Can Intel’s $14.2 billion Fab 34 Deal really turn a balance-sheet gamble into a long-term AI and foundry advantage?

Why does the Intel Fab 34 Deal matter for Wall Street?

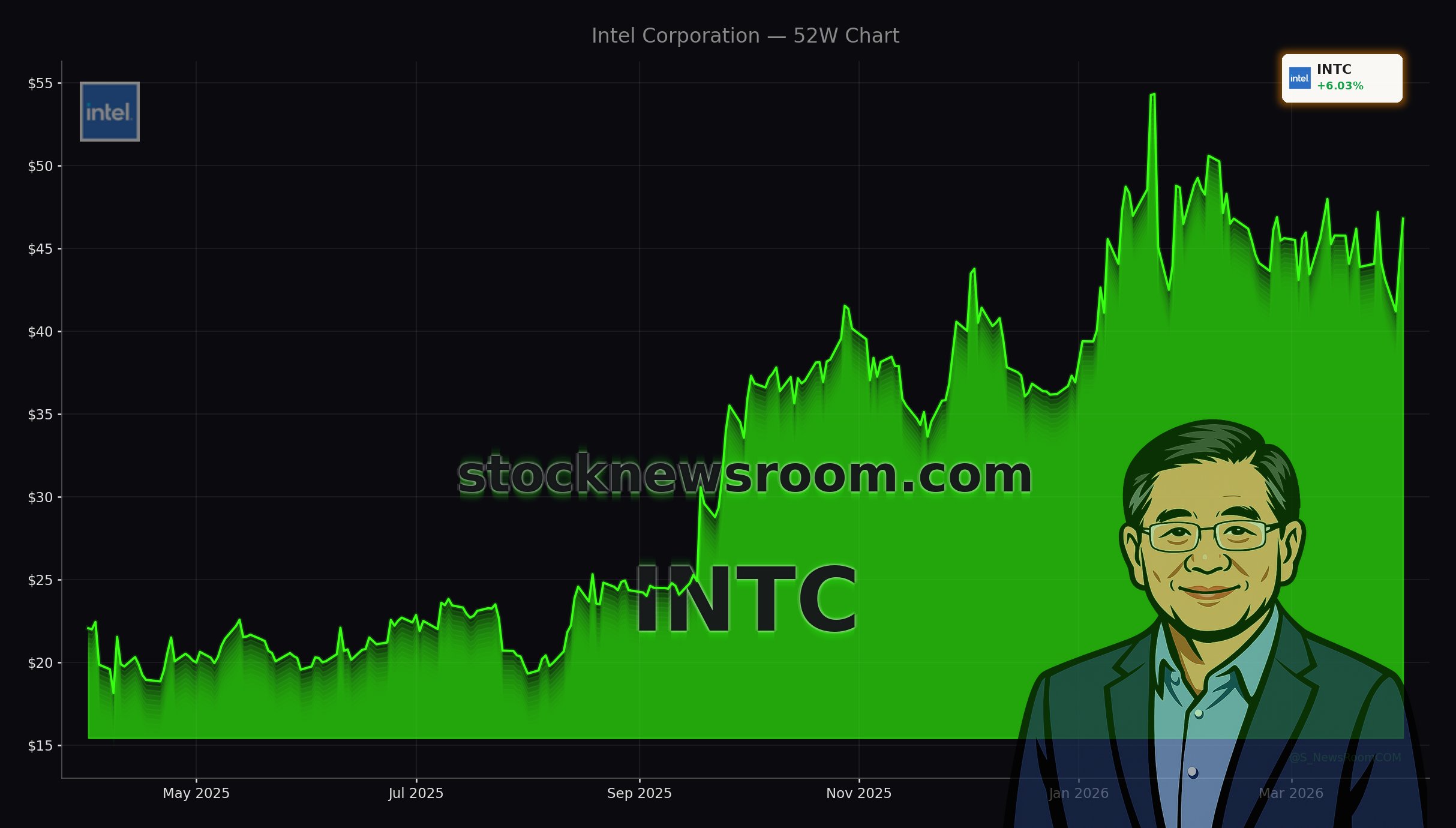

The Intel Fab 34 Deal immediately boosted market sentiment around Intel, with the stock rallying nearly 9% to $48.05, well above its prior close of $44.44. While still below recent 52‑week highs, the reaction highlights how investors view this $14.2 billion transaction as a vote of confidence in Intel’s balance sheet, AI demand tailwinds and long-term manufacturing roadmap. The company plans to fund the repurchase through a mix of cash on hand and roughly $6.5 billion in new debt, while still expecting to retire upcoming maturities in 2026 and 2027.

For U.S. portfolios heavily exposed to mega-cap AI beneficiaries such as NVIDIA and Apple, Intel’s move offers a different angle on the AI infrastructure trade: owning the fabrication capacity itself. Fab 34, based in Leixlip outside Dublin, is a high-volume plant for Intel 4 and Intel 3 process technologies, supporting Core Ultra PC chips and Xeon 6 data center processors that are increasingly used in AI inference workloads. Intel said the Intel Fab 34 Deal should be accretive to ongoing EPS and strengthen its credit profile from 2027 onward, a key point for income and quality-focused investors in the S&P 500 and NASDAQ.

How does Fab 34 fit into Intel’s AI and foundry strategy?

