Can Intel Advanced Packaging turn hyperscaler AI deals into the profit engine that finally fixes the company’s struggling foundry business?

Is Intel’s packaging bet the new AI profit engine?

The quiet bottleneck in the AI hardware race has shifted from pure chip fabrication to how efficiently chiplets, high‑bandwidth memory and interconnects are combined into a single module. That is exactly where Intel Corporation is pushing Intel Advanced Packaging, built around technologies like EMIB and Foveros, which can deliver dense connections and improved power efficiency at attractive economics. Management has flagged potential gross margins around 40% on these services, roughly in line with Intel’s traditional product business, but with far lower capital intensity than building new leading‑edge fabs.

In recent investor comments, CFO David Zinsner described packaging as “the more interesting part of the Foundry business today”, signaling that meaningful revenue from Intel Advanced Packaging could arrive before wafer volumes ramp on the 18A process. That is a crucial distinction for U.S. investors looking for nearer‑term AI monetization rather than waiting years for full node transitions to pay off.

How big could deals with Google and Amazon be?

Reports indicate Intel is in advanced negotiations with Alphabet’s Google and Amazon Web Services to provide advanced packaging on their in‑house AI accelerators, including Google’s TPUs and Amazon’s Trainium and Inferentia chips. Zinsner has said Intel is “close to closing some deals that are in the billions of dollars per year in terms of revenue” from packaging alone, a scale that would dwarf the $222 million in external foundry revenue the company reported in the most recent quarter.

For hyperscalers, the attraction is twofold: cutting‑edge packaging capacity and a U.S.‑aligned alternative to Taiwan Semiconductor Manufacturing’s CoWoS technology. TSMC remains the volume leader, but intense allocation pressure means cloud giants are increasingly open to a second source. That gives Intel Advanced Packaging a strategic opening it has not enjoyed in traditional leading‑edge logic, where NVIDIA still relies heavily on TSMC for its flagship GPUs.

Where does this leave Intel versus rival chipmakers?

On Wall Street, the key question is whether Intel’s foundry pivot can close the performance and profitability gap to AI winners like NVIDIA and diversify exposure beyond PC and legacy server CPUs. KeyBanc Capital Markets recently highlighted that both Intel and AMD could benefit from improving server CPU demand, and Intel is reportedly preparing price increases across server and client products as the market tightens. At the same time, packaging‑driven AI revenue could provide a distinct profit stream that is less sensitive to cyclical PC demand.

