Is Apple’s quiet satellite push about to become a high‑stakes battleground as Amazon circles key partner Globalstar?

Is Amazon forcing a rethink of Apple Satellite Strategy?

The immediate catalyst for Wall Street is Amazon’s reported talks to acquire Globalstar, the satellite communications company in which Apple holds a 20% stake after a roughly $1.5 billion commitment to expand its constellation and ground network. Globalstar enables iPhone emergency SOS via satellite, making it a critical—if often overlooked—pillar of the broader Apple Satellite Strategy. Any change of control at Globalstar would have to accommodate Apple’s economic interest and strategic roadmap for satellite-enabled services.

For Amazon, Globalstar would accelerate its low-Earth-orbit internet ambitions as it races to close the gap with SpaceX’s Starlink. For Apple Inc., it introduces a new layer of negotiation leverage and risk: Amazon could become both a competitor in cloud and AI and a de facto infrastructure partner in orbit. Investors will watch closely whether Apple pushes for contractual protections, alternative launch partnerships, or even diversifies satellite relationships beyond Globalstar and SpaceX to preserve optionality.

With Globalstar shares jumping more than 15% in after-hours trading on the report, the market clearly sees strategic value in this asset. For Apple, the question is whether the Apple Satellite Strategy remains a quiet feature play—or evolves into a more explicit connectivity platform spanning safety, messaging and potentially premium data services.

How critical is satellite to Apple’s next hardware cycle?

Satellite connectivity arrived first as an emergency capability on recent iPhones, but it fits neatly into Apple’s history of layering must-have features into a maturing product line. As the iPhone approaches two decades on the market, the company is rumored to be working on form-factor leaps such as a foldable iPhone and new spatial computing devices. In that context, the Apple Satellite Strategy looks less like a side project and more like a foundational layer for always-available, AI-enhanced services, even when users are off the grid.

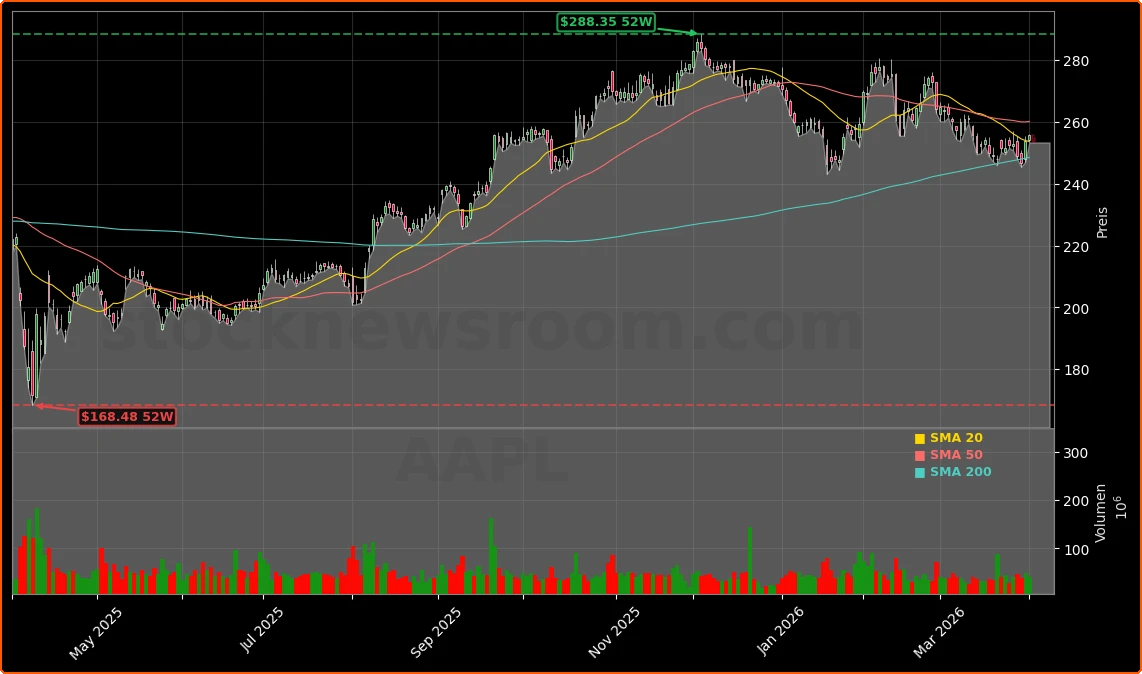

The numbers underline why this matters. In the latest reported holiday quarter, iPhone revenue around $85 billion again demonstrated that the smartphone remains Apple’s core profit engine. Over the last five years, shareholders have seen a total return of roughly 114%, outpacing the S&P 500, helped by strong margins and a powerful brand. Sell-side analysts tracked by The Motley Fool expect diluted EPS to compound at about 11.6% annually through at least 2028, with valuation assumptions implying potential double-digit annualized returns if execution holds.

