Is Boeing’s sliding share price hiding a major upside from a rapidly expanding Boeing Defense Budget?

How is Boeing moving the Dow today?

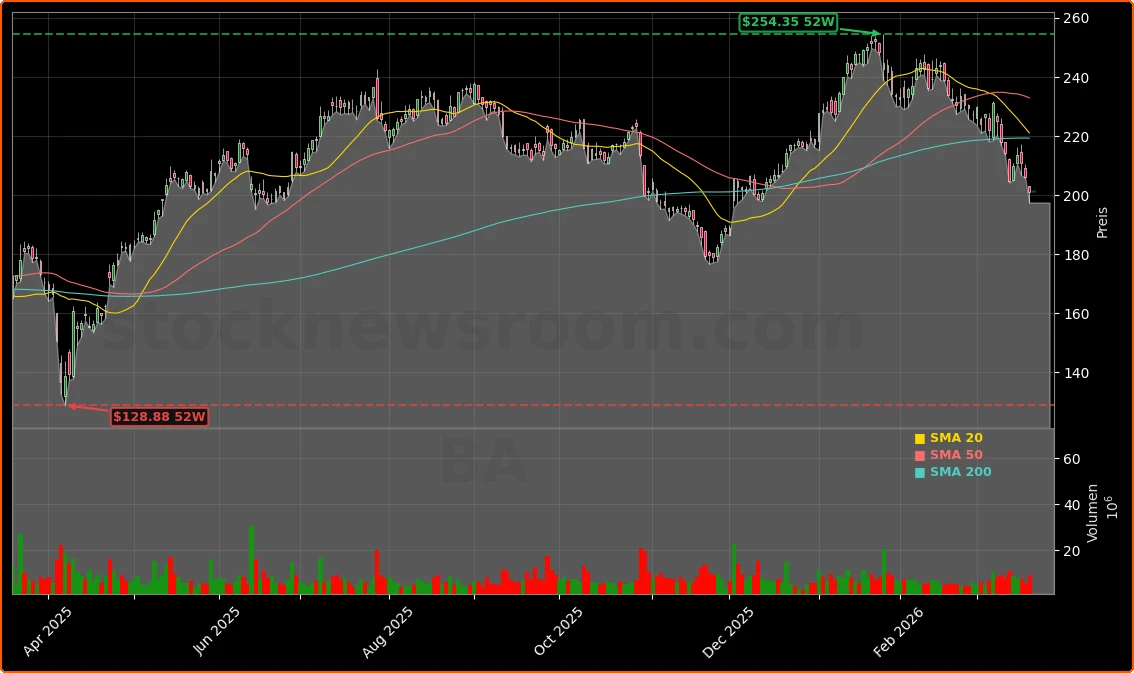

The Boeing Company (BA) was again one of the heaviest drags on the Dow Jones Industrial Average on Thursday, with the stock down $4.73, or about 2.3%, to $201.18 before inching slightly higher in after-hours trading to $201.50. Moves in Boeing have an outsized impact on the price-weighted Dow, where a $1 change in any component roughly equates to a 6.16‑point swing. At several points during the U.S. session, Boeing’s weakness, alongside 3M and Sherwin‑Williams, accounted for more than 70–90 points of downside pressure in the index, even as the broader S&P 500 slid a more modest 0.3%.

The selling comes despite a constructive fundamental backdrop: aerospace and defense peers like GE Aerospace, RTX and Lockheed Martin have rallied 40–55% over the past year, supported by rising order backlogs and robust defense cash flows. Boeing has lagged that cohort, reflecting its mixed commercial track record and investor caution after a series of safety and certification setbacks.

Is the Boeing Defense Budget story changing with Iran?

The near‑term macro backdrop for the Boeing Defense Budget has shifted markedly with the ongoing conflict involving Iran. The Pentagon is seeking an additional $200 billion in supplemental funding to support operations and replenish key weapons systems, on top of an already elevated national defense framework that totals around $1 trillion for fiscal 2026 when including prior supplemental measures. If approved, the extra request would lift total defense outlays for 2026 to roughly $1.2 trillion and could reduce the need for an extreme one‑year jump in the fiscal 2027 baseline budget.

For defense contractors, that kind of spending trajectory — implying 5–10% annual growth over the next few years — is supportive. Investors have seen that dynamic in the 48% twelve‑month surge of the iShares U.S. Aerospace & Defense ETF and strong gains in names like Lockheed Martin and RTX. Yet Boeing’s share price is not reflecting the full potential of an expanding Boeing Defense Budget opportunity, with Iran‑related uncertainty, higher oil prices and company‑specific risk keeping a lid on sentiment.

