Is a divided Fed and rising geopolitical risk about to redraw the Federal Reserve Rate Path for stocks, real estate and crypto?

How fragile is the Federal Reserve Rate Path now?

The March 17-18 FOMC meeting ended with an 11-1 vote to hold rates at 3.50% to 3.75%, underscoring a fragile consensus. The minutes show that “the vast majority” of participants see both upside risks to inflation and downside risks to employment as elevated, a classic illustration of the Fed’s dual mandate dilemma. Several members argued that, if inflation continues to decline in line with forecasts, it would “likely become appropriate” to lower the target range later this year or in 2026, keeping at least one cut on the table.

Yet a growing faction now believes additional hikes may be required if inflation proves sticky, particularly in response to higher energy prices tied to the Iran conflict. Some participants explicitly called for a more two-sided description of policy risks, reflecting the possibility that upward adjustments in the federal funds rate could be necessary should inflation remain above target. That tension is exactly what makes the current Federal Reserve Rate Path highly data-dependent and difficult for markets to price.

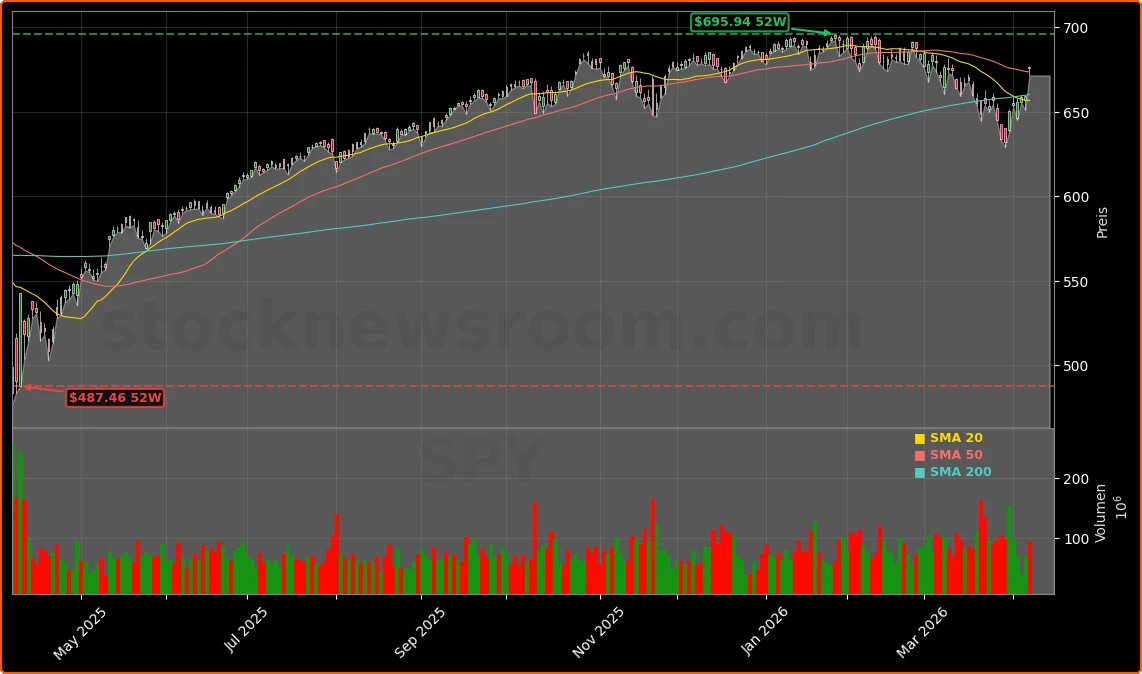

Derivatives markets remain cautious. FedWatch-style probabilities suggest a dominant chance that rates stay unchanged through the December meeting, with only a modest likelihood assigned to a cut and almost no conviction behind a hike in the near term. For portfolio managers, that implies ongoing yield competition for equities and a premium on companies with solid balance sheets.

What do geopolitics and oil mean for Tesla and energy?

