Can Meta’s aggressive AI strategy turn massive infrastructure spending and Muse Spark into sustainable upside for investors?

Is Muse Spark enough to reset expectations?

Muse Spark is Meta’s first major large language model in more than a year and the debut product of the Meta Superintelligence Labs unit led by former Scale AI CEO Alexandr Wang. Unlike the open‑weight Llama family, Muse Spark is a closed, proprietary model that already powers the Meta AI app and will roll out across Facebook, Instagram, WhatsApp and Ray‑Ban smart glasses in the coming weeks. Internally, Meta is positioning the model as a compact but capable native multimodal system that can process text and images simultaneously and serve as the foundation for future “agentic” AI products that act on users’ behalf rather than just answer questions.

Early independent tests indicate Muse Spark is competitive with frontier models from OpenAI and Anthropic in language, reasoning and health‑related queries, and it reportedly outperforms xAI’s Grok on many benchmarks. However, the model still lags rivals on coding and some higher‑order reasoning tasks, underscoring that Meta remains a fast follower rather than a clear leader. CEO Mark Zuckerberg has framed Muse Spark as the “first step on our scaling ladder” after a ground‑up overhaul of Meta’s AI stack, emphasizing trajectory over perfection in this first release of the new Meta AI Strategy.

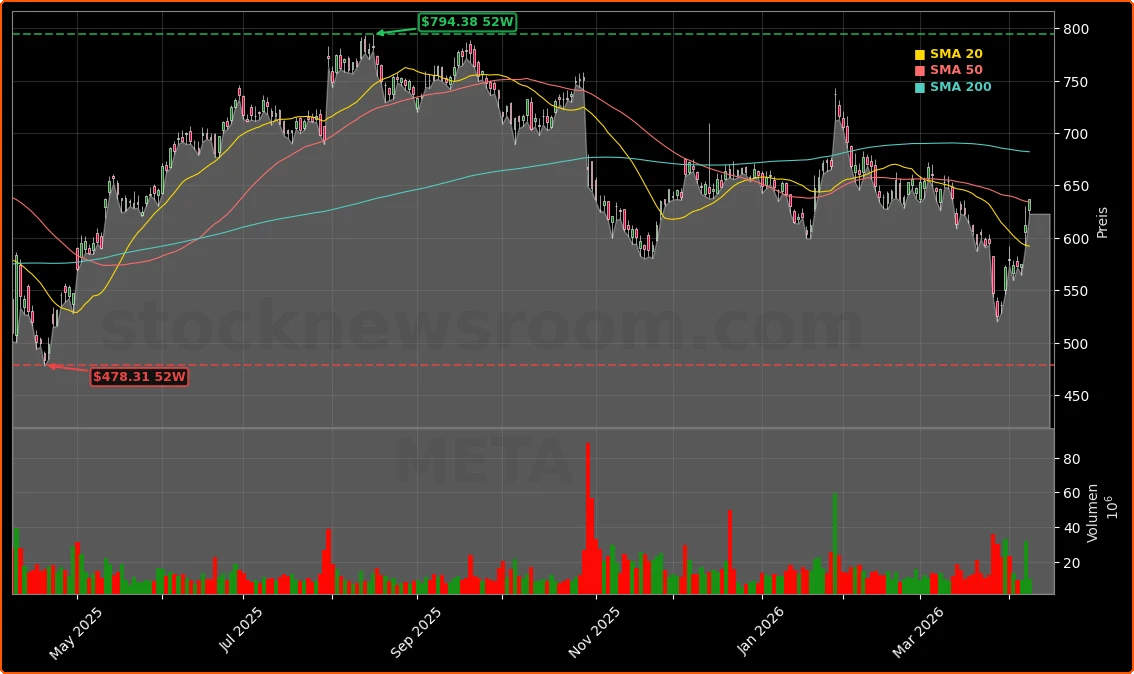

Despite the technical caveats, Wall Street liked what it saw. Meta’s market cap rose by roughly $100 billion on the announcement day, signaling relief that a year of heavy AI hiring and restructuring is at last producing visible product output. For NASDAQ and S&P 500 investors who watched Meta drop double digits earlier this year on capex worries and youth‑safety litigation, Muse Spark is being interpreted as an early proof point rather than a finished competitive endpoint.

How central is CoreWeave to Meta AI Strategy?

