Is the latest Carvana Short Report a temporary scare or the start of a deeper unwind in one of Wall Street’s wildest rebounds?

Why is Carvana’s stock sliding again?

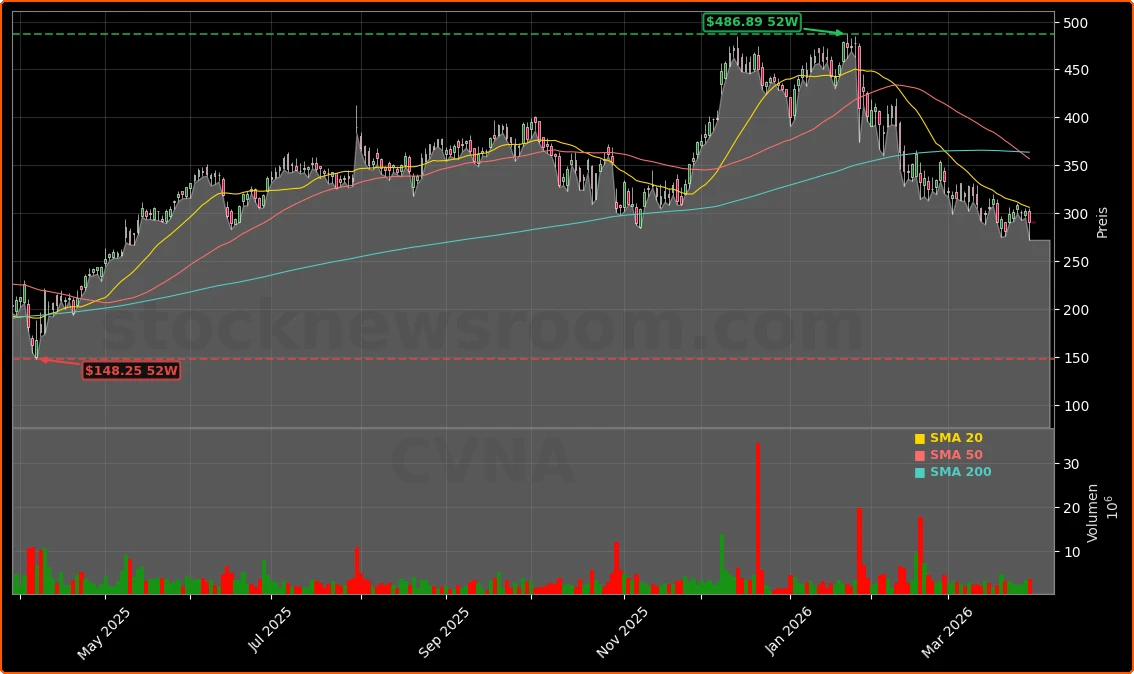

Carvana Co. (CVNA) finished Monday’s session on the NYSE down about 3.7% at $290.80, retreating further from its 52-week high of $486.89. After hours, the stock slipped another fraction to around $290.20. That leaves Carvana down roughly a third year to date, even after reporting record 2025 revenue of $20.32 billion and 43% retail unit growth.

The immediate catalyst is a new Carvana Short Report from Temple 8 Research, which focuses on weakening unit economics and margins. At the same time, investors are digesting a planned 5‑for‑1 forward stock split that some see as cosmetic, coming after a huge multi‑year rebound and ahead of potentially tougher credit conditions for auto buyers. The combination has turned CVNA back into a high‑beta stress test for risk appetite on Wall Street and the NYSE’s consumer discretionary cohort.

For U.S. portfolios that already lived through Carvana’s boom‑and‑bust cycle, the question is whether the current drawdown is another shakeout in a long‑term turnaround story or an early warning that short-seller criticism is finally biting into the bull thesis.

What is in the new Carvana Short Report?

The latest Carvana Short Report from Temple 8 Research zeroes in on two key metrics that have long anchored the Carvana bull case: gross profit per unit (GPU) and EBITDA margin. Temple 8 argues that recent quarters show falling GPU and a declining EBITDA margin, suggesting that the company’s aggressive growth is not translating into improving profitability.

Short sellers also highlight the company’s dependence on auto financing, particularly to subprime and near‑prime borrowers. In a higher‑rate environment, funding those loans and securitizing them at attractive yields becomes more difficult. If credit spreads widen or investor appetite for auto ABS weakens, Carvana’s ability to convert originations into cash could be pressured, potentially forcing the company to lean more heavily on capital markets precisely when sentiment is turning cautious.

The Carvana Short Report revives themes that have stalked the stock for more than a year. Gotham City Research had previously accused Carvana of overstating earnings by more than $1 billion across 2023 and 2024, and several law firms have pursued securities class action investigations. Carvana has rejected those accusations as “inaccurate and intentionally misleading,” but the pattern of forensic scrutiny keeps a cloud over the name and makes institutional holders quicker to hit the sell button when new bearish analysis appears.

Temple 8’s timing is critical. With CVNA trading on a rich earnings multiple after an 8,000%+ rebound from its lows, any evidence of margin compression or weaker unit economics can trigger sharp de‑risking by hedge funds and momentum‑oriented investors.

How does the 5-for-1 stock split fit into the picture?

Adding fuel to the debate is Carvana’s plan for a 5‑for‑1 forward stock split of its Class A and Class B common shares, subject to shareholder approval at a virtual annual meeting on May 5, 2026. The announcement helped push the stock up about 7.4% on Friday, as some traders read the move as a sign of management confidence and a nod to broadening ownership among employees and retail investors.

