Can Meta’s aggressive AI strategy and $21 billion CoreWeave bet turn a volatile mega-cap into the market’s next AI powerhouse?

How does Meta AI Strategy reshape the stock story?

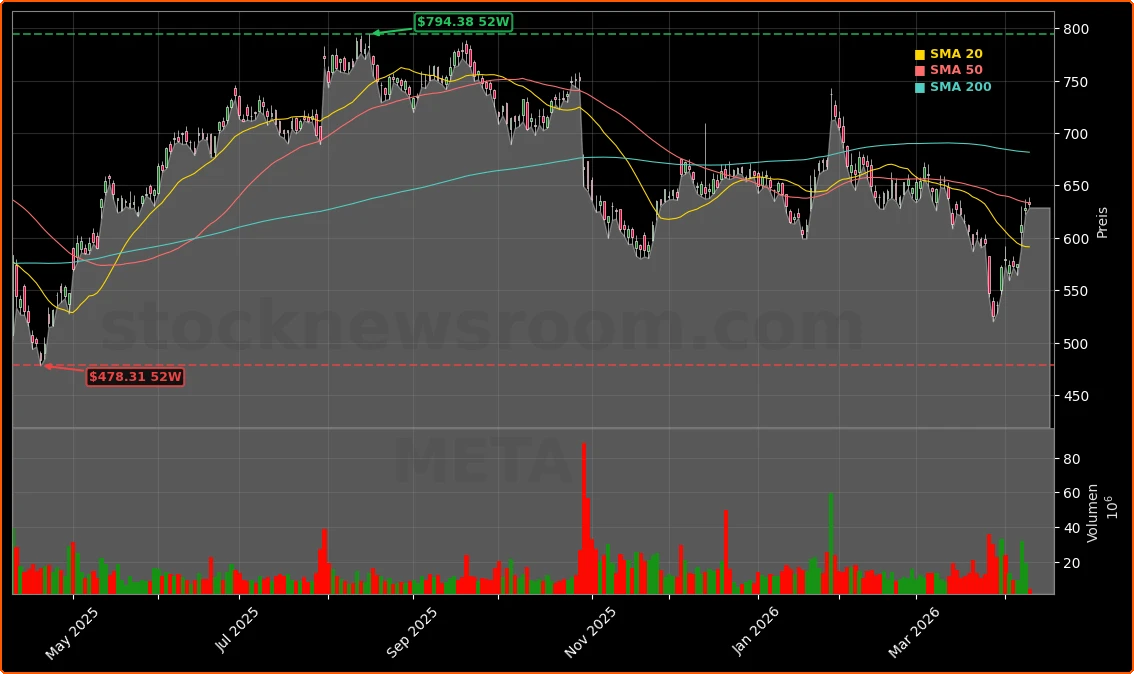

Meta shares were recently changing hands around $632.27, up modestly on the day and still well below last year’s peak near $800, after a volatile stretch driven by geopolitical shocks and court setbacks. Yet sentiment is notably less euphoric than it was at the top: tech sector valuation multiples have compressed sharply, and Meta now trades at roughly 19–21 times projected earnings, making it one of the cheaper mega‑cap growth names in the S&P 500.

The centerpiece of the current Meta AI Strategy is twofold: first, turning its more than 3 billion daily users into a distribution edge for consumer AI; second, securing the compute, networking and chip stack needed to chase so‑called “superintelligence” over the next decade. That combination positions Meta as both an AI applications play and an infrastructure‑demand engine for suppliers from CoreWeave and Corning to NVIDIA and Arm.

J.P. Morgan recently reiterated a Buy rating on Meta with an $825 price target, arguing that the market underestimates how quickly AI features can be monetized inside Meta’s dominant ad platforms. CFRA also upgraded the shares to “Strong Buy,” citing the potential for new models, cost discipline and a resilient ad business to drive the next leg of earnings growth.

What’s in the CoreWeave and chip build‑out?

The latest expansion of Meta’s cloud‑capacity agreement with CoreWeave lifts the total commitment to about $21 billion through December 2032, on top of an existing $14.2 billion deal. Dedicated capacity will be deployed across multiple data centers, including some of the first installations of NVIDIA’s Vera Rubin platform, aimed at large‑scale inference workloads. For CoreWeave, backed by an additional $2 billion investment from NVIDIA, the contract helps fund a rapid build‑out of AI data centers.