To sustain that, Apple will likely keep using satellite hooks as a differentiation tool against Android OEMs and connectivity initiatives at rivals like Tesla and Amazon. From a portfolio perspective, the more deeply satellite becomes embedded in the iPhone and Watch experience, the stickier Apple’s ecosystem—and its Services revenue stream—could become for long-term investors.

Is Apple really behind in AI versus NVIDIA and others?

While headlines focus on the Apple Satellite Strategy and off-planet infrastructure, the louder debate on Wall Street is whether Apple is falling behind in artificial intelligence. Compared with hyperscalers and chip leaders like NVIDIA, Apple has been quieter on foundation models and cloud AI, prompting concerns that it may be ceding ground in the “Magnificent Seven” race.

Yet Apple’s strengths are different: it controls more than 2.5 billion active devices, designs its own silicon, and owns the operating systems, App Store and Services stack. Rather than shouting about model sizes, the company is expected to deepen on-device and hybrid AI at the software layer, including a significantly upgraded Siri and multi-agent integrations with partners like Google Gemini and OpenAI. This mirrors how Apple handled search—outsourcing the heavy compute while monetizing distribution.

Goldman Sachs recently highlighted that telecom efforts like AT&T’s OneConnect value offering could pressure premium smartphone demand, implicitly challenging Apple’s pricing power. At the same time, research desks at Goldman Sachs and Bernstein flagged potential share shifts for Qualcomm as Apple accelerates more in-house chip development. In other words, AI and modem choices at Apple are reshaping the broader mobile supply chain, even if Apple itself maintains a relatively closed narrative on its AI roadmap.

What does 50 years of Apple innovation tell investors?

As Apple turns 50, the company’s history offers context for both the Apple Satellite Strategy and its AI trajectory. From the garage-era Apple II to the Macintosh, iPod, iPhone and App Store, the firm has repeatedly reinvented its core experience rather than simply chasing specs. Former early employees point to Apple’s ability to change course as its real moat; when the company stopped evolving in the 1990s, it stumbled.

Today, CEO Tim Cook earns high marks from many institutional investors for operational excellence: supply chain resilience, record Services margins, disciplined dividends and massive buybacks, plus a renewed $400 million commitment to U.S. manufacturing through 2030 that reinforces political and logistical positioning. Criticism focuses less on execution and more on whether Apple can deliver the next breakthrough product—and whether AI and satellite integration will feel truly new or incremental.

Upcoming milestones will test that narrative: a potential foldable iPhone, more advanced spatial computing hardware, and WWDC announcements around Siri and AI-powered interfaces. Apple has historically preferred to be a fast follower, entering categories after rivals like NVIDIA and Google prove out demand, then using tight hardware-software integration to deliver a more polished experience. Satellite connectivity and AI orchestration are likely to be no different.

Related Coverage

Investors looking for a deeper dive into Apple’s capital spending and AI positioning can explore how its domestic factory push plays into risk management and innovation in Apple US Manufacturing -1.5%: AI Boom or Risk Warning?. For broader tech-sector context around software and AI financing firepower, the analysis in ServiceNow Financing: $3B Credit Line and Rating Shock shows how other enterprise leaders are arming up for the next phase of digital transformation.

In the end, the Apple Satellite Strategy, AI catch-up and 50-year innovation track record converge on a single investor question: can Apple keep turning infrastructure bets into sticky, high-margin user experiences. With the stock recently trading around $255.63 and analysts modeling roughly market-like returns ahead, the next big product and platform reveals—from orbital partnerships to Siri’s reinvention—will be decisive. For long-term portfolios, Apple remains a central tech holding whose off-planet and on-device moves are both worth watching very closely.