Can the new Boeing Pentagon Deal finally shift the BA story from crisis headlines back to long-term defense cash flows?

How does the Boeing Pentagon Deal change the story?

The centerpiece of the Boeing Pentagon Deal is a seven‑year framework with the U.S. Department of Defense to roughly triple output of Patriot Advanced Capability‑3 (PAC‑3) Missile Segment Enhancement seekers. These guidance units are a critical component of Lockheed Martin’s interceptors used in layered air and missile defense, including against ballistic and emerging hypersonic threats. Boeing will ramp production out of its Huntsville, Alabama campus, where it has already invested more than $200 million since 2024 and added a new 35,000‑square‑foot facility.

The framework is part of Washington’s broader “Arsenal of Freedom” initiative to strengthen the U.S. defense industrial base and secure long‑lead components. While specific revenue numbers have not been disclosed, the commitment to triple capacity over seven years provides a rare level of volume visibility in defense hardware. For investors, the Boeing Pentagon Deal signals that defense may increasingly offset volatility in the commercial jet business, especially as BA continues to work through 737 MAX reputational and regulatory legacy issues.

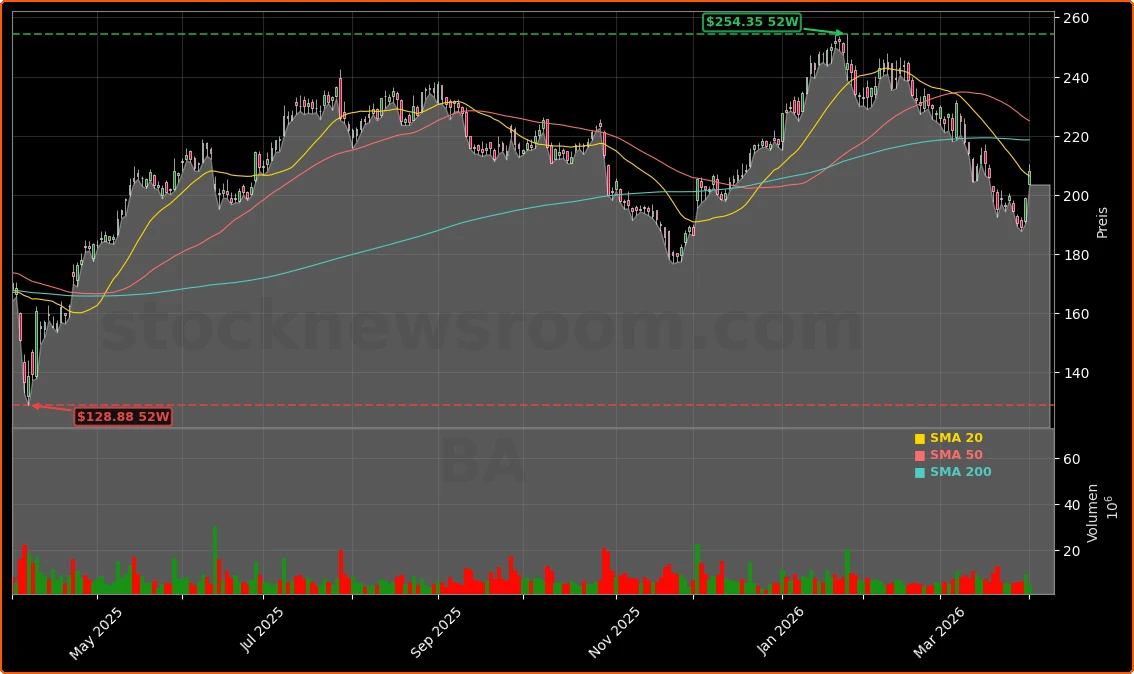

Market reaction has been swift. With the stock up about 4.6% to $208.10 and extending pre‑market gains, Boeing has become one of the biggest contributors to the Dow Jones Industrial Average’s rally on Wednesday. The move follows a difficult March, when the shares fell double digits, suggesting the defense news is helping investors re‑anchor around fundamentals and contract backlog rather than headlines alone.

What does the Pentagon pact mean for Boeing Defense?

The Boeing Pentagon Deal also reinforces the strategic relevance of Boeing Defense, Space & Security at a time when geopolitical risk remains elevated from Eastern Europe to the Middle East. Beyond PAC‑3, Boeing already maintains deep ties to the U.S. Air Force and allied militaries through platforms like the B‑52 Stratofortress, which continues to receive structural and systems upgrades and is expected to stay in service into the 2050s. Recent B‑52 missions over Iran have reminded markets that legacy airframes can still generate modernization work and steady revenue.

