Will the latest oil shock and fragile Middle East truce finally push Federal Reserve Rate Policy toward long-awaited cuts?

How is Federal Reserve Rate Policy shifting after the truce?

The fed left its benchmark rate unchanged in the wake of the Iran conflict, even as the oil shock pushed energy and transportation costs higher. Officials argued that responding aggressively to what might prove a temporary surge in fuel prices could damage growth without durably cooling inflation. With news of a cease-fire and a pullback in crude, markets are now rapidly repricing the outlook for Federal Reserve Rate Policy toward gradual easing rather than further tightening.

New York Fed President John Williams has been pivotal in that shift. He reiterated that the outlook for underlying price pressures is “largely unchanged,” despite the earlier spike in energy costs. Williams expects core inflation to rise only one or two tenths of a percentage point from the oil shock, while projecting headline inflation around 2.75% for the full year, heavily dependent on where crude prices settle. That relatively benign core view has helped push the implied probability of a 25-basis-point hike at the late‑April FOMC meeting down to roughly 3% in swaps markets.

At the same time, fed officials including Chair Jerome Powell and several regional presidents continue to stress caution. Inflation has run above the 2% target for roughly five years, and policymakers warn against declaring victory prematurely. Still, with geopolitical tensions easing and growth indicators softening at the margin, investors increasingly see the next move in Federal Reserve Rate Policy as downward, not upward.

What does the oil shock mean for inflation and growth?

The earlier oil spike raised the specter of stagflation: higher prices combined with slower growth. Chicago Fed President Austan Goolsbee voiced concern that an oil shock could push prices higher in a stagflationary way, squeezing consumers and complicating the policy trade-off. Transportation firms have already begun to add fuel surcharges, which tend to feed into broader logistics and, ultimately, food prices with a lag.

For now, Williams argues that monetary policy is well positioned to “wait and see,” with his growth forecast trimmed to around 2–2.5% this year and unemployment near 4.3%. Economists like Jason Schenker expect that softer economic data in coming quarters, including the possibility of the jobless rate rising toward 4.5%, could strengthen the case for two rate cuts this year, even if headline CPI hovers near 3.3% and core around 2.7%. That scenario would imply that the fed accepts slightly above‑target inflation in order to prevent a more pronounced slowdown in hiring.

The cease-fire has removed some of the immediate upside pressure on crude, easing fears of a sustained energy price spiral. If oil stabilizes or drifts lower, much of its direct contribution to inflation will fade, giving the central bank more room to shift Federal Reserve Rate Policy toward accommodation later in the year. Conversely, any renewed disruption that reignites fuel and fertilizer prices could lift grocery bills and force the fed back into a more hawkish stance.

How are Wall Street and tech leaders like NVIDIA reacting?

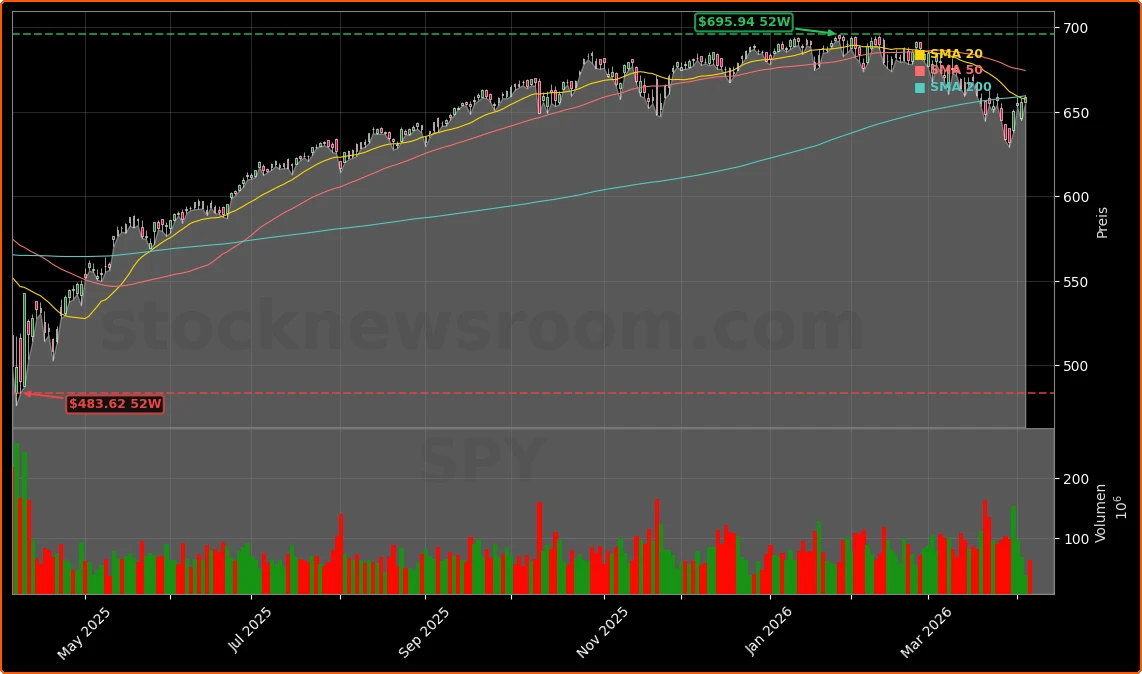

On Wall Street, the easing of rate-hike fears has been modestly supportive for risk assets. The S&P 500 was recently up about 0.08%, underscoring that investors are treading carefully rather than chasing a full‑blown relief rally. Higher long-term yields, with the 10‑year Treasury around 4.33%, still present a valuation headwind for growth stocks and high‑duration sectors such as mega‑cap technology.

Rate-sensitive names, from big tech like NVIDIA, Apple and Tesla to unprofitable software and speculative growth plays, stand to benefit the most if Federal Reserve Rate Policy shifts decisively toward cuts. Lower real yields reduce discount rates applied to long-dated cash flows and can re‑ignite the growth premium on the NASDAQ. Conversely, if oil or food prices flare back up and the fed is forced to keep rates elevated or even hint at further hikes, richly valued tech and long-duration equities would be among the first to reprice lower.

Commodity markets tell a similar story. The last major hiking cycle contributed to a drawdown in gold toward $1,656 in 2020 as higher real yields lifted the dollar and increased the opportunity cost of holding non‑yielding assets. Today, with investors once again expecting rate cuts later this year, the dollar has come under pressure, and bullion has found support as traders position for a more dovish Federal Reserve Rate Policy over the medium term.

Could regulation and global central banks change the picture?

Beyond the immediate oil shock, structural shifts in the financial system may also shape the path of rates. The Federal Deposit Insurance Corporation has proposed rules for banks involved in issuing and handling dollar stablecoins under the new GENIUS Act, setting standards for reserves, redemption and risk management. While these rules will not make stablecoin holders insured depositors, they are designed to bolster confidence in tokenized cash and could, over time, affect demand for money‑market funds and other short‑term dollar instruments that are closely tied to Federal Reserve Rate Policy benchmarks like SOFR.

The outlook for underlying price pressures is largely unchanged, even with higher energy costs, which argues for patience rather than a knee-jerk policy reaction.— John Williams, President of the New York Fed

On the global stage, interest‑rate differentials remain a key driver for currency markets. With the FOMC widely expected to cut at least 25 basis points in 2026 while the Bank of Japan and European Central Bank are projected to nudge rates higher, the dollar’s yield advantage is narrowing. That shift has already weighed on the greenback, reinforcing flows into U.S. risk assets but potentially loosening overall financial conditions more than the fed might like.