Is Intuit’s sharp rebound a real vote of confidence in its tax and AI strategy, or just another bear-market head fake?

Intuit in the Market Crossfire: What the Rebound Really Means

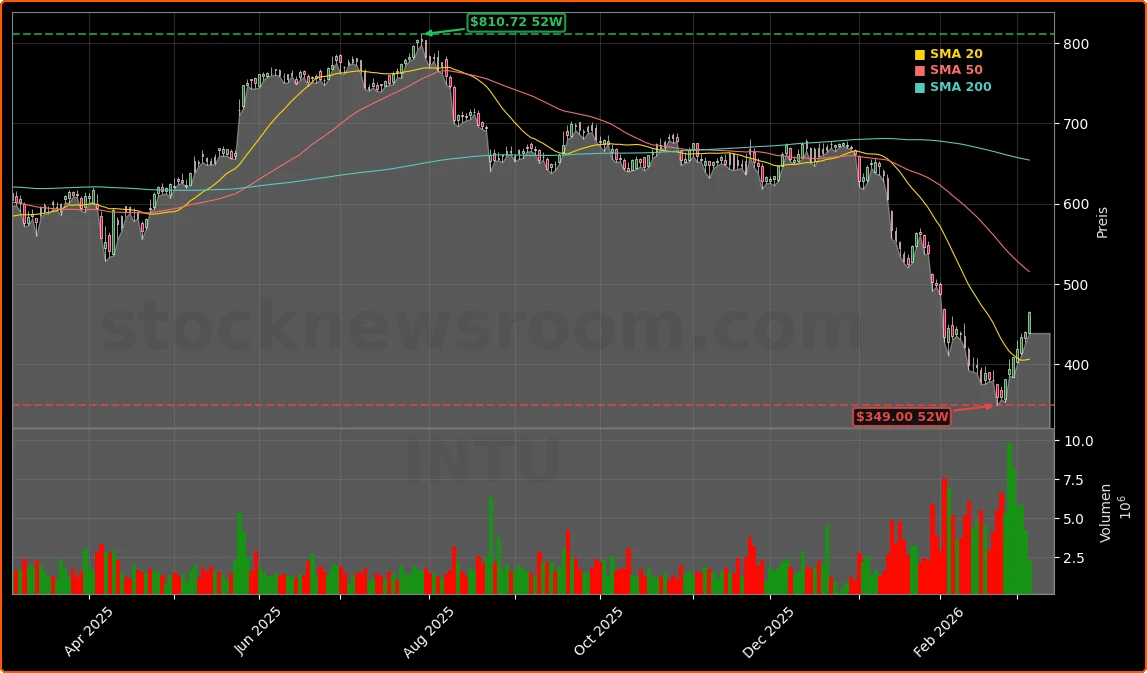

Intuit’s share price at roughly $465.45, up about 5.8% on the day, stands in stark contrast to the stock’s bruising performance earlier in the year, when software names broadly sold off on fears that generative AI would erode incumbents’ pricing power. While the stock has bounced from its lows, it is still well below prior peaks and remains in repair mode rather than exuberant territory. For growth investors benchmarking to the NASDAQ and S&P 500, the key question is whether the recent move is the start of a sustainable rerating or just a short-covering rally in an oversold name.

Fundamentally, the latest quarter gave the bulls fresh ammunition. Revenue rose 17% year over year to $4.65 billion, and earnings per share came in ahead of expectations. Management reaffirmed full-year guidance and flagged double-digit growth in the core consumer tax business during the current filing season, even as overall IRS submissions are slightly down. This combination of outperformance against a tepid macro backdrop and resilient guidance underpins the argument that Intuit remains a high-quality compounder.

Yet Wall Street’s reaction has not been uniformly euphoric. Some banks that are otherwise constructive have trimmed their price targets. JPMorgan cut its target to $605 and Argus reduced its view to $580, while keeping positive ratings in place. On the more cautious side, Morningstar lowered its fair value estimate to $495 and, more importantly, downgraded Intuit’s economic moat from “wide” to “narrow” on rising AI uncertainty. This divergence sets the stage for a nuanced Intuit Analysis rather than a simple buy-the-dip narrative.

Intuit Inc.: How Strong Are the Tax and Small Business Franchises?

Any serious Intuit Analysis has to start with the company’s two economic engines: TurboTax on the consumer side and QuickBooks across small businesses and self-employed users. CEO Sasan Goodarzi recently highlighted that TurboTax is growing revenue by about 12% so far in the current tax season, outpacing the slight decline in total returns submitted to the IRS. That implies modest market share gains and, crucially, suggests that AI-powered alternatives have not yet dented the franchise in the mass market.