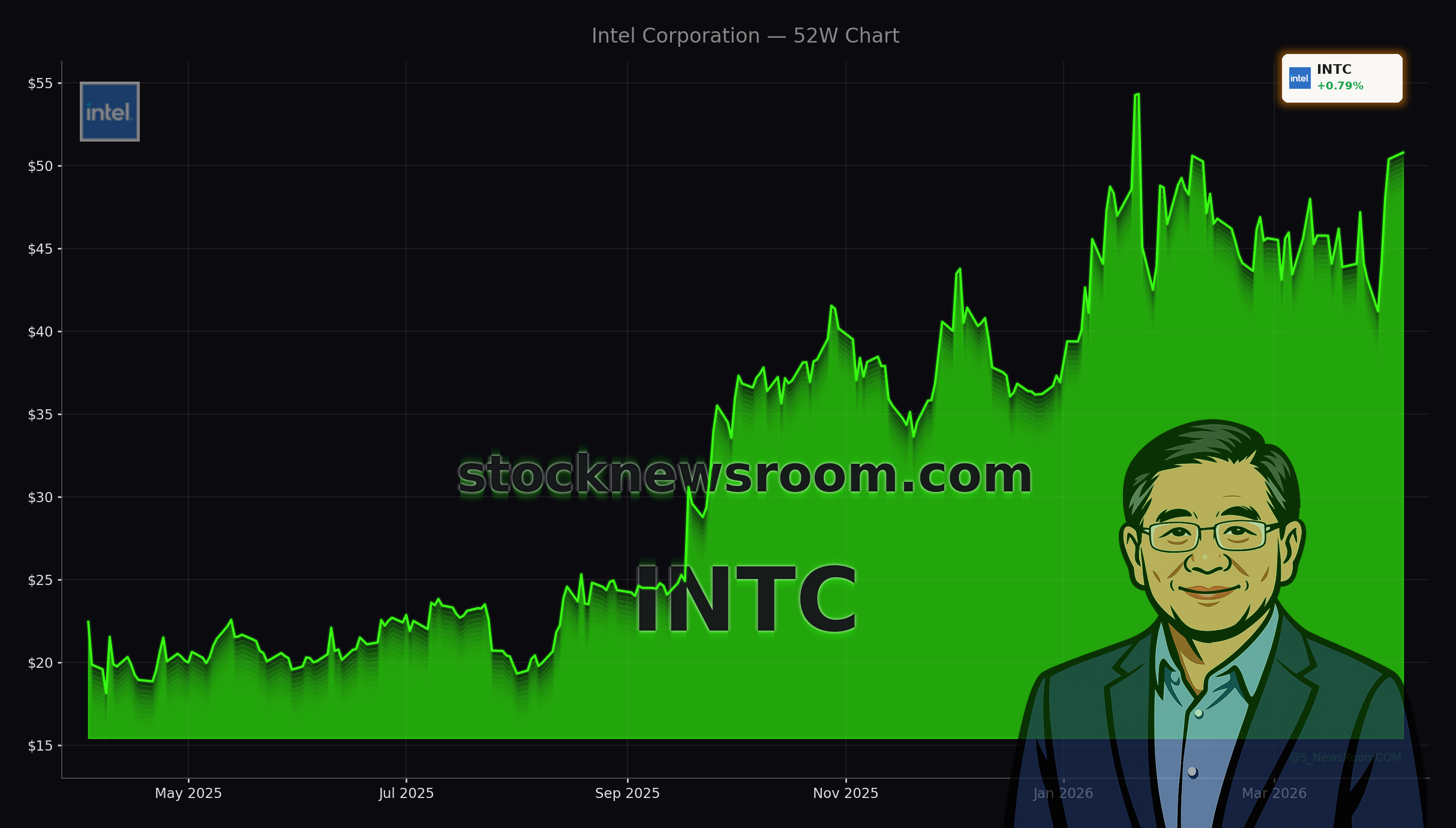

Investors should note the mixed sentiment embedded in current analyst targets. Zacks Investment Research points out that consensus on Intel screens cautious, with many on Wall Street still rating the stock a “Reduce” despite AI enthusiasm. MarketBeat data shows an average target price in the mid‑$40s, below Monday’s close, even as some houses nudge their estimates higher. In contrast, KeyBanc recently raised its price target from $65 to $70 with an “Overweight” rating, arguing that Intel’s AI and foundry initiatives are still underappreciated by the broader market.

Can Intel Advanced Packaging fix the foundry P&L?

Intel Foundry remains deep in the red: the unit generated $4.5 billion in quarterly revenue but posted a $2.5 billion operating loss due largely to heavy 18A ramp costs. Yet management continues to guide to breakeven operating margins by the end of 2027. The math hinges on scaling Intel Advanced Packaging faster than full‑blown wafer volumes. Packaging expansions in New Mexico and Malaysia, backed in part by CHIPS Act funding, are designed to add capacity without the multibillion‑dollar price tag of a new leading‑edge fab.

If Intel can secure even one hyperscaler on a long‑term, multi‑billion‑dollar packaging agreement, external foundry revenue could jump from a trickle to a meaningful line item within the next couple of years. That would not only validate Intel Advanced Packaging as a differentiated technology offering, it would also strengthen the strategic case for U.S.‑based AI manufacturing at a time when Washington is keen to reduce dependence on Asia for critical semiconductor supply.

How are institutions and Wall Street reacting?

Institutional flows remain mixed. Several asset managers, including Y.D. More Investments and Perpetual Ltd, trimmed positions in Intel during the fourth quarter, locking in gains after the stock’s strong run and reflecting lingering skepticism about execution risk. Others added exposure, and insiders have been active as well, with one senior executive selling shares while Zinsner himself bought, signaling internal confidence in the long‑term plan.

For U.S. portfolio managers, Intel now sits at the intersection of multiple themes: the AI arms race, domestic manufacturing policy and the rebirth of a legacy S&P 500 technology giant. Intel Advanced Packaging is no longer a technical footnote; it is emerging as a potential swing factor for margins, cash flow and ultimately where the stock settles within the NASDAQ’s crowded AI trade, alongside names like Apple and Tesla which offer different, more consumer‑oriented exposure.

Related Coverage

Investors who want a deeper look at Intel’s manufacturing bets can read how the company is spending $14.2 billion to fully reacquire its Fab 34 facility in Ireland in “Intel Fab 34 buyback $14.2B Surge in AI Ambition”, which examines whether that deal can close the gap with top AI chip rivals. For a broader PC and device ecosystem angle, “Apple MacBook Neo Strategy Boom in Budget Laptops” explores how Apple is repositioning in the low‑end laptop segment, a move that could indirectly shape demand for x86‑based systems where Intel still holds substantial share.

In the end, Intel Advanced Packaging is positioning Intel Corporation as a critical supplier in the AI build‑out, potentially unlocking high‑margin, multi‑billion‑dollar revenue streams from cloud giants while its wafer roadmap catches up. For Wall Street, the next major catalysts will be the formal announcement of any Google or Amazon packaging wins and updated guidance on foundry profitability targets. If execution matches the ambition, Intel’s packaging bet could turn today’s cautious sentiment into a more durable AI‑driven re‑rating over the coming years.