Fab 34 is central to Intel’s plan to build a competitive global foundry business and reclaim technology leadership from rivals. The facility was the company’s first high-volume site for Intel 4, using extreme ultraviolet (EUV) lithography, and is now being expanded for Intel 3. These nodes underpin chips that target AI-enabled PCs and data center platforms, areas where Intel is trying to close the gap with NVIDIA’s accelerators by leaning on CPUs for inference and complementary workloads.

The original 2024 joint venture with Apollo injected $11.2 billion of equity-like capital into Intel, allowing the company to accelerate critical projects such as Intel 4, Intel 3 in Europe and its next-generation Intel 18A process in the U.S. With the turnaround further along, CFO David Zinsner emphasized that Intel now has a stronger balance sheet, improved financial discipline and an evolved strategy, making it the right time to fold the JV back in. For investors tracking Intel’s AI CPU strategy and foundry roadmap, the Intel Fab 34 Deal is a signal that management wants tighter operational control over a key EU manufacturing asset just as AI data center build-outs are accelerating globally.

What are the financial and competitive implications for Intel?

Financially, the transaction is structured to balance growth investments with credit discipline. Intel expects the repurchase to add to EPS while ultimately improving its credit profile beyond 2027, even after issuing about $6.5 billion in new debt. This is happening alongside a broader restructuring under CEO Lip-Bu Tan, which has included job cuts, asset sales and a sharper focus on profitable manufacturing and foundry services. The company has also benefited from significant capital support, including U.S. government incentives and strategic investments from ecosystem partners, as it ramps capacity in both Europe and the United States.

Competitively, the Intel Fab 34 Deal positions Intel to better respond to surging AI infrastructure demand that has driven outsized gains for names like NVIDIA and pushed peers such as Broadcom and AMD into custom accelerators and advanced packaging. With customers diversifying supply chains and seeking more geographically distributed production, Intel’s control over Fab 34 strengthens its pitch as a Western manufacturing alternative for advanced nodes. For investors comparing AI exposure across the semiconductor stack, Fab 34’s output in Intel 4 and Intel 3, and its eventual linkage to Intel 18A products, is a key part of whether Intel can regain pricing power and margin stability.

How are institutional investors and analysts reacting?

The deal lands amid mixed but active institutional positioning in Intel. Recent filings show firms like Nisa Investment Advisors LLC modestly increasing holdings to more than 1 million shares, while others such as Meyer Handelman Co. and Silver Oak Securities have trimmed exposure, reflecting ongoing debate about execution risks and cyclical timing. Overall institutional ownership sits around the mid‑60% range, a solid base for a mega-cap chipmaker undergoing a multi-year reset.

On the Street, consensus remains cautious. MarketBeat data show an average analyst rating around “Reduce” with an aggregate price target near $45.74, below today’s $48.05 spot price after the news-driven spike. Some banks, including Citigroup and Goldman Sachs, have in recent months nudged price targets higher on AI and foundry optionality but still flag Intel’s negative net margins, heavy capex and the need to prove it can consistently deliver on its node roadmap. RBC Capital Markets has generally taken a “Sector Perform” stance, highlighting that while the Fab 34 transaction is strategically sound, investors will ultimately judge Intel on sustained earnings growth and foundry customer wins.

How does this compare with broader AI chip trends?

Across the sector, the Intel Fab 34 Deal lands in the middle of a broader AI build-out that is reshaping capital allocation. Tesla is designing its own AI silicon for autonomous driving and data centers, Broadcom is pursuing tens of billions in custom AI chips for hyperscalers, and cloud providers are deploying proprietary accelerators to reduce dependence on any single vendor. For Intel, owning Fab 34 outright supports not just internal CPU production but also its ambition to manufacture chips for external customers on advanced nodes, including Intel 18A, where early interest from major tech platforms has been reported.

Investors watching the NASDAQ and semiconductor ETFs now have another data point suggesting that Intel is willing to use its balance sheet aggressively to secure strategic assets, while still pledging to manage leverage and retire debt on schedule. Whether that bet pays off will depend on Intel’s ability to translate fabs like 34 into durable AI and foundry revenue, and to narrow the technology and profitability gap versus faster-growing peers.

Related Coverage

For a deeper dive into how Intel is trying to monetize AI CPUs, readers can review our analysis of pricing power and data center positioning in Intel AI CPU Strategy +6.8%: Can Pricing Power Last?. That piece examines whether recent price moves reflect a durable turnaround or a late-cycle squeeze.

Investors comparing Intel’s manufacturing-centric bet with other AI chip strategies should also read Broadcom AI Strategy Boom: Targeting $100B Custom Chips, which looks at how Broadcom aims to ride hyperscaler demand with custom accelerators rather than owning leading-edge fabs.

Today, we have a stronger balance sheet, improved financial discipline and an evolved business strategy.— David Zinsner, Intel CFO

The Intel Fab 34 Deal ultimately reinforces Intel’s decision to anchor its turnaround in advanced manufacturing, full control over strategic European capacity and tighter alignment between its balance sheet and long-term AI roadmap. For U.S. and global investors, the transaction makes Intel a more focused, higher-conviction play on Western chip fabrication, and the next few quarters will show whether improving AI demand and foundry traction can justify the renewed capital commitment.