Is the Chevron Oil Price Plunge just a knee-jerk reaction to cease-fire headlines, or a warning sign for energy bulls?

Why did Chevron drop on the cease-fire news?

The immediate catalyst for the Chevron Oil Price Plunge was a roughly 15% slide in crude prices after Washington and Tehran agreed to a two-week cease-fire that includes reopening traffic through the Strait of Hormuz. Brent and WTI futures fell back toward the mid-$90s per barrel, down from peaks around $113 as of April 7, unwinding part of the war premium that had built up in recent weeks.

Energy stocks were the only major laggard on an otherwise strong day for the broader market, with the S&P 500 energy sector down about 4.6% in afternoon trading. Chevron Corporation was hit alongside peers, with Exxon Mobil off around 5% and Occidental Petroleum posting even deeper losses. The Chevron Oil Price Plunge effectively erased about a month of gains for the stock and capped a volatile stretch in which CVX had surged roughly 28% year to date before the pullback.

Investors had been buying integrated oil majors as a straightforward hedge on escalating conflict and constrained supply. As the immediate risk premium in crude receded, those same positions were quickly unwound, leading to outsized moves in both oil benchmarks and energy equities.

Is Chevron’s fundamental story really broken?

Despite the shock of the Chevron Oil Price Plunge, the underlying environment for the company remains more favorable than the headline move suggests. Even after the drop, crude around $95 a barrel still trades at a substantial premium to the roughly $58–$68 range that prevailed through most of 2025. At those levels, Chevron’s upstream operations continue to generate attractive cash flows.

Refining economics also look constructive. Industry data show the popular 3-2-1 crack spread — a proxy for refining margins — elevated near $42 per barrel, well above early-2025 levels. That backdrop supports Chevron’s downstream and chemicals businesses, cushioning earnings even if spot crude fails to retest recent highs above $110.

Operationally, Chevron has leaned into growth. Full-year 2025 worldwide production climbed 12% to a record 3,723 thousand barrels of oil equivalent per day, driven by the Hess acquisition, a ramp-up in Kazakhstan’s TCO project, and milestone output of 1 million BOE per day in the Permian Basin. The company is also accelerating a structural cost reset, targeting $3–$4 billion of reductions by the end of 2026 after delivering $1.5 billion in savings last year.

That said, the balance sheet bears watching. Chevron’s net debt ratio rose to 15.6% from 10.4% following the Hess deal, and 2025 shareholder returns of $27.1 billion exceeded free cash flow of $16.6 billion, signaling reliance on the balance sheet that becomes more sensitive when oil prices fall.

How does Chevron stack up against Exxon Mobil?

The Chevron Oil Price Plunge also throws the contrast with Exxon Mobil into sharper relief. Both supermajors enjoyed a powerful first quarter, with Exxon stock up about 41% and Chevron roughly 36% in that period before today’s reversal. Each raised dividends 4% and beat fourth-quarter EPS estimates, but their cash-flow profiles diverge.

Exxon generated about $26.1 billion in full-year free cash flow in 2025 and covered its dividend roughly 3.0 times with operating cash flow. Chevron, by comparison, produced $16.6 billion of free cash flow and covered its dividend about 1.30 times. Exxon also boasts a 43-year dividend growth streak versus Chevron’s 39 years, giving Exxon more visible cushion if crude remains under pressure.

Still, Chevron’s higher raw yield — recently around 3.4%–3.6% with a quarterly dividend of $1.78 per share — remains attractive for income-focused investors. The company is also pushing diversification beyond traditional oil and gas faster than some peers, including investments in data-center power solutions, lithium acreage in the Smackover Formation, and renewable diesel expansion at Geismar.

