforms rather than just hardware refreshes.

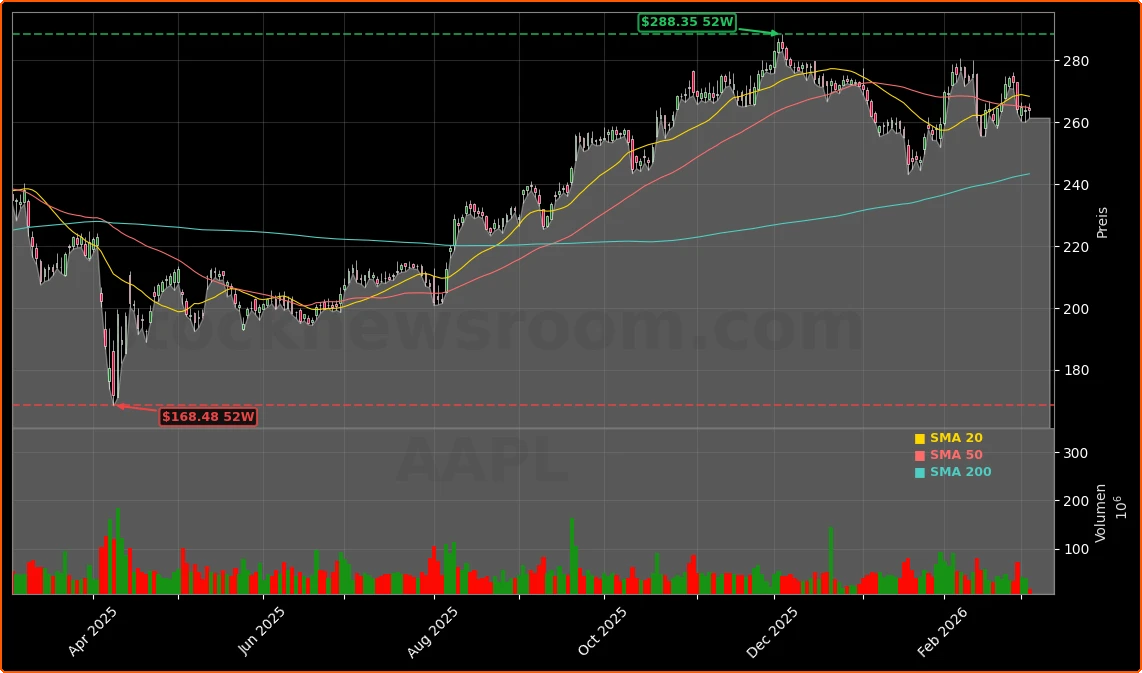

Recent volatility in global equities – including sharp drawdowns in some Asian markets tied to AI supply‑chain worries and geopolitical tensions – has underscored how concentrated AI expectations are in a handful of mega caps. Apple’s resilience stands out: the stock has shown relatively low volatility in a tight band between roughly $255 and $278, with technical analysts watching a potential breakout above the high-$270s as a trigger for a move toward and beyond $300. The stability reflects Apple’s massive free cash flow, sticky ecosystem and perception as a defensive growth name, even as its AI narrative has lagged cloud‑centric peers.

Against this backdrop, the Apple AI Strategy is shifting from quiet internal development to a visible, partner‑driven approach that aims to monetize AI on the “edge” – on hundreds of millions of iPhones, iPads and Macs – rather than through a $700+ billion cloud capex arms race. The new product wave and the Gemini deal are the first major signals of that pivot.

Apple AI Strategy: is the Gemini-powered Siri a strength or a risk?

The most controversial piece of the Apple AI Strategy is the decision to integrate a revamped Siri powered by Google’s Gemini large language models, reportedly at the trillion‑parameter scale. For a company that long insisted on owning the full technology stack, from chips to operating systems, leaning on a rival for core AI capabilities is a stark shift. Some investors see it as an admission that Apple missed the first wave of frontier model development.

Strategically, however, outsourcing parts of the model stack can be rational. Apple’s competitive edge has never been in running hyperscale data centers like Alphabet or Microsoft. Its strength is integrating hardware, software and services into a frictionless user experience and then extracting value from a massive installed base. By plugging Gemini into Siri, Apple can accelerate time to market for high‑quality generative features – natural language assistants, content generation and on‑device agents – while focusing its own silicon and OS engineering on privacy, efficiency and tight integration.

This Apple AI Strategy could catalyze an upgrade cycle if the new Siri feels meaningfully smarter than today’s version and is tightly woven into everyday workflows: messages, mail, calendar, photos, productivity apps and third‑party services. Bulls argue that if AI agents become the primary interface on smartphones, the platforms that control that interface – Apple on iOS and Alphabet on Android – will capture disproportionate economic value, regardless of who owns the base model.