On Thursday, Meta and CoreWeave disclosed an expanded AI cloud deal that commits Meta to about $21 billion in additional spend on CoreWeave’s GPU‑rich infrastructure through December 2032. This builds on a prior AI cloud agreement worth up to $14.2 billion, bringing total potential CoreWeave‑related spending above $35 billion. The new contract includes some of the first large‑scale deployments of NVIDIA’s Vera Rubin platform across multiple data center locations, tailored for large‑scale inference workloads.

For Meta, the deal clarifies a portfolio approach to infrastructure: continue to build massive in‑house data centers—such as the recently announced $10 billion Texas facility—while leaning on specialized cloud providers like CoreWeave and Nebius to bridge capacity gaps and manage demand spikes. Meta has also lined up AI infrastructure partnerships with Google Cloud and is in talks with Oracle for an additional multi‑year arrangement reportedly worth around $20 billion. That makes the Meta AI Strategy one of diversification and redundancy in compute, an important hedge as training and inference demands surge.

From a market standpoint, the CoreWeave expansion reinforces two themes. First, Meta is now one of the most aggressive spenders in the Magnificent Seven on AI infrastructure, alongside Apple, Microsoft and Amazon. Second, it underlines how intertwined Meta’s fortunes are with upstream suppliers in chips and optics—from NVIDIA GPUs and AMD accelerators to Corning’s $6 billion optical‑cable agreement and Arista Networks’ AI switching platforms supporting clients like Meta.

Can Meta monetize AI fast enough for Wall Street?

Analyst commentary following the Muse Spark reveal has been broadly constructive but focused on execution risk. KeyBanc’s Justin Patterson kept an Overweight rating while trimming his price target to $760, arguing that Meta’s frontier model progress and practical ad tech applications remain underappreciated. Citi’s Ronald Josey reiterated a Buy rating with an $850 target, saying the launch removes an overhang around delayed AI releases and adds visibility into the longer‑term roadmap for personal superintelligence and engagement‑driven monetization.

The near‑term monetization path is less about selling AI APIs to developers—the lane dominated by OpenAI, Anthropic and Google—and more about using Muse Spark and subsequent models to enhance Meta’s core advertising engine. Analysts at firms such as Morningstar and Citizens have highlighted that the “killer use case” for Meta AI Strategy is better targeting, higher‑quality creative and more engaging ad formats inside feeds and Reels. With roughly $200 billion in annual ad revenue and more than 3 billion monthly users across its apps, even small improvements in conversion and ad quality can translate into outsized earnings leverage.

There are still significant overhangs. Meta faces thousands of youth‑safety lawsuits, with recent jury verdicts finding the company partially liable for alleged mental‑health harms linked to social media. At the same time, Meta is trimming legacy roles in California and elsewhere as it reallocates billions toward AI talent and compute, alongside hefty ongoing losses in Reality Labs. For U.S. portfolio managers, that combination of legal risk, margin compression and capex intensity keeps Meta’s risk profile higher than peers like Tesla or some software‑only AI beneficiaries.

Related Coverage

Investors who want a deeper dive into the short‑term stock reaction can read how the model unveiling sparked a sharp move higher in Meta Platforms Muse Spark +6.2% Surge Shocks Wall Street, which dissects whether this AI catalyst can turn elevated capex into a fresh leg up for the shares. For broader AI infrastructure exposure beyond platforms like Meta, our piece on chip supplier Marvell explores whether its latest upgrade marks an inflection point: Marvell Technology Upgrade +6% Rally After Barclays Shock looks at how networking silicon is becoming a core bottleneck in hyperscale AI data centers.

We plan to release increasingly advanced models that push the frontier of intelligence and capabilities, including new open source models.— Mark Zuckerberg, CEO of Meta Platforms

The revamped Meta AI Strategy—anchored by Muse Spark and a $21 billion CoreWeave expansion—moves Meta from AI rhetoric to tangible deployment, but the company still has to prove it can turn agentic AI and smarter ads into durable profit growth. For long‑term U.S. investors, Meta now offers a high‑beta way to play both consumer AI adoption and the AI infrastructure build‑out, albeit with elevated legal and spending risk. The next earnings reports and product rollouts will show whether this strategy can sustain revenue acceleration and support further multiple expansion on Wall Street.