Why is Boeing lagging other defense names?

From an equity‑market standpoint, Boeing is increasingly viewed as a special situation rather than a pure defense winner. Investors Business Daily recently highlighted how defense stocks such as General Dynamics, Howmet, Karman, Lockheed and RTX are clear winners in the current conflict‑driven tape, while Boeing lags despite its large defense and services segments. The underperformance underscores concerns that any Boeing Defense Budget upside could be partially offset by weaker execution, legacy cost overruns and the heavy lift required to restore margins in Commercial Airplanes.

That said, not all institutional flows are negative. MarketBeat reported that FNY Investment Advisers significantly increased its stake in Boeing to 11,557 shares, making it the firm’s 15th‑largest position. Hedge fund interest has been creeping higher as some managers position for a multi‑year recovery, a trend also noted by Insider Monkey, which framed Boeing as a high‑risk, high‑reward play relative to high‑growth AI names like NVIDIA.

What do analysts say about Boeing’s outlook?

On the Street, the tone has turned more constructive but remains nuanced. BofA Securities reiterated its positive stance on Boeing this week, emphasizing steady production plans and upside from defense even as near‑term margin pressure persists. The bank’s analysts see long‑term cash flow leverage as 737 and 787 build rates rise and as defense contracts tied to the Boeing Defense Budget begin to flow more meaningfully through earnings.

Other research outfits echo the long‑duration angle. A recent Seeking Alpha analysis argued that investors should “ignore fuel price spikes” and treat Boeing as a decade‑long play, underpinned by accelerating commercial output, double‑digit growth in defense and services, and a deep backlog that provides strong revenue visibility. At the same time, some managers remain cautious, pointing to ongoing legal issues, a delayed profitability timeline in the commercial division, and the risk that persistent quality problems could push airlines toward rivals like Airbus or temper future orders from key customers such as Apple‑heavy corporate travel partners and global carriers.

How are operations and certification milestones progressing?

Operationally, there are signs of progress that could eventually reinforce the Boeing Defense Budget bull case by stabilizing cash flows. Reuters reported that the FAA has allowed Boeing’s long‑delayed 777‑9 wide‑body to move into the fourth phase of certification testing, a key step toward eventual entry into service later this decade. Separately, Ryanair’s CEO said he expects certification of Boeing’s 737 MAX 10 in the third quarter, with deliveries on time early next year — a critical validation for the company’s narrow‑body franchise.

Commercial demand remains healthy. United Airlines is rolling out a premium‑heavy 787‑9 Dreamliner with a new elevated interior on long‑haul routes from San Francisco to Singapore and London, reinforcing the value of Boeing’s wide‑body platform even as the airline navigates delivery delays and higher fuel costs. For investors with diversified portfolios that include travel names like Tesla‑exposed EV suppliers and large‑cap tech such as NVIDIA, Boeing offers an orthogonal cyclical lever tied to global traffic and defense budgets rather than consumer hardware cycles.

Related Coverage

For a deeper dive into how recurring 737 MAX problems are shaping sentiment, readers can review the recent analysis “Boeing 737 MAX issues: Delivery Warning Jolts Investors,” which explores whether repeated quality and delivery setbacks are turning a long‑awaited recovery into yet another test of patience for shareholders. The article, available at Boeing 737 MAX issues: Delivery Warning Jolts Investors, also examines how these issues intersect with broader portfolio decisions in the aerospace and defense sector.

Because the 737 MAX story is central to both Boeing’s commercial franchise and its ability to capitalize on a larger Boeing Defense Budget, the same piece is equally relevant as a sector look, contrasting Boeing’s challenges with the smoother execution seen at other defense‑exposed manufacturers. Investors can access that broader industry lens via this sector‑focused review of Boeing 737 MAX issues and delivery risks, which helps place Boeing’s risk‑reward profile in context against faster‑growing peers.

Boeing is evolving into a long-duration, high-conviction idea for investors who can look through near-term noise and focus on the combined power of defense budgets and a recovering jet cycle.— Unnamed Wall Street portfolio manager

In sum, Boeing sits at the intersection of market volatility, war‑driven tailwinds and company‑specific repair work, with the Boeing Defense Budget theme offering a critical offset to commercial and macro headwinds. For U.S. investors constructing diversified portfolios, the stock remains a high‑beta bet on both elevated defense spending and a multi‑year normalization of jet deliveries. The next few quarters of execution — across certification, margins and Pentagon awards — will determine whether today’s Boeing Defense Budget optimism translates into sustainable upside for the shares.