Is the Meta AI Strategy a visionary long-term growth engine or a risky $70+ billion capex gamble with deep layoffs attached?

[fxmag_hero_image]

Is Meta rewriting the AI playbook?

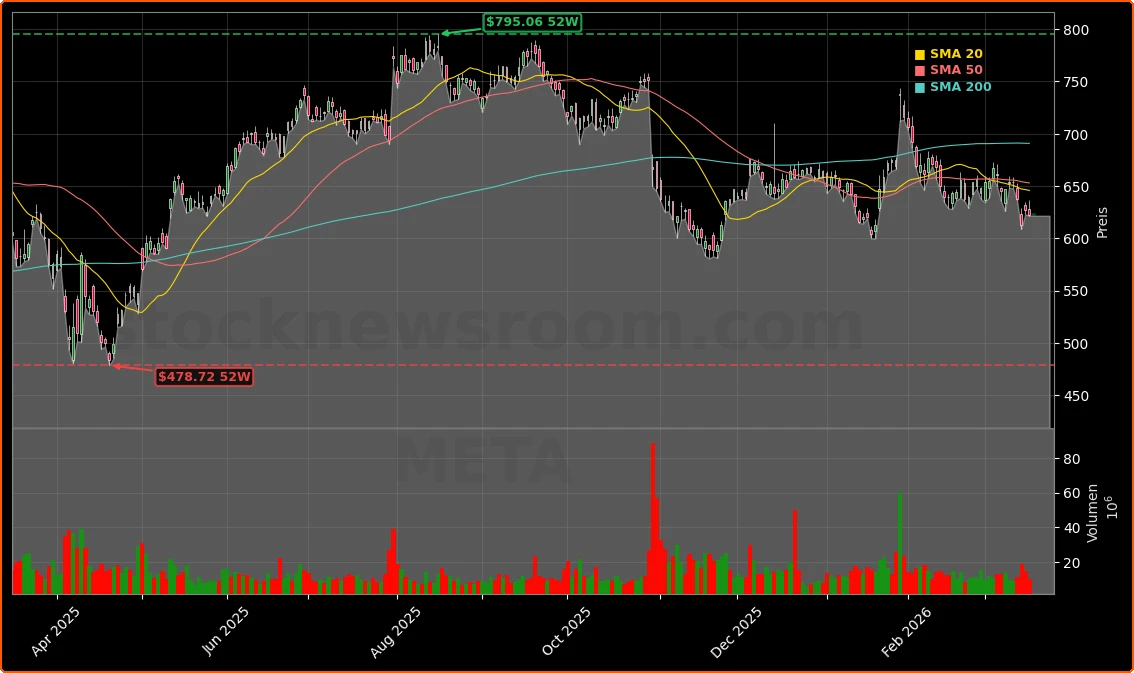

Meta Platforms, Inc. closed regular trading on Tuesday at about $622 per share, down slightly on the day and roughly 15% below recent peaks, as investors reassess the Meta AI Strategy. Despite the pullback, Meta remains one of the largest weights in the NASDAQ and S&P 500, with analysts like Citizens maintaining a Market Outperform rating and a bullish $900 price target. Citizens points to a 17% year‑over‑year jump in global time spent across Meta’s apps for seven straight months, highlighting how AI‑driven relevance is lifting Instagram engagement and ad monetization.

Under the Meta AI Strategy, the company is shifting from a pure social media play to what management describes as a “circular AI architect”—designing its own hardware stack, recycling critical materials and optimizing AI workloads across Facebook, Instagram, WhatsApp and new agent platforms. Q3 2025 revenue reached $51.2 billion, up 26% year over year, with operating income of $20.5 billion and an impressive 40% margin before a one‑time tax hit. Reels surpassed a $50 billion annualized revenue run rate and automated ad solutions topped $60 billion, underscoring the leverage of AI in Meta’s ad engine.

Why tie billions to Nebius and rare‑earth supply?

The most eye‑catching move in the Meta AI Strategy is a five‑year AI infrastructure deal with Nebius, valued at up to $27 billion. Nebius will supply cloud capacity and Nvidia GPU‑based AI compute, aiming to scale from 170 megawatts of power to 5 gigawatts by 2030. Morningstar estimates the Nebius contract could generate $4–$6 billion in annual recurring revenue for Nebius, while giving Meta long‑term access to high‑end AI capacity as demand for model training and inference explodes.

At the same time, Meta is attacking the capex bottleneck from the hardware side. Working closely with AMD, Meta co‑developed the Helios rack‑scale architecture, built around modular AI accelerators such as custom Instinct MI450 variants. Helios is designed for rapid disassembly so Meta’s labs can recover high‑value rare‑earth magnets and optical components in minutes, easing dependence on constrained supply chains dominated by China. This circular approach to AI hardware separates Meta from rivals like NVIDIA and traditional hyperscalers, potentially lowering long‑term capex while keeping AI capacity high.

Meta is also experimenting with next‑generation energy solutions. It has partnered with Oklo on a planned nuclear campus in Ohio to power future data centers, a sign that the Meta AI Strategy extends from chips and software all the way down to electricity and materials.

How do layoffs fit into Meta AI Strategy?

The flip side of Meta’s AI push is aggressive cost cutting. Reports point to layoffs of around 20% of staff—roughly 15,000 jobs—during 2026, coming on top of the 20,000 positions eliminated in the 2022–2023 “year of efficiency.” Management is effectively telling Wall Street that payroll, not AI capex, is where the knife will fall. For investors, this raises both margin optimism and execution risk: AI tools may boost the productivity of remaining employees, but sustained morale and innovation will be crucial as compute intensity rises.

Meta’s capital expenditures already surged to $19.4 billion in its latest reported quarter, with full‑year guidance lifted to $70–$72 billion and an explicit signal that AI investments will accelerate again in 2026. Critics warn of an “AI bubble” across the Magnificent Seven, and some strategists expect capital to rotate toward suppliers of power, memory, and materials rather than hyperscalers themselves. Still, bullish voices on Wall Street, including detailed work arguing that Meta trades near 16x adjusted 2026 earnings, see the Meta AI Strategy as a long‑duration growth driver rather than a capex trap.

Meta is no longer just buying AI infrastructure, it is architecting the entire stack—from rare-earth magnets and nuclear power to agent platforms and ad auctions.— Independent Wall Street technology strategist

Competition is intense. Apple, Tesla and other mega‑caps are also leaning into AI‑heavy ecosystems, while AMD and NVIDIA battle for accelerator dominance. Yet Meta’s combination of AI‑enhanced engagement, circular hardware design and large‑scale cloud partnerships gives it a differentiated path. The acquisition of Moltbook, a social networking platform for AI agents, and multi‑year content and commerce integrations across partners from News Corp to MONAT show that Meta is positioning AI not just as infrastructure, but as a front‑end user experience.