Goodarzi and the finance team have consistently argued that tax compliance is not an obvious target for simple, generic AI tools. Errors carry legal and financial liability, and many consumers want support from either professionals or heavily guided workflows. That friction creates a protective layer around TurboTax, especially when combined with Intuit’s ability to integrate live human advice into software flows and to bundle adjacent services, such as credit monitoring and financial planning.

On the small business side, QuickBooks remains the go-to accounting platform for U.S. SMEs, and the company has enriched the ecosystem with payroll, payments and marketing tools via Mailchimp. Switching costs are significant: migrating financial systems is painful, time consuming and risky. This is one reason Morningstar still assigns Intuit a narrow moat, even after the downgrade. Small firms tend to stick with what works once embedded, and specialized workflows are harder to replicate with generic large language models.

However, management is not complacent. A key pillar of its strategy is turning QuickBooks into a distribution platform for third-party AI solutions. In practice, that means leveraging the reach to millions of small business customers to offer domain-specific AI agents that handle tasks like invoicing, cash-flow forecasting and marketing automation. In this respect Intuit is trying to play a role for enterprise productivity similar to what NVIDIA plays in AI infrastructure or Apple in consumer devices: own the channel, not just the feature.

Intuit Analysis: Is AI a Threat or a Hidden Tailwind?

Fears that AI could render tax and bookkeeping software obsolete have clearly weighed on the stock, particularly as tools like Claude, ChatGPT and other assistants demonstrate that they can process and summarize complex documents rapidly. For many investors, it is easy to imagine a future where a consumer uploads a 1099 and W-2 into a chatbot and receives a complete return without ever touching TurboTax.

The reality, at least for now, looks more nuanced. Intuit has already embedded AI across its product suite, focusing on “done-with-you” and increasingly “done-for-you” services. That means the software does more of the data entry, categorization and recommendation work, while still operating inside a regulatory-compliant and auditable environment. The CFO has emphasized that just because individuals have direct access to AI models does not mean they will abandon specialized software that integrates bank feeds, payroll data, receipts and filings in a cohesive system.

From an investment perspective, this is where the Intuit Analysis becomes less binary. AI is simultaneously a risk—because it lowers barriers for new entrants—and an opportunity, because it can make Intuit’s existing offerings more valuable and more profitable. If Intuit can charge more for AI-enhanced workflows, increase attach rates for advisory services and lower support costs, margins could actually expand over time despite rising marketing investments.

Morningstar’s decision to cut the moat rating and fair value estimate to $495 captures the risk side of that equation, reducing the margin of safety investors can ascribe to future cash flows. Yet at around $465, the stock still trades modestly below that intrinsic value estimate, leaving room for upside if Intuit executes on its AI roadmap and the most pessimistic scenarios fail to materialize. TD Cowen has already argued that sector-wide AI fears are “overdone” in relation to Intuit’s latest results, suggesting that sentiment may have overshot fundamentals.

Intuit and the Direct File Question: Policy Risk You Can’t Ignore

The most distinctive overhang in this Intuit Analysis is not technological but political. Democrats in Washington are pushing to make the IRS Direct File program a permanent, government-run tax filing service. In its current form, Direct File targets taxpayers with simple financial situations and relatively straightforward returns, a core segment of TurboTax’s mass-market base.

If the program becomes permanent and widely adopted, it could gradually erode Intuit’s low-complexity customer pool, pressuring both volume and pricing at the bottom of the funnel. In isolation, losing some free and low-ARPU users may not sound catastrophic, but it could blunt cross-selling opportunities into premium offerings such as live human advice, audit defense and financial products.

Management has pushed back gently on the long-term threat, arguing that many filers will still prefer commercial products with richer guidance, better usability and integrated financial tools. But policy risk is, by nature, difficult to model and can change with election cycles. For U.S. investors, the IRS Direct File initiative introduces a structural headwind that is less about year-to-year earnings and more about how big the total addressable market really is over the next decade.

This helps explain why some analysts, while maintaining bullish stances, are tempering their price targets. JPMorgan’s and Argus’ reductions, alongside Morningstar’s more cautious stance, signal that even optimists are now baking in some level of long-run pressure from public-sector competition and a more automated tax landscape.

