Will Meta AI Regulation turn today’s court setbacks and massive AI spending into a long-term drag on one of tech’s biggest winners?

How are courts reshaping Meta’s risk profile?

Meta has been hit by a series of jury verdicts that found the company did not sufficiently control its platforms and thereby exposed minors to harm. Two separate juries concluded that internal research painted a more critical picture of social‑media risks than Meta’s external communications suggested, with a former Facebook executive testifying that internal findings “did not align with how the company presented itself publicly.” Meta and Alphabet face financial penalties and are appealing, but the decisions mark a turning point: liability that was once hypothetical is now material and quantifiable.

The new rulings come on top of earlier legal pressure that already linked social‑media usage to potential addiction and mental‑health issues among younger users. For equity holders, the key shift is that juries are increasingly willing to look inside internal studies and product‑safety processes, not just at public marketing claims. That raises the odds that future plaintiffs, state attorneys general and regulators will target internal AI‑driven ranking algorithms and recommendation systems, which could sit at the heart of any broad Meta AI Regulation package.

The market has noticed. Meta’s stock has fallen roughly a third from its 2025 highs and is still down sharply year to date despite Monday’s 1.38% rebound. Last week alone, the shares dropped around 11%, part of a wider tech correction that saw the Nasdaq log its worst week in months. The selloff has been amplified by headlines linking Meta’s name to youth safety, social‑media addiction and possible digital taxes, raising the specter of long‑running legal overhangs similar to what legacy tobacco and opioid manufacturers faced.

What does Meta AI Regulation mean for AI spending?

Meta sits at the center of the global AI build‑out. Alongside Amazon, Microsoft, Alphabet and Oracle, the company is one of the hyperscalers driving an unprecedented capital‑expenditure cycle in data centers, networking and compute. Industry estimates suggest these giants could collectively deploy more than $650–700 billion in AI‑related capex in 2025 and 2026, with Meta and Microsoft among the most aggressive spenders this year. That level of investment is pulling the entire AI supply chain higher, from chip designers like NVIDIA to power‑grid operators and network vendors.

For Meta, however, the question is no longer whether it can fund the build‑out – its balance sheet and cash flows remain robust – but whether the returns will be commensurate. The company’s AI Superintelligence Lab and generative‑AI initiatives are already improving ad targeting and automated creative, helping to drive a strong rebound in operating cash flow since 2022. Meta’s family of apps attracted about 3.58 billion daily users in December 2025, giving it unmatched reach to monetize AI‑powered products across Facebook, Instagram, WhatsApp, Messenger and Threads.

Still, Wall Street is shifting from the “promise” phase of AI to a “show me the money” phase. Capital markets are increasingly intolerant of open‑ended capex without clear revenue payoffs. Several high‑growth software names have seen their valuations crushed as investors questioned their ability to adapt to AI; Meta, in contrast, trades at roughly 17x–19x forward earnings and around 9x forward cash flow, making it one of the cheaper members of the Magnificent Seven. Yet the more Meta AI Regulation becomes a live possibility, the more investors must discount long‑duration AI cash flows for potential compliance costs, product redesigns and constrained data access.

Is the Magnificent Seven leadership at risk?

The recent correction has hit the Magnificent Seven unevenly. While Tesla and Apple command far higher forward price‑to‑cash‑flow multiples – with Tesla priced for near‑perfection and Apple still richly valued despite slower growth – Meta and Amazon screen as the relative bargains of the group. Based on forward cash‑flow estimates, Meta trades at roughly a one‑third discount to its own five‑year average multiple, while Amazon also sits well below its historical norms. That divergence reflects both the legal overhang around Meta AI Regulation and concerns that AI capex could compress margins before new revenue streams fully ramp.

Yet Meta’s operating fundamentals remain powerful. Digital advertising is still its core engine, and AI is a tailwind there rather than an unproven side bet. Generative models already help automate ad creation, optimize bidding and better match campaigns to users, improving click‑through rates and pricing power. On top of that, Meta has barely begun to monetize WhatsApp and Threads with advertising, and is exploring commerce integrations that could further deepen its moat.

In the broader market context, the S&P 500 and Nasdaq remain well above their 2025 troughs, even as Meta now trades near levels last seen during the tariff‑driven volatility of April 2025. That suggests the stock’s drawdown is more company‑specific than purely macro‑driven. Investors are selectively punishing those mega‑caps seen as taking on the heaviest AI spending burdens and the greatest regulatory risk. Microsoft and Meta have been singled out on both counts, even though their balance sheets arguably make them best placed to carry those costs.

How are Wall Street analysts reacting to Meta’s AI risks?

Analysts remain divided on how to balance Meta’s legal and regulatory exposure against its improving fundamentals and relatively low valuation. Morgan Stanley recently cut its price target on Meta to $775 per share, explicitly citing weaker sentiment around generative AI and rising concern over regulatory setbacks, including the latest social‑media safety verdicts. The bank still sees long‑term upside, but the lower target reflects a higher risk premium for legal outcomes and AI strategy execution.

RBC Capital has also highlighted Meta as one of the large‑cap tech names that suffered double‑digit percentage losses during the latest pullback, noting that some of the issues haunting the stock – from elevated capex to regulatory scrutiny – pre‑dated geopolitical shocks and are not just a by‑product of war‑related uncertainty. At the same time, RBC emphasizes that earnings across the mega‑cap tech cohort remain robust and that the sector continues to drive aggregate profit growth for the U.S. equity market. In this framework, significant and sustained damage to tech earnings would likely be needed to pull the S&P 500 into deeper negative territory.

