Is Intel’s $14.2 billion Fab 34 buyback the bold AI manufacturing gamble that finally closes the gap with its fiercest chip rivals?

Why did Intel stock jump on the Fab 34 deal?

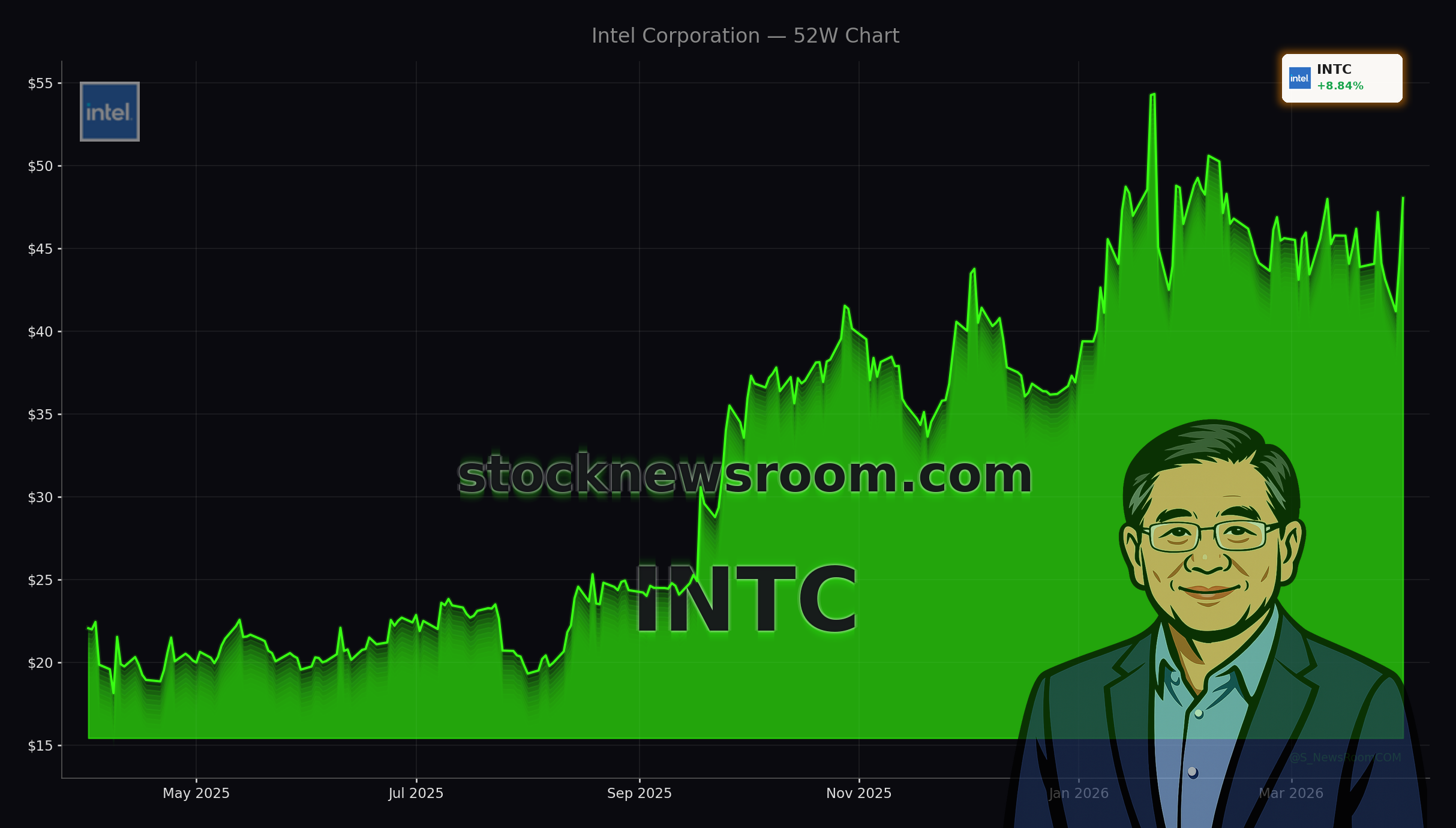

Intel (INTC) rallied 8.84% on Wednesday to close at $48.03, outperforming the broader semiconductor rally on the NASDAQ and S&P 500. The pop followed Intel’s announcement that it will buy back Apollo’s 49% stake in the Fab 34 joint venture in Ireland for $14.2 billion, funded with existing cash and roughly $6.5 billion in new debt. The Intel Fab 34 buyback restores full ownership of one of its most advanced manufacturing sites at a time when AI infrastructure demand is booming.

