Is the revamped Intel Strategy and Irish fab buyback the start of a genuine AI comeback or just another short-lived rally?

Is Intel buying back Ireland to go all-in on AI?

The decision by Intel Corporation to repurchase the remaining 49% stake in its Irish chipmaking facility from Apollo marks a sharp break from the austerity era under former CEO Pat Gelsinger. That stake sale in 2024 was a distress move to raise cash; taking the fab fully back on balance sheet now suggests management believes AI-driven demand will justify higher capacity and capital intensity. The plant is central to Intel’s push to ramp advanced process nodes and packaging for data center and cloud customers.

Under new CEO Lip-Bu Tan, long known in Silicon Valley from his leadership at Cadence Design Systems, Intel is leaning heavily into advanced semiconductor packaging, an increasingly lucrative part of the AI hardware stack. While GPUs from players like NVIDIA dominate headlines, large AI clusters also require huge numbers of CPUs to orchestrate workloads, run traditional services, and manage networking, storage, and security. That is where the revamped Intel Strategy sees a chance to defend and expand its historic CPU beachhead.

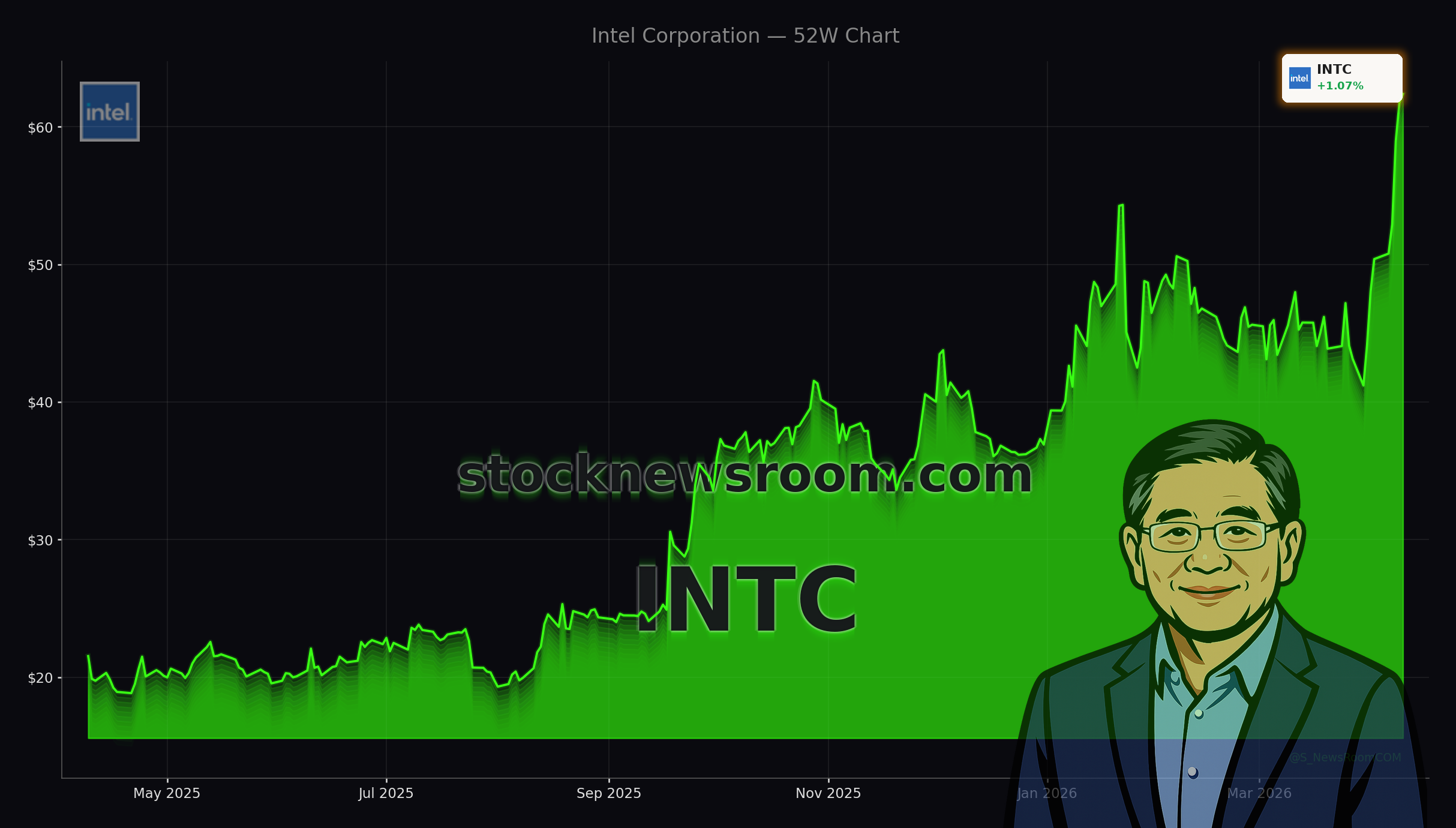

The stock has surged roughly 50% over the last eight trading days, giving the chipmaker what some on Wall Street are calling a “renewed lease on life.” At around $62, shares are well off pandemic-era lows near $20, though still below previous cycle peaks, leaving room for debate over whether the current AI enthusiasm is ahead of fundamentals.

