How long can the Federal Reserve’s monetary policy remain independent as Trump’s tariff plans simultaneously fuel inflation, markets, and the election campaign?

How is the Fed responding to Trump’s tariff offensive?

President Trump has aggressively defended his tariff policy during the longest-ever televised State of the Union address. Tariffs of up to 10% on broad import baskets are expected to generate hundreds of billions of dollars and potentially replace parts of the income tax in the long term. At the same time, the administration is working to raise the tariff level to 15% in certain areas. For the Federal Reserve’s monetary policy, this strategy is delicate: economists estimate that the tariffs could increase the Fed’s preferred PCE inflation by about 0.5 percentage points, complicating further interest rate cuts.

Fed officials point out that core inflation is still hovering around 3%, well above the 2% target. Chicago Fed President Austan Goolsbee explicitly warns against settling at 3%. In this environment, additional rounds of tariffs would likely intensify price pressure rather than alleviate it, while the yields on 10-year U.S. Treasury bonds stabilize around the psychologically significant 4% mark.

Federal Reserve Monetary Policy: How Significant is the Political Pressure?

Trump is pushing Congress for a swift confirmation of a new Fed chair and makes no secret of wanting a central bank that actively supports his growth and “affordability” agenda. Names like Kevin Warsh or Rick Rieder are circulating as potential successors to Jerome Powell. The core demand: a significantly looser Federal Reserve monetary policy with two to three additional rate cuts in 2026 – regardless of short-term economic data.

Fed officials have so far resisted. Several central bankers signal an extended pause until a sustainable return of inflation toward 2% is evident. Boston Fed President Susan Collins emphasizes that interest rates must remain “stable for some time.” This openly positions the Fed against Trump’s call for rapid rate cuts, reigniting the debate over its independence and creating structural stress for U.S. creditworthiness.

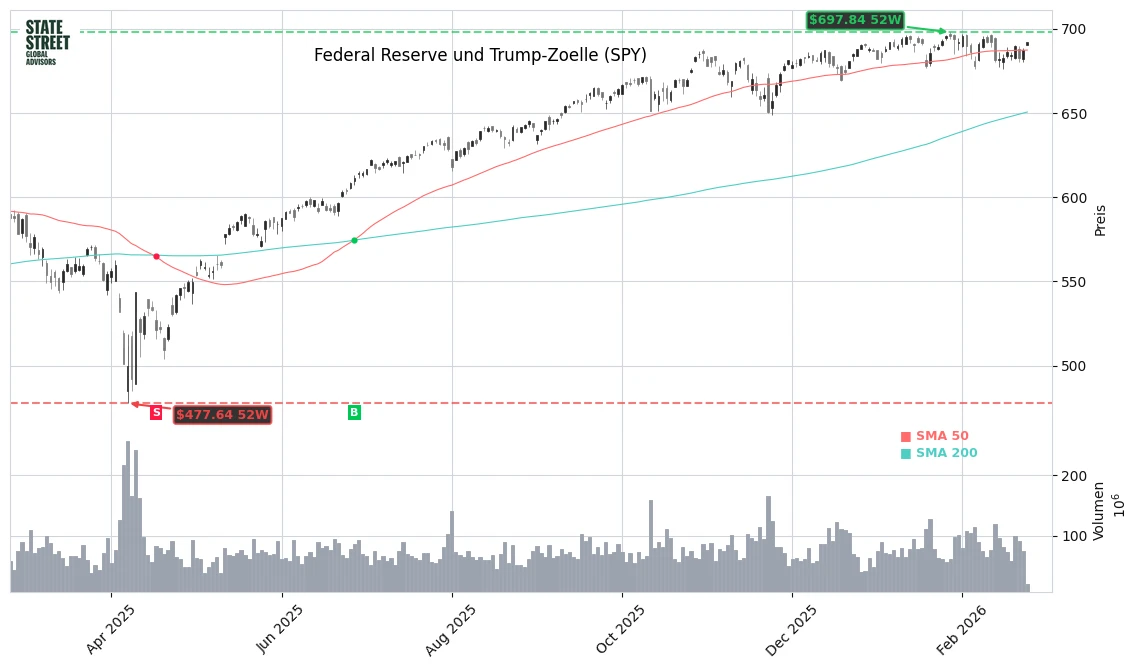

” alt=”Federal Reserve and Trump Tariffs Stock Chart – 252 Days Price Trend – February 2026″ loading=”lazy” style=”width:100%;height:auto;border-radius:8px;”>

What Do Tariffs and Interest Rates Mean for Stocks and the Housing Market?

Despite the political tensions, U.S. stock markets are showing resilience: the S&P 500 is at 6,940.54 points, having moved further away from last year’s lows. The Fear & Greed Index is at 43 points, near the neutral zone, while the VIX has fallen below 20 – a sign of decreasing short-term fear. Nevertheless, market strategists warn that the combination of high valuations, tariff uncertainty, and unclear Federal Reserve monetary policy increases vulnerability to pullbacks.

On the housing market, Trump’s policies and the Fed’s course collide particularly hard. The president aims to lower mortgage rates through further monetary easing and has simultaneously prohibited institutional investors from acquiring additional single-family homes to make room for private buyers. However, experts point out that a real market revival is only expected when mortgage rates fall below about 5.5%, while the central bank has not yet been willing to aggressively use the interest rate lever due to tariff dynamics and robust employment.

How Are Analysts Positioning Themselves on the Fed and Tariffs?

Research houses see the markets in a fragile equilibrium. At Goldman Sachs, the interest rate strategy department continues to expect a total of 50 to 75 basis points of easing by the end of the year, clearly data-dependent and only if the labor market noticeably weakens. Morgan Stanley, led by Chief Economist Seth Carpenter, remains positive about U.S. growth in 2026 at over 2.5%, but warns that tariffs could make inflation more persistent, thereby constraining the Federal Reserve’s monetary policy.

Citigroup highlights in its Fixed-Income and FX reports that a mix of fiscal expansion, higher tariffs, and only moderate rate cuts is likely to put pressure on the U.S. dollar in the medium term. RBC Capital Markets points to the high sensitivity of tech and AI stocks to real yields: should tariff escalation and a less accommodative Fed drive yields higher, particularly highly valued growth stocks could come under pressure, while value and small-cap stocks may benefit from tax cuts.

Tariffs drive inflation up while simultaneously expecting the Federal Reserve to save affordability through rate cuts – this balancing act will be a stress test for the independence of the central bank in 2026.

— Editor in Chief

Bottom Line

The Federal Reserve’s monetary policy stands at a turning point where political demands for cheaper money collide with the real constraints of inflation and tariff pressure. For investors, this means that robust indices like the S&P 500 are built on a foundation of fiscal stimulus but also increasing monetary policy risks. Those invested should closely monitor upcoming labor market and inflation data – they will determine whether the Fed can maintain its course or if political pressure ultimately dictates the direction.

Related Sources

- U.S. Inflation and Tariffs: How Politics Challenge the Fed (Bloomberg)

- Goldman Sachs Outlook 2026: Rates, Stocks and Tariffs (Goldman Sachs)

- Citigroup Global Markets – U.S. Rates & FX Strategy (Citigroup)