Is the current -4.5% drop in ASML just a healthy pause in ASML’s AI growth or the start of a larger correction?

What’s Behind the ASML Correction?

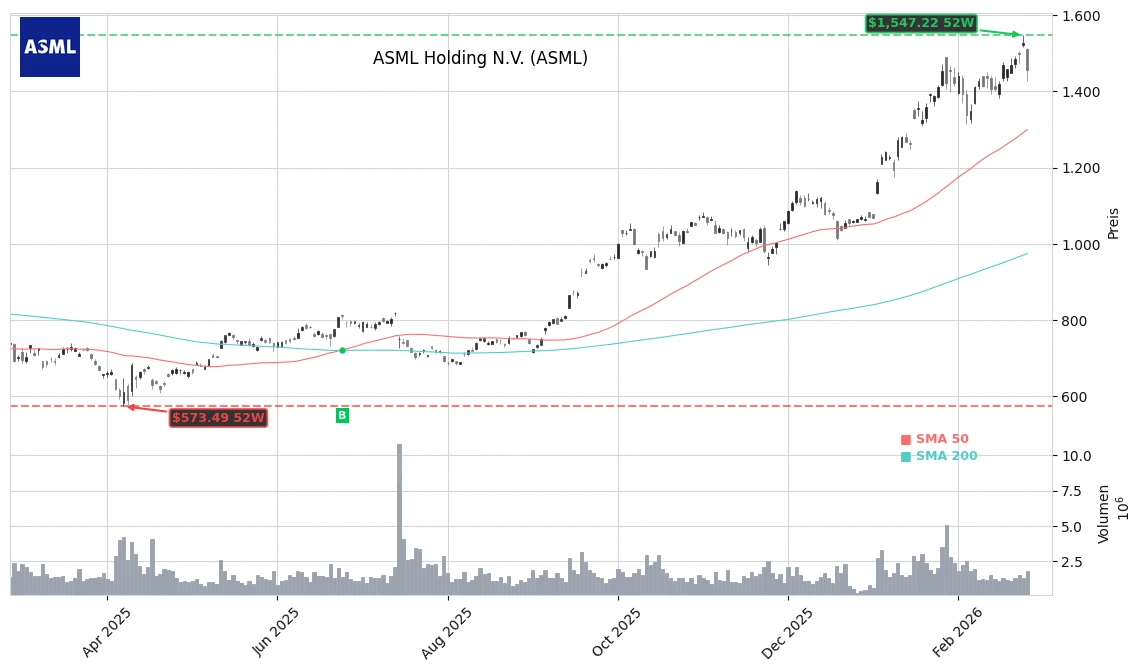

The stock of ASML Holding N.V. is down 4.54% today to $1,457.24. This reflects a technical breather after a massive rally: the stock had nearly doubled in the last six months and recently marked a new all-time high. Now, a shift in sentiment in the AI sector, triggered by profit-taking following strong numbers from Nvidia, has pulled ASML down.

Fundamentally, there has been no new negative news from ASML. Instead, many investors view the entire chip sector as overbought in the short term. ASML’s price-to-earnings ratio is reportedly around 50, even higher than Nvidia’s, which increases sensitivity to profit-taking. Short-term traders are cashing in after the stock’s doubling, while long-term investors are focusing more on the structural ASML AI growth.

How Does ASML Benefit from the AI Boom?

The core of ASML’s AI growth lies in its unique technology: ASML is the only manufacturer of EUV lithography systems worldwide, which are essential for cutting-edge chips with structure sizes of 7 nanometers and smaller. These high-performance chips power data centers, AI models, and high-end graphics processors. Over the past five years, ASML has increased its revenue by about 100%, while its stock price has risen approximately 162% during the same period.

The company continues to invest aggressively in productivity enhancements. A new EUV process or a more powerful light source is expected to enable customers to produce about 50% more chips per hour by the end of the decade. This lowers unit costs, increases the attractiveness of the systems, and simultaneously strengthens ASML’s pricing power. Combined with the global establishment of new chip factories in the U.S., Europe, Japan, and Taiwan, this is likely to sustain ASML’s AI growth for many years.

In its recently published 2025 annual report, ASML emphasizes that demand from the artificial intelligence sector is now seen as a central long-term growth driver. EUV technology is already contributing an increasing share of total revenue, and the trend toward ever-smaller structure widths continues to play into the monopolist’s hands.

What Do Forecasts and Valuations Look Like?

Analysts expect ASML’s revenue to nearly double from approximately $37 billion to about $75 billion over the next five years. With an operating margin of around 35%, this would correspond to an operating profit of over $26 billion. Based on a market capitalization of around $600 billion, this would imply a multiple of about 22 times the expected operating profit in five years.

Several research firms point to the robust order book, strong position in the AI value chain, and growing dividends and stock buybacks. At the same time, institutions like Zacks Investment Research caution against the high valuation and potential short-term price fluctuations. Classic Wall Street firms such as Citigroup, Goldman Sachs, Morgan Stanley, or RBC Capital Markets generally express a positive outlook for the sector, but see the risk of temporary corrections for highly valued AI beneficiaries like ASML within normal market cycles.

What Does This Mean for Investors in ASML’s AI Growth?

Institutional investors continue to leverage the story around ASML’s AI growth to expand their positions. Several asset managers have significantly increased their stakes in ASML recently, underscoring the stock’s attractiveness for long-term investors. Additionally, an increased quarterly dividend and ongoing stock buyback programs support total returns.

Despite this strong fundamental basis, the stock remains vulnerable to pullbacks due to its ambitious valuation—as evidenced by today’s price drop following Nvidia’s reaction. For long-term investors, however, such a correction could be seen more as an opportunity to gradually build positions in ASML’s AI growth rather than as a break in the investment case. It will be crucial for ASML to confirm the expected acceleration in order intake in the AI and high-performance computing segment in the coming quarters.

Bottom Line

ASML’s AI growth remains intact despite the recent price correction, as the company holds a monopoly position in the center of global AI chip manufacturing. For investors, the decline represents more of a normalization after an extraordinary rally than a fundamental trend reversal. The next quarters and the implementation of announced productivity enhancements will reveal whether ASML can continue its growth trajectory in the AI era dynamically.

Related Sources

- ASML Holding N.V. Stock Price and Metrics (Yahoo Finance)

- Why ASML Stock Was Down Today (The Motley Fool)

- Where Will ASML Be in 5 Years? (The Motley Fool)

- ASML sees AI demand as long-term growth driver in 2025 annual report (Reuters)