Can the Chevron Energy Strategy turn Gulf chokepoint risk and volatile oil prices into reliable cash flows through 2030?

How is Chevron handling the Strait of Hormuz risk?

Chevron Corporation CEO Mike Wirth warned this week that the closure of the Strait of Hormuz is already having “very real, physical” effects on global supply that are not fully reflected in oil futures curves. The Chevron Energy Strategy currently benefits from tight physical markets, with U.S. producers generally viewed as more reliable than many Middle Eastern exporters. MarketWatch has highlighted that the Iran conflict underscores structural advantages for American oil and gas suppliers, particularly for LNG exports, a space where Chevron is a key player.

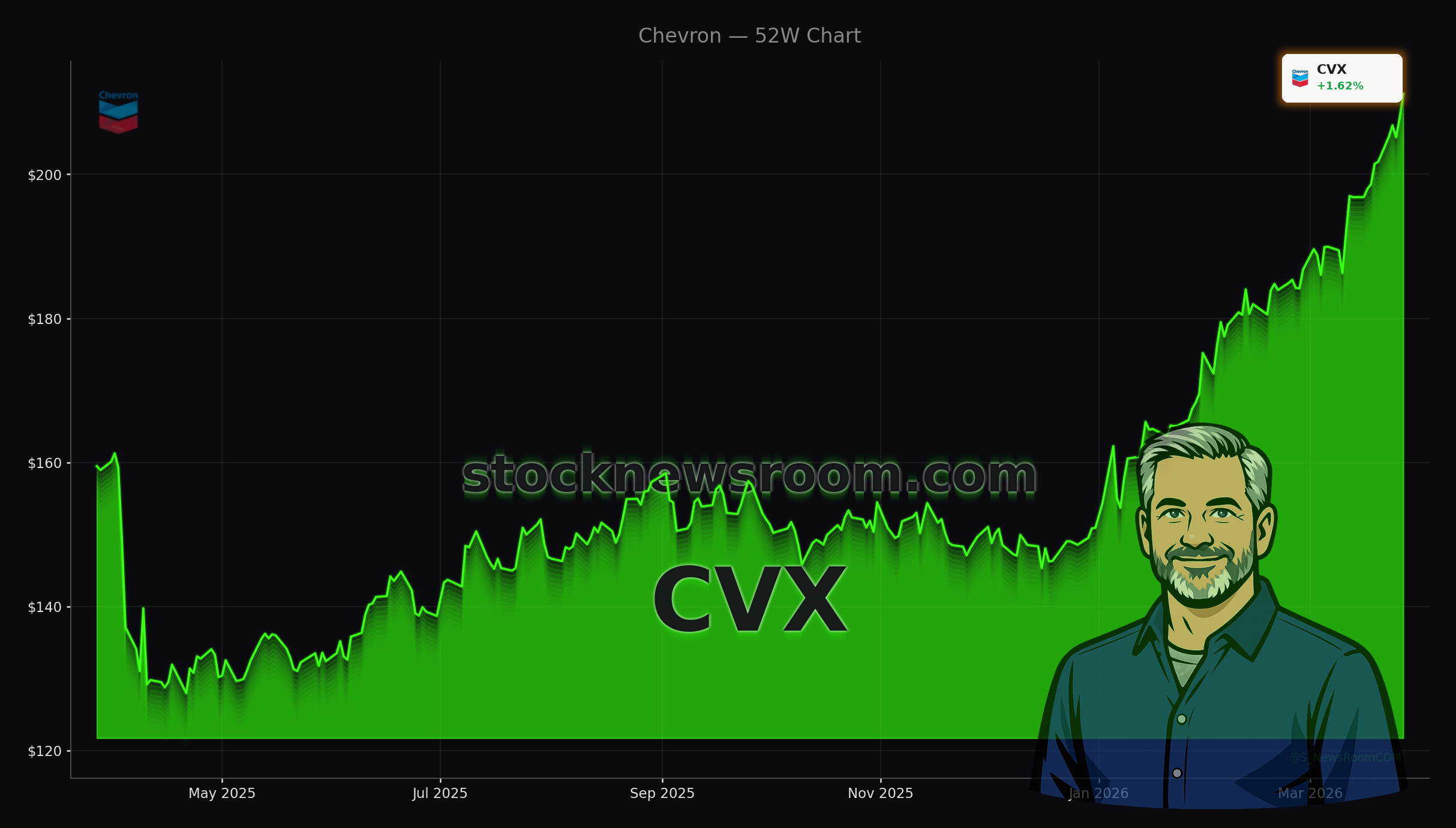

Short-term, traders on the NYSE have pushed CVX sharply higher in March as geopolitical risk premiums expanded. Zacks notes that Chevron’s combination of earnings momentum and price strength now screens well in its style scores, attracting growth, value and momentum investors across the S&P 500.

What makes Chevron’s cash flows stand out?

At the core of the Chevron Energy Strategy is a portfolio rebuilt to thrive at lower oil prices. Over recent years Chevron has sold low-margin assets and doubled down on low-cost, high-margin resources, including the Hess acquisition, giving it one of the sector’s lowest corporate breakevens. Management says it can fully fund capex and its dividend at oil below $50 per barrel through 2030.

With large growth projects completed in 2025, Chevron expects roughly $12.5 billion in additional annual free cash flow at $70 oil versus its 2025 base, potentially more if prices stay elevated. That underpins $10–$20 billion in annual share repurchases, continued dividend growth and balance-sheet strength even if Middle East tensions ease. TradingKey recently flagged this mix of geopolitical tailwinds and capital returns as a key driver behind the stock’s latest 3%+ daily surge.

How does Chevron stack up for U.S. portfolios?

Despite a valuation near 31 times earnings, Chevron’s dividend of $7.12 per share (about 3.3% yield) has risen for 39 consecutive years, appealing to retirees who might otherwise focus on defensive payers like Apple or high-growth names such as NVIDIA and Tesla. With gasoline vehicles still over 90% of the global fleet and oil and gas supplying about 70% of U.S. energy use, the Chevron Energy Strategy assumes long-lived demand even as renewables expand.

For income-focused investors comparing Chevron with peers like Exxon Mobil or pipeline giant Enbridge, the combination of low breakevens, double-digit targeted free cash flow growth through 2030 and a proven dividend policy stands out in the S&P 500 Energy sector.

Related Coverage

For a deeper dive into how geopolitics and oil price shocks are shaping Chevron’s positioning, read “Chevron Geopolitics Rally: Oil Shock, Jobs and Risk Shift”, which examines how the company may be turning regional conflict into a strategic edge on Wall Street. Investors also looking at the clean-energy side of the ledger can explore hydrogen player Plug Power in “Plug Power Turnaround: -2.7% Shock After First Margin Boost”, a useful contrast to Chevron’s fossil-fuel-focused approach.

There are very real, physical manifestations of the closure of the Strait of Hormuz that are working their way around the world and through the system that I don’t think are fully priced into the futures curves on oil.— Mike Wirth, CEO of Chevron Corporation

Overall, the Chevron Energy Strategy marries geopolitical resilience with low-cost production and an elite dividend record. For U.S. portfolios seeking a blend of income and inflation protection, Chevron remains a core energy holding. The next quarters will show whether free cash flow growth and buybacks can sustain CVX’s rally even if Middle East risk premiums recede.