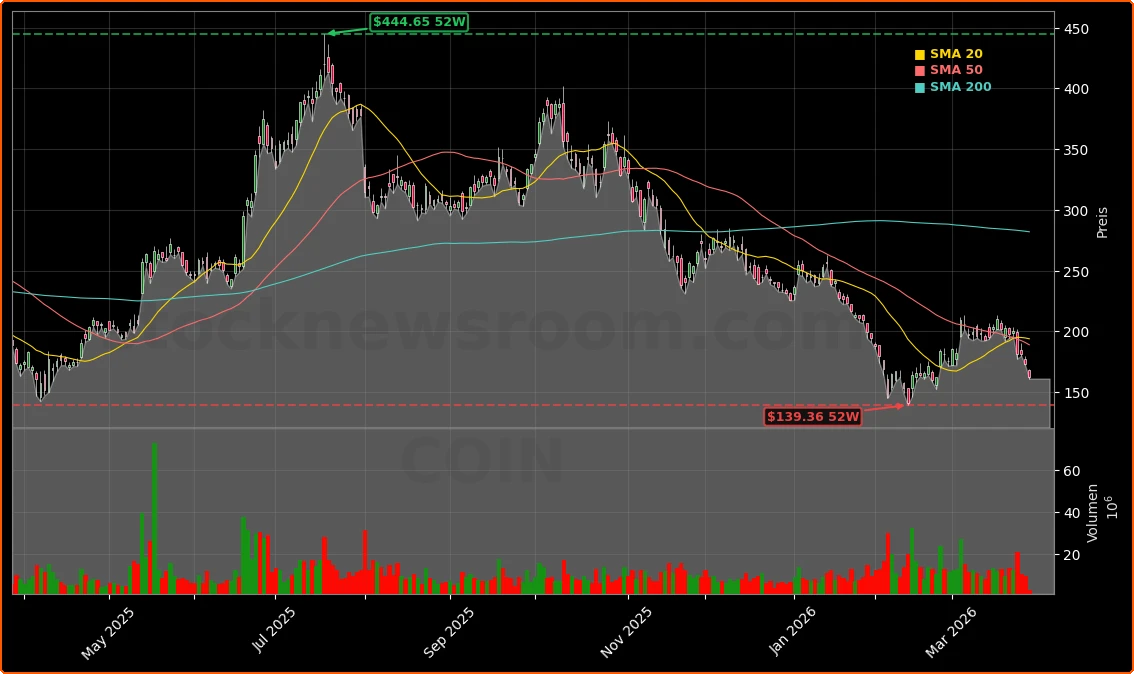

Is the Coinbase Crypto Strategy unlocking new profit pools or setting up investors for a regulatory and leverage shock?

Is Coinbase blocking US crypto rules?

At the core of the current Coinbase Crypto Strategy is a bruising fight over stablecoin rewards in the Senate’s CLARITY Act. Large banks want to shut down passive yield on idle stablecoin balances, arguing exchanges enjoy a regulatory loophole, while crypto platforms warn that banning rewards would cripple user acquisition and entrench traditional finance. Earlier drafts that effectively outlawed such yields wiped roughly 10% off COIN and about 20% off stablecoin issuer valuations in a single session, underscoring how tightly regulation is linked to the business model.

Recent reports suggest Coinbase representatives still view the latest compromise language as too restrictive, even as White House advisers downplay talk that the company is single‑handedly blocking the bill. For investors, the outcome will determine whether stablecoin float and rewards remain a scalable profit pool or shrink into a thin‑margin utility, with direct read‑through for COIN’s long‑term multiple.

How is Coinbase reshaping crypto use in housing?

Beyond Washington, the Coinbase Crypto Strategy is pushing deeper into mainstream credit markets. A new partnership with Better Home & Finance lets U.S. homebuyers use bitcoin and USDC held at Coinbase as collateral for separate loans funding their down payments, while the primary mortgage remains a conventional Fannie Mae‑eligible loan. Borrowers avoid liquidating crypto, potentially sidestepping immediate capital‑gains taxes and preserving upside if prices recover.

The trade‑off is leverage and cost: buyers stack a secured crypto loan on top of a standard mortgage, with rates typically 0.5 to 1.5 percentage points higher than traditional 30‑year products. Still, in a market where spot bitcoin ETFs and institutions are seeking new yield channels, this structure pushes Coinbase closer to a hybrid between a regulated exchange and a fintech credit platform, a positioning distinct from pure‑play crypto miners or high‑growth names like Tesla and NVIDIA.

What does the GameStop deal signal for Coinbase?

Another pillar of the Coinbase Crypto Strategy is acting as a structured‑products venue for corporate treasuries. GameStop moved roughly $324 million in bitcoin from its wallets to Coinbase, not to dump it, but to pledge 4,709 BTC into a covered‑call program. By selling call options with strike levels near $105,000–$110,000 per bitcoin, GameStop converted volatile holdings into about $368 million in cash premiums plus a digital‑asset receivable, while capping upside if bitcoin rockets past six figures.

The arrangement gives Coinbase considerable flexibility to rehypothecate or sell the pledged BTC, explaining why GameStop now accounts for the coins off‑balance‑sheet. For investors, that means some of the convex upside in future bitcoin bull runs may accrue to Coinbase and its counterparties rather than to corporate “bitcoin proxy” equities. It also underlines how Coinbase is becoming a core infrastructure layer for advanced options, lending, and treasury strategies that traditional brokers and even Big Tech names like Apple do not yet offer.

Related Coverage: Regulatory risk around stablecoins has already hit COIN once this week. A deeper look at how rewards language and bank pressure could reshape yields and valuation appears in Coinbase Stablecoin Regulation -7.2% Crash Sparks Debate. For a broader view of crypto market sentiment and how another major token is reacting to legal and structural shocks, see Ripple Market Analysis: Is the $10 XRP Dream or Crash Risk?, which examines whether XRP’s recent slide is consolidation or a warning for high‑beta crypto plays.

In sum, the Coinbase Crypto Strategy now spans Washington lobbying, mortgage innovation, and complex bitcoin option structures for corporates, making COIN a leveraged but more diversified bet on digital assets than owning tokens outright. For U.S. investors, the key questions are whether stablecoin rewards survive, whether crypto‑backed lending gains traction, and how much upside Coinbase can capture from institutional bitcoin adoption. The next moves in Congress and in corporate treasury demand will determine whether this strategy translates into durable revenue growth for long‑term shareholders.