In parallel, Boeing’s Australian defense unit has teamed up with Rheinmetall in Germany to offer the MQ‑28 Ghost Bat autonomous combat aircraft for the Bundeswehr by 2029. Under that arrangement, Rheinmetall will serve as system manager while Boeing supplies the airframe and integration expertise. Together with the PAC‑3 seeker expansion, these moves show Boeing pivoting toward next‑generation systems such as collaborative combat aircraft and advanced missile defense, rather than relying solely on traditional manned fighters and transports.

For U.S. investors who track defense peers like Lockheed Martin, Northrop Grumman and General Electric’s aerospace arm, the Huntsville ramp‑up highlights how industrial capacity is becoming a key competitive moat. Management has emphasized that additional investments tied to the framework should be cash‑neutral, suggesting Boeing can scale without putting significant incremental strain on its balance sheet.

How are Wall Street and institutions reacting to Boeing?

The Boeing Pentagon Deal arrives alongside a constructive shift in analyst sentiment. Wells Fargo analyst Matthew Akers initiated coverage of Boeing with an “Overweight” rating and a $250 price target, implying more than 20% upside from current levels. Akers points to the recovery in free cash flow as aircraft production normalizes and sees the defense backlog as an important stabilizer. For investors comparing BA to high‑growth names like NVIDIA or Tesla, the appeal here is less about explosive revenue growth and more about multi‑year visibility and operating leverage as rates of production increase.

Institutional investors have also been quietly adding exposure. Nisa Investment Advisors recently grew its Boeing stake by about 4.7% to nearly 197,000 shares, while Capital Advisors Inc. OK increased its position by roughly 19%, now holding more than 275,000 shares. These moves indicate that large asset managers view the recent pullback as an opportunity to average into a long‑term aerospace and defense recovery theme rather than a reason to exit.

On the legal front, a federal appeals court decision to allow the Department of Justice to dismiss a criminal case tied to the 737 MAX tragedies has removed a significant overhang. While civil litigation and regulatory scrutiny are not fully behind the company, the affirmation of the deferred prosecution agreement reduces tail risk and helps management stay focused on operations, including high‑priority contracts like the Boeing Pentagon Deal.

How does Boeing stack up against global aerospace rivals?

From a competitive standpoint, Boeing’s defense momentum complements its progress in commercial aviation versus Airbus. So far this year, Boeing has outperformed Airbus on net orders and deliveries, driven by strong demand for widebody jets at a time when engine constraints have capped Airbus’s delivery growth. Both manufacturers still carry large backlogs and pricing power, but Boeing’s incremental wins in defense, such as the PAC‑3 seeker expansion, provide a diversification edge that some civilian‑focused peers lack.

On Wall Street, Boeing remains tightly correlated with the S&P 500, and options markets are tracking that linkage closely. Yet the stock’s recent bounce to around $208, still well below prior cycle highs, suggests investors are not pricing in an overly optimistic scenario. Instead, the market seems to be recognizing Boeing as a turnaround and cash‑flow recovery story under CEO Kelly Ortberg, with defense contracts building a more predictable base while commercial and space programs like NASA’s SLS and Artemis evolve.

For U.S. investors balancing growth and defense exposure in their portfolios, Boeing now sits at an intersection: it offers cyclical upside if global air travel and widebody demand remain strong, and a more resilient floor supported by long‑dated Pentagon and allied contracts.

Related Coverage

Investors who want a deeper dive into how defense spending trends shape the stock can read Boeing Defense Budget -2.3%: Dow Plunge Warning for BA, which analyzes whether recent weakness in the share price is masking a stronger long‑term defense budget story. For a broader sector comparison, General Electric Aerospace -3.1%: Sentiment vs. Fundamentals looks at how another major U.S. aerospace player is navigating sentiment swings versus its underlying fundamentals.

With this framework, we’ll be able to produce and deliver more advanced seekers and enhance our military’s advantage.— Steve Parker, President and CEO, Boeing Defense, Space & Security

The Boeing Pentagon Deal to triple PAC‑3 seeker production underscores how defense is becoming a central pillar of Boeing’s multi‑year recovery. For Wall Street, the combination of a major long‑term Pentagon framework, improving legal visibility and fresh “Overweight” ratings supports the view that BA can compound free cash flow as execution improves. The next few quarters of deliveries, margin progress and contract announcements will show whether this renewed optimism is justified, but for now the Boeing Pentagon Deal is a clear signal that the company’s defense engine is shifting into a higher gear.