Is the Intel AI Strategy finally delivering a lasting turnaround, or just fueling another short-lived hype rally in the stock?

Is Intel’s AI pivot really driving the stock?

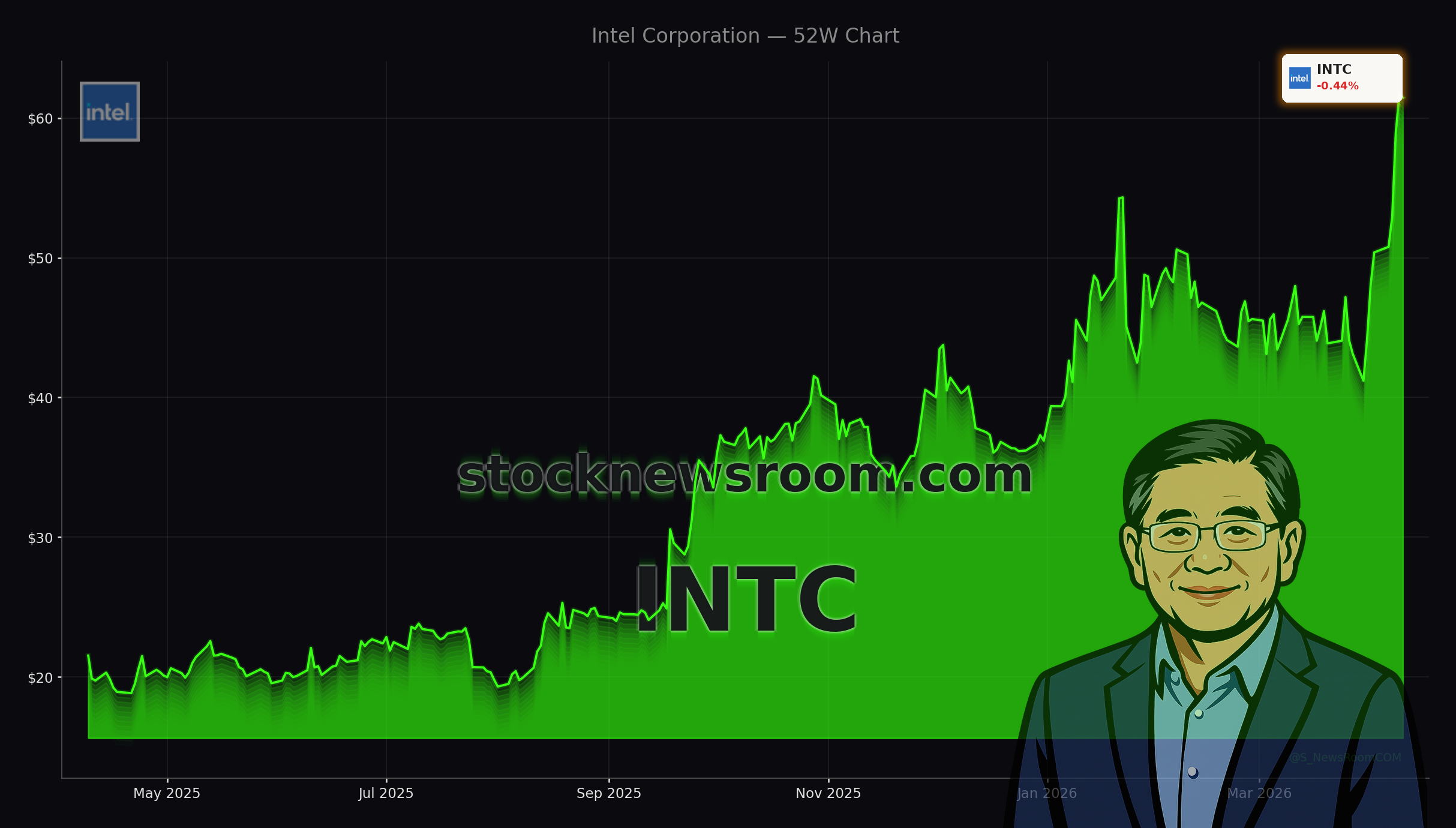

At roughly $62, Intel remains about 20% below its 2000 dot‑com peak but is now at its highest level since April 2021, making it one of the standout gainers in the S&P 500’s recent seven‑day winning streak. The Intel AI Strategy has become the core narrative behind that move: investors are betting that a renewed focus on AI data‑center CPUs, AI‑ready PCs and custom infrastructure chips can pull the company out of years of underperformance versus rivals like NVIDIA and AMD.

Momentum is extreme. Intel is up about 57% year‑to‑date and roughly 187% over the past 12 months, making it one of the top semiconductor performers on the NASDAQ. The stock’s advance has been powered by a cluster of catalysts, including expanded AI partnerships with Google, participation in Elon Musk’s Terafab chip‑building initiative alongside Tesla and SpaceX, and a move to buy back full control of its Irish fab. For now, buyers clearly believe this time Intel’s turnaround story is different.

What does the Google partnership change?