The trade‑off is dependency risk. Apple will have to manage privacy, regulatory and negotiating dynamics carefully as it deepens technical ties with Alphabet, a direct competitor in phones, laptops and AI. But in the near term, the Gemini partnership gives Apple a faster path to parity with leading assistants, without the balance‑sheet drag of building a hyperscale training footprint from scratch.

Apple product wave: iPhone 17e, MacBook Neo and M5 Macs as AI hardware

Apple’s “big week” of launches underscores how the Apple AI Strategy is being executed through hardware first. The company rolled out the budget‑friendly iPhone 17e with the new A19 chip and Apple’s own C1X modem, promising roughly double the speed of prior Qualcomm-based solutions. Alongside that came refreshed MacBook Air models with the M5 processor and MacBook Pro models featuring M5 Pro and M5 Max chips, as well as new Studio Displays and updated iPad Air models running M4.

Crucially for AI positioning, these chips are not just about raw CPU/GPU gains; they embed ever‑more capable neural engines optimized for on‑device inference. As AI agents shift from cloud‑only to hybrid and local execution, M‑class Macs and A‑series iPhones can run many tasks at the edge – with lower latency, more privacy and potentially lower cloud costs. Wedbush Securities highlighted this in maintaining an “outperform” rating and a $350 price target, arguing that the broad-based hardware refresh materially lowers Apple’s revenue growth risk for fiscal 2026–2027 by preparing the installed base for AI features.

The new MacBook Neo, debuting at $599 (and even cheaper for education), is especially noteworthy. It is Apple’s most affordable new MacBook ever and the first to use an iPhone‑class chip – the A18 Pro – inside a Mac. Reviews have emphasized that while it is not built for professional video editing or 3D rendering, it offers performance akin to a high‑end iPhone on a larger macOS screen, with up to 16 hours of battery life and enough headroom for everyday productivity and light AI workloads. This makes the Neo a gateway device for Windows and Chromebook switchers who want access to macOS and Apple Intelligence without paying $1,100+ for a MacBook Air.

Bloomberg and other outlets noted that Apple has simultaneously nudged prices up on higher‑end MacBook Air and Pro models by about $100, justified partly by higher base storage and a global memory crunch. That mix shift – premium Macs creeping higher while the Neo undercuts prior entry points – suggests Apple is segmenting the Mac line into distinct AI tiers: cost‑conscious users on A18 Pro, mainstream and pro users on M5 and M5 Max, all capable of running AI features but at different performance and price levels.

Apple versus NVIDIA, Alphabet and Microsoft: competing AI narratives

On Wall Street, Apple is often discussed alongside NVIDIA, Alphabet, Microsoft and other trillion‑dollar giants that anchor AI indices and ETFs. But its AI story is structurally different. Nvidia and cloud providers monetize AI primarily in the data center, with hyperscale spending on GPUs and training clusters driving near‑term revenue surges. Apple, by contrast, barely participates in that capex cycle. Instead, it is betting that the real long‑term value accrues where inference happens most often: the edge devices people use every day.

That distinction matters for portfolio construction. AI‑heavy allocators may already be overweight Nvidia, Microsoft and Alphabet through core S&P 500 or total market ETFs. Incrementally adding Apple exposure is less about getting another data‑center AI proxy and more about owning the consumer‑side monetization of AI agents. If AI‑driven assistants become daily operating systems for work and life, Apple’s control over iOS and macOS user experience could translate into greater services attach rates, higher average selling prices and reduced churn.

There is also a risk element: some skeptics argue that Apple ceded the narrative to cloud peers by not launching its own brand‑name frontier models or AI developer platforms early. The Gemini deal underscores this perception. Yet Apple’s historical pattern has often been to arrive late to a trend – smartphones, tablets, wearables – but define the mass‑market version and then compound profits over long cycles. The Apple AI Strategy will either follow that playbook or prove to be the exception, and investors are currently pricing in only a moderate AI uplift versus the more explosive expectations embedded in Nvidia‑like valuations.

Can Apple’s fundamentals support an AI re‑rating?

Despite the AI narrative, Apple remains grounded in strong fundamentals. Research inspired by Robert Novy‑Marx on profitability factors shows Apple among the world’s most profitable companies, with high returns on capital and robust free cash flow yields. Those cash flows fund dividends, large‑scale share repurchases and selective acquisitions, all of which support per‑share earnings growth even in mature hardware markets.