How Wall Street Ownership and Insider Moves Shape the Setup

Institutional investors still overwhelmingly dominate Intuit’s shareholder base, with roughly 84% of the float held by large funds. Recent filings show a mixed but generally constructive picture. Crossmark Global Holdings increased its stake by about 15.8% to more than 47,000 shares, while Dimensional Fund Advisors grew its position by nearly 5% to over 600,000 shares. CI Investments also added to its holdings, signaling continued confidence in the long-term story.

At the same time, some institutions have been trimming exposure. Amova Asset Management cut its stake by close to 30%, and Segall Bryant & Hamill reduced its position almost by half. This two-way flow is consistent with a market trying to recalibrate AI and regulatory risks rather than abandoning the name outright. The resulting ownership structure still skewed toward long-only, fundamentals-driven investors gives Intuit a relatively stable base compared with more speculative software peers.

Insider activity tilts more cautious. Several executives, including the CEO and other senior leaders, have been net sellers in recent months. While insider selling does not automatically signal trouble—executives often diversify or exercise options—it does reduce one potential bullish argument, especially when paired with a stock that has been under pressure. For momentum-oriented investors, the combination of insider selling and a still-soft technical backdrop is a reason to size positions conservatively.

Competitive Landscape: Where Intuit Sits Among U.S. Tech Leaders

Within the broader U.S. technology complex, Intuit occupies an interesting middle ground. It is not a hyperscale cloud provider or an AI hardware story like NVIDIA, nor is it a consumer hardware and ecosystem player like Apple or an automotive-disruption narrative like Tesla. Instead, it sits in the “applied software” layer that turns financial and regulatory complexity into usable workflows.

That positioning has historically supported premium valuation multiples, driven by high recurring revenue, strong margins and predictable cash flows. Even after the drawdown, Intuit still trades at a richer multiple than many enterprise software peers, reflecting both its durable franchises and the scarcity of scaled, profitable growth names in the financial technology niche.

For portfolio managers balancing growth and quality, Intuit continues to screen as an attractive core holding relative to smaller, less profitable fintechs. However, the step-down from a “wide” to a “narrow” moat should not be overlooked. It suggests that the gap between Intuit and both legacy competitors and AI-native insurgents may narrow over time, potentially limiting multiple expansion.

Investors should also recognize that macro or sector rotations can overshadow company-specific progress in the short term. In a risk-off environment where yields are rising, longer-duration software names often de-rate together, regardless of fundamentals. A disciplined Intuit Analysis therefore needs to separate cyclical pressure—which can create buying opportunities—from structural threats like Direct File and generative AI commoditization.

Valuation, Risk/Reward and Portfolio Role in This Intuit Analysis

With the stock around $465 and Morningstar’s fair value at $495, Intuit trades at a modest discount to one well-known intrinsic value estimate, though still below the more optimistic targets from JPMorgan and Argus. The market is implicitly assigning a probability that AI and policy risks will shave a few percentage points off long-term growth or compress margins relative to the company’s historical trajectory.

On the positive side, the business is executing well: double-digit top-line growth, strong EPS, a reaffirmed outlook and a board-approved quarterly dividend of $1.20 per share all signal confidence. The company continues to invest heavily in marketing ahead of the April 15 tax deadline, which may pressure near-term profitability but is aimed at defending and expanding its user base in a competitive season.

On the risk side, there are multiple fronts to monitor: Direct File’s evolution, further shifts in analyst moat assessments, insider selling trends and any evidence that AI-native tools are gaining real traction among TurboTax or QuickBooks customers. For now, the data points tilt toward resilience rather than disruption, but the margin for error has undeniably narrowed.

For U.S. and international investors, Intuit’s role in a portfolio should reflect this balance. It is still a high-quality, cash-generative software name that can anchor a fintech or software sleeve, but it no longer looks like an unassailable compounder. Position sizing, entry price and risk controls matter more than they did when the competitive moat was universally considered wide.

Conclusion

Putting this Intuit Analysis together, the stock appears attractively positioned for investors with a multi-year horizon who believe management can harness AI as a tailwind rather than succumb to it, and who see Direct File as a contained, though real, policy risk. For shorter-term traders, however, the mix of policy noise, insider selling and sector-wide AI narratives suggests that volatility is likely to remain elevated, and that patience will be required to harvest the underlying earnings power.

Further Reading

- Intuit Inc. (INTU) Stock Price, Quote & News (Yahoo Finance)

- Intuit Inc. Posts Strong Earnings Amid Sector-Wide AI Concerns (Finviz)

- Intuit: We Lower Moat Rating, Cut Fair Value Estimate on Reduced Certainty Around AI (Morningstar)

- Intuit Inc. Shares Bought by Crossmark Global Holdings Inc. (MarketBeat)