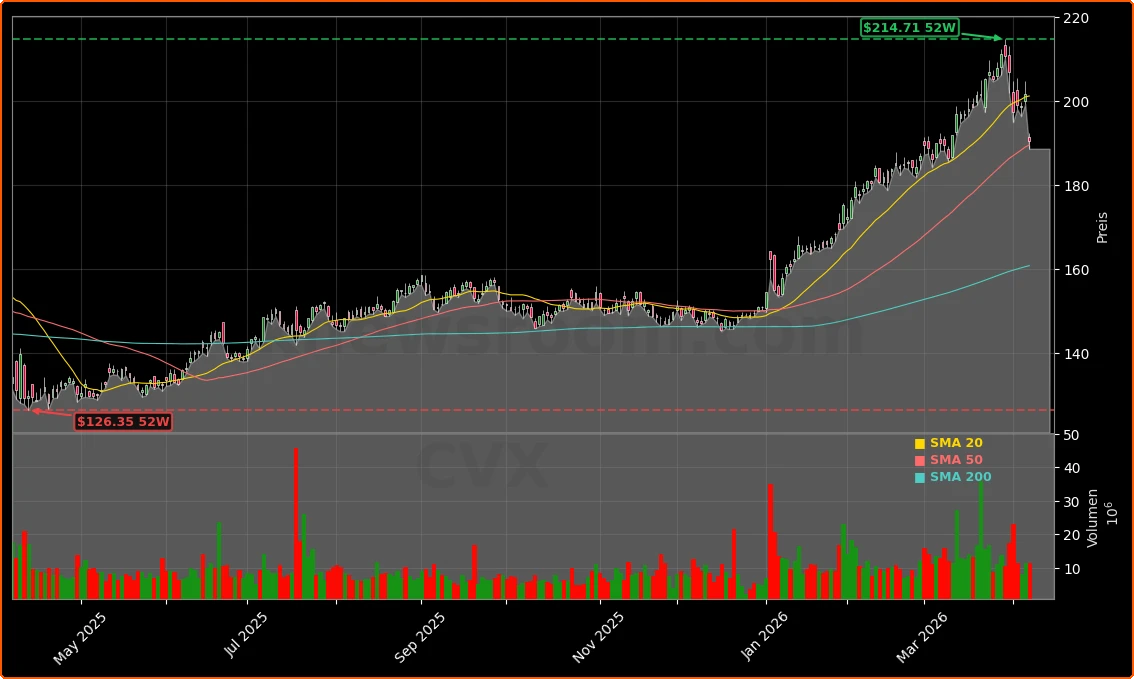

In terms of momentum, Chevron’s one-day loss of 5.52% to $190.39 comes just a day after it outperformed competitors, closing Tuesday at $201.54 and sitting only about 6% below its 52-week high reached in late March. The latest selloff brings the stock roughly $20 off that peak but does not mark a new low or structural break in the long-term chart.

What are analysts saying after the selloff?

Wall Street research has been measured rather than panicked in response to the Chevron Oil Price Plunge. CFRA reiterated its Hold opinion on Chevron and maintained a 12-month price target of $165, which implies modest downside from recent levels and signals that the firm sees the stock as fairly valued after its multi-month rally. Other large banks such as Goldman Sachs, Morgan Stanley, and Citigroup have previously highlighted integrated oil majors as a key way to gain exposure to higher-for-longer crude, but the cease-fire and reopening of Hormuz could prompt revisions to their oil-price decks and energy weighting recommendations in the coming weeks.

Trading desks also emphasize that the agreement in the Persian Gulf is a cease-fire, not a comprehensive peace settlement. Several sticking points remain over the long-term control and security regime in the Strait of Hormuz, and supply from the region may take time to normalize even if hostilities stay contained. That lingering uncertainty keeps Chevron, Exxon, and other supermajors in play as partial hedges against renewed volatility, particularly for diversified portfolios dominated by high-growth names like NVIDIA, Tesla, and Apple.

Related Coverage: How does this fit into the broader energy story?

For a deeper dive into how Chevron is trying to convert wartime tailwinds and the AI infrastructure boom into a durable advantage, readers can revisit our analysis of the company’s strategic positioning in Chevron Energy Project -1.8%: AI Power and War Shock. That piece explores how Chevron aims to supply reliable power to data centers while managing war-driven volatility.

Investors comparing traditional oil exposure with more speculative clean-energy plays should also look at our recent feature on Plug Power, Plug Power Turnaround -9.1%: Rally Setup or Crash Warning for PLUG?. Together, these articles frame the trade-offs between established cash-generating giants like Chevron and higher-risk transition stories in the hydrogen and renewables space.

The Chevron Oil Price Plunge underscores how quickly sentiment can shift when geopolitics and commodities collide, but it does not erase the company’s scale, dividend track record, or multi-year growth projects. For U.S. investors, the selloff is a reminder to stress-test portfolio assumptions about oil prices and conflict risk rather than to abandon the sector outright. The next few months of price action in crude and the upcoming earnings season will show whether this is a temporary air pocket or the start of a more sustained re-rating for Chevron and its energy peers.