Fab 34 produces cutting-edge chips for AI-enabled PCs and high-performance data-center processors, including CPUs that will support AI inference workloads. Management said the transaction should be accretive to earnings per share by 2027, reinforcing the view that Intel is trading short-term leverage for long-term strategic control. With the stock still below its 52-week high of $54.60, some investors see the move as a turning point after the deep downturn of 2023–2024.

What does the Intel Fab 34 buyback mean for AI strategy?

The Intel Fab 34 buyback sits at the core of Intel’s attempt to reposition itself in the AI era after missing the first wave of GPU-driven training dominated by NVIDIA. As AI spending shifts from model training toward inference—running those models in the cloud and at the edge—demand for advanced CPUs and custom accelerators is expected to climb sharply. Fab 34 is set to be one of Intel’s main hubs for producing these inference-focused chips on leading-edge process nodes.

Intel is also building out its contract foundry business, aiming to manufacture chips for external customers that compete directly with Taiwan Semiconductor and, indirectly, with design-focused rivals like Apple and Tesla. Full control of Fab 34 gives Intel maximum flexibility to prioritize its own AI road map or allocate capacity to high-value foundry clients. Several analysts argue that as 3 nm and below capacity tightens globally, owning a modern fab outright could become a competitive advantage rather than a balance-sheet drag.

How does this reshape Intel’s financial profile?

On the surface, adding $6.5 billion in new debt for the Intel Fab 34 buyback raises leverage and short-term risk. But Intel’s management is clearly signaling that it sees more value in owning a cash-generating fab than in preserving a highly structured joint venture that siphons off 49% of the economics to Apollo. CFO David Zinsner emphasized that the original 2024 sale of the stake to Apollo for $11.2 billion provided important flexibility at a time when Intel needed capital to accelerate its turnaround.

Today, with government support in the U.S. and Europe, improving margins, and a firmer competitive footing, Intel appears more comfortable bringing Fab 34 fully back on balance sheet. Northland Capital Markets has highlighted the buyback as a bullish signal for Intel’s long-term earnings power, although the broader Wall Street consensus on the stock remains a Hold with average price targets still below the most optimistic bull cases. Investors will be watching upcoming quarters to see whether operating cash flow and foundry bookings keep pace with the higher capital intensity.

How does Intel stack up against AI chip rivals?

Even with the Intel Fab 34 buyback, the competitive landscape remains fierce. NVIDIA still dominates high-end AI training with its data-center GPUs, while Advanced Micro Devices is scaling both GPUs and AI-optimized CPUs. Arm-based designs are gaining traction in custom AI servers, and hyperscalers are pushing their own accelerators, raising the bar for Intel’s x86 roadmap.

Intel’s counter is a more diversified approach: x86 CPUs for inference, custom accelerators, and a foundry platform that could eventually manufacture chips designed by many of those same rivals. At the same time, Intel is deepening its exposure to AI startups. It plans to invest an additional $15 million into AI chip and software startup SambaNova Systems, bringing its stake to roughly 9%, though that move has drawn governance questions because Intel CEO Lip-Bu Tan also chairs SambaNova and has venture stakes in several related companies.

For U.S. investors comparing Intel to mega-cap AI leaders, the story is different: Intel’s multiple remains far below high-fliers like NVIDIA and other AI infrastructure plays, reflecting both execution risk and the capital-heavy nature of fabs. The payoff from the Intel Fab 34 buyback, therefore, hinges on Intel’s ability to translate new AI demand and foundry wins into sustainable margin expansion.

Related Coverage

For a deeper dive into how this transaction fits into Intel’s broader turnaround narrative, including technical chart levels and sentiment after the initial spike, see Intel Fab 34 Deal +8.9% Rally After $14.2B Buyback Shock. If you are tracking how other tech giants are making capital-intensive infrastructure bets, particularly in space and communications, it is also worth reading Apple Satellite Strategy Warning as $1.5B Globalstar Bet Faces Test for context on how strategic assets can reshape long-term competitive positions.

In the end, the Intel Fab 34 buyback underscores how central advanced manufacturing has become to the AI race. For investors, the deal confirms that Intel is willing to take on more risk now to secure capacity and control in a tightening chip market. The next few years of execution on AI inference, foundry services, and capital returns will determine whether this $14.2 billion wager turns into the sustained earnings growth Intel is promising.