The latest leg of the rally was sparked by news that Intel and Google are deepening their collaboration to build next‑generation AI and cloud infrastructure. Google Cloud plans to continue deploying Intel’s Xeon processors for general‑purpose workloads while broadening co‑development of custom infrastructure processing units (IPUs) and ASIC‑based chips tailored for AI‑heavy data centers. This ties directly into the Intel AI Strategy: the company wants to supply both the CPU backbone and specialized accelerators that sit alongside GPUs in modern AI clusters.

The deal comes as demand for AI inference and agentic AI systems shifts some attention back to CPUs, which handle a significant share of orchestration and non‑GPU processing. For Intel, being embedded in Google’s long‑term roadmap could stabilize data‑center revenue and, critically, showcase its ability to deliver custom silicon at scale — a prerequisite if it is to compete for broader cloud and hyperscaler business against Advanced Micro Devices and NVIDIA.

How does the Intel AI Strategy fit the foundry reboot?

Under CEO Lip‑Bu Tan, Intel is pushing an ambitious “five nodes in four years” manufacturing roadmap aimed at regaining process leadership with Intel 18A by 2025. The Intel AI Strategy is tightly coupled with this foundry reboot: leading‑edge AI chips require cutting‑edge process nodes, and Intel wants not only to build its own products but also become the world’s second‑largest contract foundry by 2030, behind TSMC.

Washington is helping. Intel has secured about $8.5 billion in CHIPS Act funding to support advanced manufacturing and capacity expansion in the U.S. and Europe. A marquee design win from Microsoft for Intel 18A manufacturing — with a reported lifetime value near $15 billion — suggests at least some major customers believe Intel can deliver. If the company proves it can manufacture bleeding‑edge AI and data‑center silicon for external clients, it could unlock a new, capital‑intensive but potentially high‑margin revenue stream that differentiates it from fabless rivals like Apple or AMD.

Are valuations and analyst views getting stretched?

Despite the excitement, Intel’s valuation has gotten demanding. Recent data show a trailing price‑to‑earnings ratio north of 900 and a forward P/E above 100, reflecting depressed current profits and heavy expectations for a multi‑year earnings ramp. Free cash flow remains negative — around minus $5 billion — while gross margin at roughly 35% trails sector leaders. The company is also carrying higher debt after years of elevated capex.

Wall Street analysts are split. Across dozens of firms, the consensus target price sits in the low‑$40s, implying downside from current levels, even though more recent updates cluster closer to today’s price. KeyBanc, for example, has one of the more optimistic views, lifting its target to $70 on April 6, 2026, while Baird has been more cautious with a $20 target. Overall, only a small single‑digit percentage of analysts rate the stock a clear “Buy,” with more rating it “Hold” or even “Sell.” Major U.S. houses such as Morgan Stanley, Goldman Sachs or Citigroup have emphasized execution risk around the foundry pivot, competitive pressure from NVIDIA in AI accelerators and ongoing market‑share losses to AMD in both client and server CPUs.

What are the main risks versus competitors?

The bull case argues that if Intel hits its process roadmap, scales Intel 18A and wins more cloud and AI customers, the Intel AI Strategy could justify the current premium and possibly more. Rising AI‑PC penetration — projected to move from under 20% in 2024 to more than half of the PC market by 2026 — could also play into Intel’s strength in laptop and desktop CPUs, especially if its AI‑optimized chips become the default for large OEMs.

The bear case is straightforward: rivals may simply move faster. AMD continues to chip away at x86 server and consumer share, while NVIDIA dominates AI accelerators and software ecosystems. Arm‑based server chips from hyperscalers like AWS and Google are gaining traction, eroding what used to be an Intel‑only domain. Any further delays in fabs in Germany or Poland, or failure to secure big‑ticket 14A and 18A foundry customers, could force Intel to scale back its most advanced manufacturing efforts, undermining the strategic reset.

Related Coverage

For a deeper dive into how the latest Google announcement specifically moved the stock, readers can explore detailed coverage of the Intel–Google AI partnership and the resulting 4.7% rally, which breaks down the deal’s structure and near‑term earnings implications. Investors tracking the broader AI trade beyond U.S. semiconductors may also want to read about Chinese tech, including how Alibaba’s surprise strength in AI video has fueled a fresh rally in BABA despite concerns about capex and margins, offering a useful contrast to Intel’s hardware‑driven AI story.

The market is finally starting to price in the possibility that Intel’s AI and foundry strategy actually works, but the burden of proof from here is all about execution.— Unnamed Wall Street semiconductor analyst

In sum, the Intel AI Strategy has transformed a former laggard into a high‑beta AI play approaching a five‑year high, powered by cloud partnerships, foundry ambitions and a resurgent PC roadmap. For U.S. investors, the stock now sits at the crossroads of AI infrastructure, onshoring policy and cyclical semiconductor dynamics. The next test will be whether upcoming quarters and new design wins can turn today’s narrative into sustained earnings growth, making Intel’s AI pivot a durable part of long‑term portfolios.