Recent holiday‑quarter results surprised many doubters. iPhone revenue grew more than 20% year over year, a remarkable performance given the size of the base and the competitive landscape. The services segment – app store, subscriptions, cloud, payments and more – continues to be a high‑margin growth engine that deepens the ecosystem and stabilizes earnings. Institutional investors such as Terra Alpha Investments and Victrix Investment Advisors have increased their Apple holdings, making it a top‑five position in their portfolios, citing AI upside and services momentum. While some headlines have focused on Warren Buffett trimming his stake, the broader institutional flow remains supportive.

On the sell‑side, Wedbush projects fiscal 2026 revenues around $461 billion, rising toward $481 billion the following year, with EPS climbing from roughly $8.50 to $9.27. Those estimates imply mid‑single‑digit to high‑single‑digit annual growth, not an AI hyper‑growth story, but solid for a company of Apple’s scale. At the current share price, that leaves Apple trading at a premium to the broader S&P 500 but at a discount to the fastest‑growing AI beneficiaries. The investment case hinges on whether the Apple AI Strategy can convert that steady baseline into a somewhat higher growth trajectory without undermining margins.

There are cost pressures to monitor. The global memory supply crunch is pushing RAM prices higher as capacity is redirected into AI data centers, raising bill‑of‑materials costs for laptops and smartphones. Apple, with its vast purchasing power, can partially buffer these increases, but higher entry prices for MacBook Air and Pro models show that some of the pressure is being passed through to consumers. Over time, if AI workloads on devices drive demand for more memory and storage, Apple will need to balance spec upgrades, price points and margins carefully.

Technical view and portfolio implications for U.S. investors

From a technical perspective, Apple’s chart currently shows a consolidation or “flag” pattern, with support around the mid‑$250s and resistance in the high‑$270s. Some technicians argue that a decisive breakout above approximately $275–$278 on a closing basis could clear the way toward new all‑time highs above $300, given the relatively narrow trading range and contained volatility. Others prefer a more contrarian approach, entering positions closer to support with stops near $254 to manage risk.

For diversified U.S. investors, Apple’s role remains that of a core holding rather than a tactical trade. It is heavily represented in S&P 500 and total‑market index funds, meaning many retirement portfolios already carry substantial exposure through vehicles like the Vanguard Total Stock Market ETF. Active investors deciding whether to overweight or underweight Apple should weigh the stability of its cash flows and buyback support against the possibility that AI benefits accrue more to data‑center‑oriented names.

Compared with more speculative AI plays or high‑beta growth stocks, Apple offers a different risk‑reward profile. It is less likely to deliver explosive upside from AI alone but also less likely to suffer catastrophic downside if AI expectations reset. In an environment where traditional retirement rules like the “4% rule” are being re‑examined amid higher rates and longer life expectancies, holdings with durable, cash‑generative business models and moderate growth can help stabilize withdrawal strategies. Apple fits that pattern, with the Apple AI Strategy providing a potential, but not yet fully priced in, growth kicker.

Investors should also consider competitive encroachment on the low end. The MacBook Neo targets the very segment where Chromebooks and budget Windows laptops have been strongest. If Apple succeeds in this price band, it could expand its addressable market meaningfully. If it fails, Neo risks being a low‑margin distraction. Early reviews highlight strong value for casual users and on‑device AI, but real traction will be visible only over several quarters of shipment data and education deals.

Ultimately, positioning Apple in a portfolio comes down to how one views the edge‑AI thesis. Those convinced that AI agents will live primarily in the cloud may favor higher exposure to Nvidia, Microsoft and Alphabet. Those who believe that most of the value will be realized in smartphones, laptops and wearables in daily use may see overweighting Apple as a more compelling long‑term bet.

Conclusion

In sum, the Apple AI Strategy is moving from concept to execution. With Gemini‑enhanced Siri, a full stack of AI‑ready hardware from iPhone 17e to M5‑powered Macs and the aggressively priced MacBook Neo, Apple is positioning itself for the next decade of AI at the edge. For investors, the company still looks more like a durable, cash‑rich compounder than a speculative AI rocket ship, but the strategy now offers a clearer path to incremental growth – and possibly a valuation re‑rating – if Apple can turn AI assistants into everyday must‑have features across its vast installed base.

Further Reading

- Apple Inc. (AAPL) Stock Price, News & History (Yahoo Finance)

- Everything you need to know about Apple’s ‘big week’ of product launches (NBC Bay Area)

- Apple just dropped 6 new products. What are they? (USA Today)

- Wedbush maintains $350 Apple target as product blitz reinforces AI hardware push (Proactive Investors)