The Iran war has become a central macro variable in the Fed’s discussion. Policymakers warned that an extended conflict could delay the disinflation process toward the 2% target by keeping oil and refined products like diesel elevated. Persistent energy strength tends to filter into transportation, food and core services, threatening to unanchor inflation expectations. Several officials indicated they would be open to another rate hike if these pressures fail to subside.

At the same time, a long war could weaken global demand and the U.S. labor market, increasing the case for cuts to avoid a hard landing. This two-sided risk is especially relevant for high-beta growth names and EV manufacturers such as Tesla, where valuations are sensitive both to discount rates and to consumer demand. Falling oil prices following tentative cease-fire headlines briefly eased inflation fears and pushed bond prices higher, bringing back expectations for one or two cuts in the second half of the year, with some economists shifting their base case from June to September.

For traditional energy companies on the S&P 500 and integrated majors on the NYSE, the combination of higher spot prices and a slower but still restrictive Federal Reserve Rate Path creates a mixed backdrop: better near-term cash flows but a higher hurdle rate for new long-cycle projects.

How does the Fed stance hit real estate and Apple?

The current rate environment continues to weigh heavily on the U.S. housing and commercial real estate markets. With the fed funds rate anchored near 3.5%-3.75% and term premia elevated, long-dated Treasury yields keep mortgage rates high. That makes it mathematically difficult to justify new development, as required returns for investors fail to clear financing costs. Developers report a significant decline in new construction starts and persistent delays in multifamily and office projects.

For large-cap growth and mega-cap tech such as Apple and NVIDIA, the implications are more nuanced. On one hand, persistently high real yields compress valuation multiples, particularly for cash flows far in the future. On the other, a cautious but non-aggressive Fed supports risk sentiment as long as corporate earnings remain robust and the labor market does not deteriorate sharply. History from 2022, when the S&P 500 dropped more than 16% amid rapid hikes, still looms large in investor memory.

The minutes also highlighted concerns that new technologies, including AI, are already eliminating some jobs and making labor conditions vulnerable to shocks. If job creation slows further, pressure could mount on the FOMC to tilt the Federal Reserve Rate Path toward easing, which would be supportive for duration-sensitive names on the NASDAQ.

What does the Federal Reserve Rate Path mean for gold and crypto?

The battle over inflation and rates is directly fueling the current gold rally. When the Fed embarked on aggressive tightening in 2022, spot gold briefly fell toward $1,656 per ounce as higher yields increased the opportunity cost of holding non-yielding assets. Today, markets expect eventual cuts by 2026, which would weaken the dollar and reduce those opportunity costs, supporting fresh inflows into bullion and gold ETFs on Wall Street.

Digital assets are also in focus. Strategists note that higher policy rates tend to channel capital toward safer income-generating instruments, limiting flows into Bitcoin (BTC) and other speculative tokens. Crypto bulls argue that a pivot to easing or renewed balance sheet expansion — sometimes loosely described as “money printing” — could act as a catalyst for a new leg higher in BTC, with some projecting a path toward $80,000 before a corrective phase and potential recovery toward $100,000 if liquidity conditions loosen.

Meanwhile, the Fed’s April note on stablecoins flagged the more than 50% jump in market capitalization to about $317 billion as of early April 2026, pointing to risks from complex intermediation chains and run dynamics. That assessment suggests the central bank will treat digital-dollar ecosystems as another factor when calibrating future steps along the Federal Reserve Rate Path.

The Fed is trying to walk a fine line between not choking off a cooling labor market and not letting war-driven energy shocks reignite inflation.— Kit Jukes, macro strategist at Sakjan

For diversified U.S. investors, the key takeaway is that the Fed is in no rush to cut, but also not firmly committed to further hikes. The split within the FOMC, the unresolved situation in Iran, and sticky core PCE near 3% keep policy in a narrow corridor where incoming inflation and labor data will drive every move. The next FOMC meeting at the end of April could recalibrate expectations again, making rate-sensitive sectors, from housing REITs to high-growth tech, especially reactive to each new data point.