Beyond CoreWeave, Meta has signed substantial GPU supply agreements with NVIDIA and AMD, is among the earliest customers for Arm’s new AGI‑focused CPU designs, and is developing its own MTIA 400 accelerator, targeting a better price‑performance ratio for internal inference. On the networking side, Meta recently agreed to a multi‑year optical‑fiber pact with Corning valued at up to $6 billion, supporting the high‑bandwidth connectivity its AI clusters require.

The cost is staggering. Meta’s capital expenditures jumped 84% last year to more than $72 billion and could reach as high as $135 billion this year, with Wall Street models projecting AI‑heavy capex above $100 billion annually for at least four more years. Including a recruiting surge for top‑tier AI researchers—some on nine‑figure pay packages—R&D spending is expected to climb more than 40% this year to around $81 billion.

How strong is the Muse Spark AI model?

Muse Spark—code‑named “Avocado” internally—is the first release from Meta’s new Superintelligence Labs and a clear reset after the delayed rollout and underwhelming benchmarks of the Llama family. Independent evaluators now place Muse Spark alongside top offerings from OpenAI, Google and Anthropic, a sharp improvement over Llama, which languished at the bottom of many rankings.

The Meta AI Strategy centers on deploying Muse Spark everywhere users already spend time: in the Meta AI app, inside the Facebook and Instagram feeds, and across WhatsApp for tasks like travel planning, shopping assistance and content generation. With more than 3 billion users, even modest per‑user AI monetization via higher ad relevance, sponsored recommendations or paid AI tools could move the needle meaningfully on revenue and margins.

Analysts such as Wedbush’s Dan Ives describe the stock as “dirt cheap” relative to its AI optionality and expect Muse technology to be a direct challenge to OpenAI and Anthropic in consumer engagement. Some observers also note that Meta appears to be quietly de‑emphasizing its open‑source Llama branding, signaling a strategic shift toward more tightly controlled, high‑end proprietary models.

Can Meta balance AI growth with legal and EU risks?

The bullish narrative around the Meta AI Strategy is playing out against an unusually heavy legal and regulatory backdrop. In the U.S., Meta faces thousands of lawsuits from individuals and school districts alleging its platforms were intentionally designed to be addictive to minors, contributing to serious mental‑health issues. Recent jury verdicts in California held Meta and YouTube liable for harms linked to social‑media use, prompting comparisons to the tobacco litigation wave of the 1990s.

Financially, the initial damage has been small—about $6 million in combined damages so far, a fraction of the cash flow Meta generates in a single hour—but the precedents matter. A sustained legal onslaught could ultimately force changes to product design, marketing practices or even lead to a large settlement, all while Meta is pouring more than half of its projected revenue into AI capex.

In Europe, the company is appealing more than EUR 6 billion in antitrust and Digital Markets Act fines levied on large U.S. tech firms since 2024, including penalties related to Facebook Marketplace and Meta’s controversial “pay or consent” advertising model. Brussels has also warned Meta over potentially excluding third‑party AI assistants from WhatsApp, highlighting how AI integration itself is becoming a regulatory flashpoint.

Despite these headwinds, many portfolio managers still see Meta primarily as a dominant, highly profitable ad platform with AI as a long‑duration growth kicker. Online advertising remains cyclical—revenues fell sharply in the 2021–2022 slowdown—but Meta’s 24% year‑on‑year revenue growth in a recent quarter underscores how quickly the business can rebound when macro conditions improve.

Related Coverage

For a deeper dive into how this latest Muse Spark release and the CoreWeave agreement fit into the broader capital‑spending picture, readers can explore Meta AI Strategy +4.0%: Muse Spark and $21B CoreWeave Boom, which analyzes whether these massive commitments can translate into durable shareholder returns. Investors tracking AI competition beyond social media may also want to read Palantir Anthropic -5.9% plunge: AI rivalry shocks PLTR, discussing how intensifying model rivalries can reprice expectations across the broader AI stock universe.

Muse Spark clearly establishes Meta as an active and credible participant in the model race standing shoulder-to-shoulder with leading players.— Mark Shmulik, Bernstein analyst

Ultimately, the Meta AI Strategy now defines how Wall Street values the company: a capital‑intensive push toward frontier models and proprietary infrastructure, backed by one of the world’s most profitable ad engines. For U.S. and global investors, the key questions are whether Muse Spark and follow‑on models can drive measurable monetization across Meta’s apps and whether legal and regulatory outcomes stay manageable. The next few quarters of user engagement data, ad trends and AI product launches will show if this high‑stakes bet can justify Meta’s growing place in tech‑heavy portfolios.