Other research shops and asset managers stress that at around 17x forward earnings, Meta looks more like a value stock than a bubble name, despite its AI story and platform dominance. They argue that the market has already priced in a substantial portion of the bad news – from Meta AI Regulation risk to legal liabilities and higher operating costs – while potentially underestimating future monetization from AI tools, commerce integrations and new hardware categories such as smart glasses.

Can Meta’s product strategy offset legal and AI headwinds?

On the product side, Meta is pushing ahead with new initiatives that could diversify revenue beyond traditional feed and stories ads. The company is preparing to launch two new Ray‑Ban smart‑glasses models designed specifically for prescription‑lens wearers, to be distributed primarily through optician channels. Chief executive Mark Zuckerberg has likened the opportunity in smart eyewear to the early days of smartphones, arguing that integrating AI assistants into everyday devices could open a large new market over time.

In Q4 2025, Meta delivered revenue of about $59.89 billion and adjusted EPS of $8.88, beating Wall Street expectations on both top and bottom lines. That performance underscores that, for now, AI‑enhanced advertising and cost discipline are more than offsetting heavy investments in infrastructure and Reality Labs. Still, the Reality Labs segment – which includes VR, AR and metaverse projects – continues to burn cash, and investors remain skeptical about its near‑term payoff.

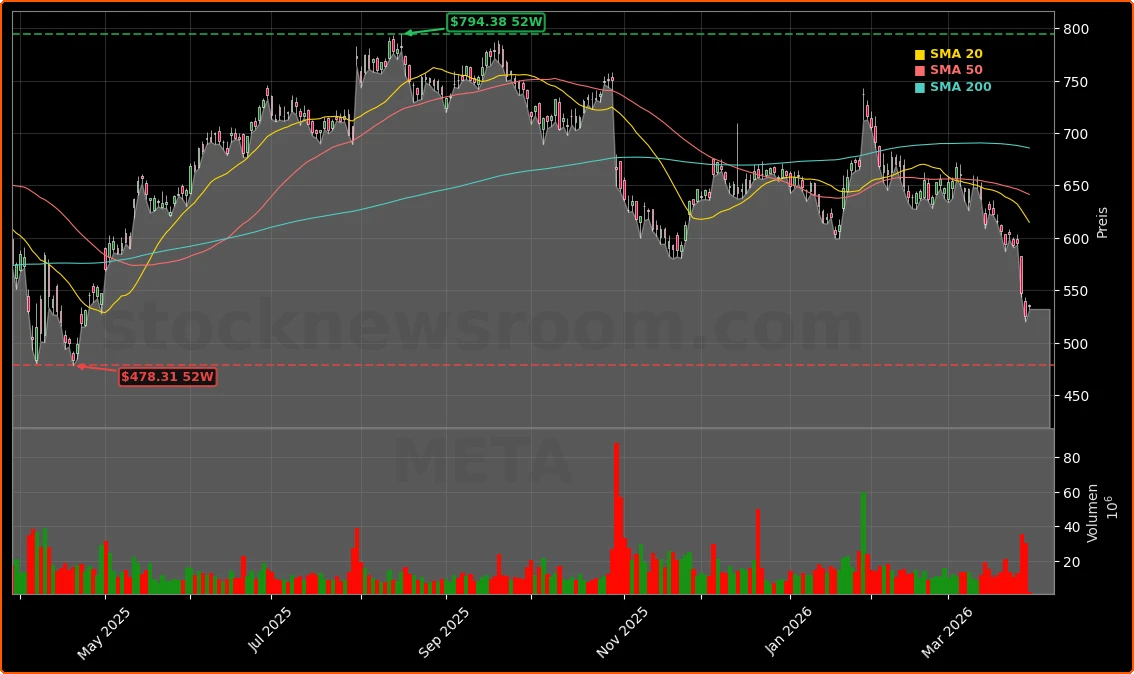

Technically, Meta shares show signs of exhaustion after the sharp drawdown. The area around $487 has emerged as an important support level on the chart, and momentum indicators such as the daily RSI recently fell into oversold territory. That backdrop may attract tactical buyers who see the stock as washed out in the short run, even as long‑term investors grapple with how far Meta AI Regulation and litigation could ultimately go.

There is also a strategic angle: some market participants argue that tougher regulation and litigation might actually entrench incumbents like Meta and Alphabet. Just as large legal settlements and compliance regimes ultimately made it harder for new entrants to challenge big tobacco, stringent AI safety and content rules could raise fixed costs and legal barriers for upstart social‑media and AI platforms. If that scenario plays out, today’s legal setbacks could paradoxically reinforce Meta’s long‑term competitive position – albeit at the cost of near‑term volatility and higher operating expenses.

Related Coverage

Investors looking for a deeper dive into the legal overhang can read how a recent wave of youth‑safety lawsuits sparked a sharp selloff in Meta’s shares in Meta Social Media Lawsuits: -6.8% Plunge Jolts Investors, which explores whether courtroom risk could permanently compress the stock’s valuation multiple. For a broader perspective on how AI volatility is affecting the entire infrastructure stack, including key Meta suppliers, the analysis in NVIDIA AI Strategy -2.2%: Crash Or $4 Trillion Reset For AI? examines whether the latest pullback in NVIDIA’s AI franchise signals a deeper reset or simply a new entry point into the next AI capex super‑cycle.

Internal research did not align with how the company presented itself publicly.— Brian Boland, former Facebook manager (court testimony summary)

Meta AI Regulation has rapidly evolved into a defining theme for both the company and the wider AI trade, intertwining courtroom risks, potential new rulebooks and massive, front‑loaded investment. For U.S. investors, the stock now represents a high‑beta bet on whether AI monetization can outrun legal, political and regulatory headwinds. The next few quarters – including any legislative moves on AI and further jury decisions – will show whether Meta can convert today’s uncertainty into durable earnings power and reclaim its leadership role in the market’s AI narrative.