However, Monday’s reversal shows that sentiment has quickly flipped. The stock is well off its highs, and skeptics argue the split looks more like optics management than a reflection of durable profitability. In a market that has seen heavily shorted, high‑multiple names trade erratically, a forward split can attract additional speculative flows without changing fundamentals—a pattern investors have already witnessed in companies like Tesla and, in the tech space, NVIDIA.

Bulls counter that making shares more affordable on a per‑share basis could deepen liquidity and drive broader participation in incentive plans, aligning employees more closely with long‑term value creation. Recent proxy materials outline a new 2026 Omnibus Incentive Plan designed to tie executive and staff compensation more tightly to long‑run performance metrics, following a year of significant revenue and EBITDA growth.

Still, with the Carvana Short Report questioning the trajectory of GPU and margins, the split is being interpreted less as a victory lap and more as a stress test of investor confidence at elevated valuations.

Are macro and financing headwinds getting worse?

Beyond company‑specific controversy, macro conditions are starting to bite. Elevated interest rates are making auto loans more expensive, especially in the subprime segment that Carvana relies on for a meaningful portion of its customer base. Tightening underwriting standards mean fewer buyers qualify, which can cap unit growth and force more discounting to move vehicles.

Consumer sentiment remains fragile: the University of Michigan Consumer Sentiment Index was recently measured at 56.6, far below the 80‑point level often considered a neutral backdrop for big‑ticket purchases. At the same time, WTI crude around $102 per barrel is raising ownership costs for internal combustion vehicles, denting affordability perceptions at the margin and affecting demand for used cars.

Carvana’s logistics‑heavy model makes it particularly sensitive to fuel and transport costs. Most vehicles are hauled significant distances to customers, so higher oil prices can pressure fulfillment costs and erode GPU just as credit gets tighter. That combination is a key pillar in the bear case gaining traction in the wake of the Carvana Short Report.

For context, other consumer and auto‑related names—ranging from legacy OEMs to high‑growth innovators like Tesla—are also facing a more demanding macro tape. The difference is that Carvana sits outside major indexes like the S&P 500, which can exacerbate volatility as hedge funds and long‑only managers trade it more opportunistically.

Do analysts still back Carvana?

Despite the latest selloff, Wall Street’s published ratings remain broadly constructive. Bank of America Securities has reiterated a Buy rating on CVNA with a $400 price target, pointing to Carvana’s record 2025 revenue and the potential to emerge as the top independent used‑car dealer in the United States. Across the street, the consensus analyst target is reported at about $428.50, with roughly 18 Buy ratings against just 1 Sell.

Supportive analysts emphasize several points. First, Carvana’s long‑term plan calls for scaling to 3 million annual retail units at a 13.5% adjusted EBITDA margin within four to nine years, which, if achieved, would significantly expand earnings power relative to today’s levels. Second, management has spent the last three years refocusing on operational efficiency—reconditioning capacity, logistics density, and marketing ROI—after the near‑bankruptcy scare earlier in the decade.

Bullish commentators also argue that GPU headwinds are at least partly cyclical, reflecting used‑car pricing normalization after an extraordinary pandemic‑era spike. Some research suggests those pressures could ease as industry inventory stabilizes, much as chip‑driven supply disruptions are gradually normalizing for auto OEMs and consumer tech leaders like Apple.

Still, a stock can trade poorly even with bullish reports on the desk. CVNA now sits well below its 50‑day moving average around $375.85, signaling technical damage that may need time to repair. High‑growth names with contested narratives, such as Carvana, often move in multi‑month waves as short interest, options positioning, and macro news interact.

How should U.S. investors frame the risk-reward now?

For U.S. investors, the current setup around CVNA is a classic battleground case. On one side, you have powerful top‑line growth, a disruptive digital model, and vocal backing from large banks like Bank of America. On the other, you have a fresh Carvana Short Report, legacy accounting allegations, tightening credit, and a stock split whose timing raises eyebrows just as the stock is sliding.

Portfolio construction matters here. For diversified investors in broad index ETFs tracking the S&P 500 or Nasdaq, Carvana is largely a side show—its absence from major benchmarks means it won’t move core retirement holdings the way a mega‑cap like NVIDIA or Apple might. But for active stock pickers, hedge funds, and options traders, CVNA’s volatility can significantly swing performance and requires a strong stomach.

Key variables to watch over the next several weeks include any formal response from management to Temple 8’s claims, additional data points on GPU and EBITDA margin in upcoming updates, trends in auto loan delinquencies, and how the shareholder vote on the 5‑for‑1 split plays out. Whether the stock can stabilize above recent support near $275 will also be important for technically minded traders.

Related Coverage

For a deeper dive into the mechanics and timing of the 5‑for‑1 split, including what it means for share count and perceived affordability, read Carvana Stock Split 5-for-1: Rally Signal or Risk?. That analysis explores whether the split marks a new leg higher after CVNA’s massive rebound or a late‑cycle warning sign.

Investors following the broader auto and mobility space may also want to look at EV leader Tesla’s changing risk profile. Our piece Tesla Robotaxi Shock: Is the Q1 2026 Delivery Bar Too High? examines whether the company’s robotaxi and Cybercab initiatives can offset slowing EV growth and what that might mean for sentiment across the wider transportation sector.

In the end, the Carvana Short Report has re‑focused the market on the tension between Carvana’s explosive growth and the fragility of its financing‑led model. For U.S. investors, CVNA remains a high‑risk, high‑reward name where conviction on unit economics and credit resilience will determine whether recent weakness is a buying opportunity or a warning to stay on the sidelines. The next catalysts—management’s response, macro data, and the May 5 split vote—will show whether the bull or the bear camp gains lasting control.