How does Intel Strategy target the AI cloud buildout?

One anchor of the new Intel Strategy is a multiyear collaboration with Google Cloud to optimize AI and cloud infrastructure around Intel Xeon processors and custom infrastructure processing units (IPUs). The plan is to offload networking, storage, and security tasks from main CPUs onto IPUs, boosting system utilization and energy efficiency in hyperscale data centers. For U.S. investors, this is a signal that major cloud platforms still see Intel as a strategic partner, not just a legacy vendor.

Beyond Google, Intel’s positioning in general-purpose AI compute is designed to complement, rather than directly replace, the GPU-centric approach that powers large language models. As AI applications move from training to massive deployment, enterprises need flexible CPU capacity for inference routing, pre- and post-processing, and integrating AI into existing software stacks. Intel is betting its latest Xeon 6 family can become the default CPU backbone for that transition, even as GPUs from NVIDIA or custom ASICs handle the heaviest math.

Macro tailwinds are also helping. Semiconductor equipment leaders like Applied Materials are highlighting strong demand from U.S. chipmakers expanding domestic production under the CHIPS Act, while test players such as Teradyne see rising orders tied to AI and automotive chips. Intel sits in the middle of this ecosystem, benefiting from both the AI cycle and Washington’s push to reshore advanced manufacturing.

Can Intel compete with NVIDIA, AMD and the hyperscalers?

Even with the Ireland fab buyback and fresh cloud deals, the competitive bar remains high. NVIDIA still dominates the AI accelerator market, while AMD has gained ground in both CPUs and GPUs for servers. At the same time, hyperscale cloud providers like Google, Amazon and Microsoft are rolling out more in-house silicon for AI and networking. Any long-term investment case must assume Intel can carve out differentiated roles in CPUs, packaging, and foundry services rather than winning every chip category outright.

The advanced packaging expertise that CEO Tan brings is crucial here. As AI models scale, fitting more compute, memory, and interconnects into dense, power-efficient packages becomes a core constraint. Intel is pushing technologies like 3D stacking and high-bandwidth interconnects to keep up. If successful, the company could become the go-to integrator for heterogeneous systems that mix CPUs, GPUs, and custom accelerators – even those it does not design itself.

Recent performance in the broader semiconductor space shows investors are willing to pay up for credible AI infrastructure stories. The iShares Semiconductor ETF has rallied on easing geopolitical risks and strong results from industry leaders, with Intel cited among names expanding capacity and technology footprints. Weekly market data also show Intel among the top gainers across U.S. stocks, underscoring the momentum behind the narrative shift.

What are analysts and institutions watching next?

Institutional investors are looking closely at whether Intel can translate stock momentum into sustained earnings growth. Large asset managers have been rotating exposure within the semiconductor supply chain, and several firms now highlight Intel-related AI demand as a driver for suppliers like Teradyne. Research houses including Zacks have moved Intel into “strong buy” territory on the back of partnerships like Google’s Terafab project, which leans on Intel hardware for AI-focused buildouts.

On the sell-side, major banks such as Goldman Sachs, Citigroup, and Morgan Stanley are updating models to reflect higher utilization at Intel’s fabs and better pricing power in data center CPUs and packaging. Some commentators argue the stock “should be at $70” if the new strategy plays out, implying further upside from current levels. Others caution that execution risk remains high, especially as Intel ramps costly new nodes and competes with deeply entrenched rivals.

For now, the combination of the Irish fab buyback, deepened Google collaboration, and sector-wide AI strength has shifted sentiment decisively. The crucial question is whether this phase of the Intel Strategy can sustain higher margins and market share without overextending the balance sheet again.

Related Coverage

Investors who want a deeper dive into the AI narrative can look at how Intel’s recent surge fits into its broader repositioning. The article “Intel AI Strategy Rally: Can This Boom Really Last?” examines whether the current run-up is backed by durable fundamentals or just another short-lived hype cycle around AI hardware demand. For a wider industry angle, “Microsoft AI Strategy Boom: Can a $625B Cloud Bet Pay Off?” analyzes how Microsoft’s massive Azure and Copilot commitments could influence spending patterns across the entire data center and chip ecosystem, including Intel and its competitors.

There’s effectively no AI without a lot of CPU horsepower, and Intel is betting that its combination of Xeon and advanced packaging can turn that reality into durable cash flow.— Lip-Bu Tan, Intel CEO (paraphrased industry view)

In sum, the latest phase of the Intel Strategy centers on regaining full control of critical manufacturing in Ireland, doubling down on AI cloud alliances, and monetizing packaging know-how in the data center stack. For U.S. investors, Intel remains a high-beta way to play the infrastructure side of AI rather than the headline-grabbing model providers. The next several quarters of execution on capacity, partnerships, and margins will determine whether this strategy cements Intel as a long-term winner in AI compute or simply marks another cyclical upswing in a notoriously volatile sector.