Can Meta’s massive AI infrastructure gamble and deep Arm partnership really turn today’s CapEx shock into tomorrow’s profit engine?

How does Meta’s AI spending hit Wall Street?

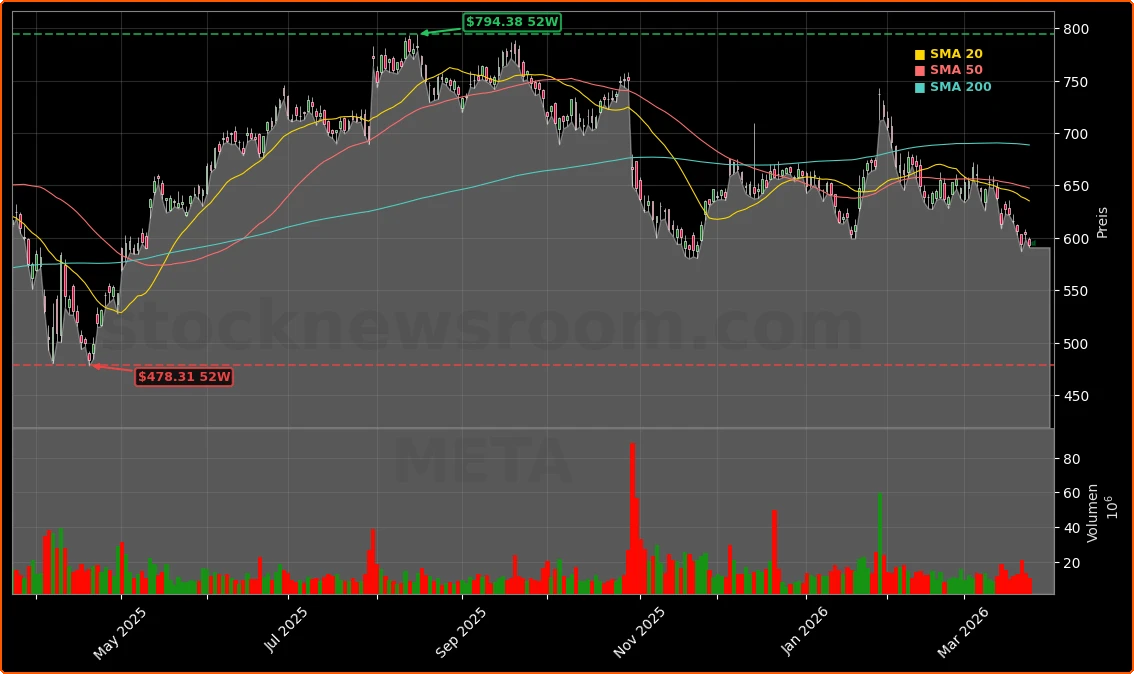

Meta shares have rallied sharply over the past year but now trade below recent highs as the market digests unprecedented AI capital intensity. In Q4 2025, Meta’s advertising revenue climbed to $58.14 billion, up 24% year over year, yet total costs jumped 40%, compressing operating margin from 48% to 41%. Management has guided to $115–$135 billion in 2026 CapEx, largely directed toward data centers, custom silicon and networking to expand Meta Platforms AI infrastructure.

That scale dwarfs many S&P 500 peers and even stands out inside the “Magnificent Seven.” While Apple keeps quarterly CapEx around $2.4 billion and prioritizes buybacks and dividends, Meta is effectively re‑rating itself as an AI infrastructure powerhouse, funding the buildout with rising debt that reached about $58.7 billion. Analysts at major brokers, including Citigroup and Morgan Stanley, still see upside, with consensus price targets around the mid‑$800s implying roughly 40% potential from current levels, but they flag execution and regulatory risk as key overhangs.

Why is Meta partnering so deeply with Arm?

The most symbolic step in this transformation is Meta’s role as lead partner and first major customer for Arm’s new AGI CPU, the British company’s first ever in‑house data center chip designed specifically for AI workloads. The processor targets high‑efficiency inference and agentic AI use cases, with fabrication handled by TSMC. Meta co‑designed the chip and plans to deploy it as a drop‑in replacement for existing compute CPUs across its next‑generation data centers.

Meta engineers emphasize that power is now a hard constraint: wattage at hyperscale sites is scarce, so a best‑in‑class CPU on performance‑per‑watt frees up electrical headroom for dense GPU and accelerator clusters. Embedding Arm’s AGI CPU into Meta Platforms AI infrastructure should lower operating costs per inference, diversify the supply chain beyond x86 vendors, and give Meta more control over its software stack. Arm, for its part, gains a flagship customer as it shifts from pure IP licensing to direct silicon sales, with additional commitments from OpenAI, Cloudflare, SAP and SK Telecom.

How do Nebius and custom chips fit the strategy?

The Arm deal sits alongside an increasingly diversified hardware and data center plan. In mid‑March, Meta signed a five‑year capacity agreement with neocloud provider Nebius Group worth up to $27 billion, including $12 billion of committed AI capacity and an option for another $15 billion. Nebius will deploy large clusters built on Nvidia’s latest Vera Rubin GPUs, giving Meta immediate access to scarce accelerators without bearing all the upfront construction and permitting risk for every data hall.

At the same time, Meta is not abandoning external silicon heavyweights. The company secured major GPU allocations from NVIDIA and Advanced Micro Devices earlier this year and is also collaborating with Broadcom on custom AI XPUs for higher‑efficiency inference at scale. Internally, Meta has rolled out several generations of its Meta Training and Inference Accelerator (MTIA) chips since 2023, aimed at offloading recommendation and ranking workloads from general‑purpose GPUs. Together, these moves suggest Meta Platforms AI infrastructure is evolving into a hybrid of owned data centers, leased capacity and a heterogeneous mix of CPUs, GPUs and custom accelerators.

How does Meta compare with other tech giants?

For U.S. investors, one key question is how Meta’s AI posture stacks up against other mega‑caps. Apple is pursuing an on‑device AI and services strategy with modest data center buildout, while Tesla invests in its Dojo supercomputer to power autonomous driving and robotics rather than broad consumer LLMs. Alphabet and Microsoft are spreading AI bets between internal models and partnerships with OpenAI, Anthropic and others, but so far have not matched Meta’s explicit willingness to sacrifice near‑term margin for bare‑metal infrastructure ownership.

Meta’s pivot is also reshaping its own culture. CTO Andrew Bosworth has been appointed to lead “AI‑native” initiatives and internal AI‑for‑work tools, signaling a shift in focus away from pure metaverse spending toward productivity‑enhancing software on top of the new hardware stack. Regulatory and legal pressures remain, from European privacy rules on less‑personalized ads to U.S. youth safety litigation, but Meta is betting that a unique, cost‑advantaged AI backbone will ultimately outweigh these headwinds in the valuation debate.

Does Meta Platforms AI infrastructure justify the risk?

Whether Meta’s AI super‑spend proves accretive will hinge on the company’s ability to convert compute into new revenue lines and stronger competitive moats. Llama models are already open‑sourced to developers and enterprises, and deeper integration of generative AI into Facebook, Instagram and WhatsApp advertising is driving higher engagement and better targeting. If Arm’s AGI CPU, Nebius capacity and Meta’s own MTIA silicon succeed in cutting inference costs, Meta Platforms AI infrastructure could become a durable barrier to entry for rivals that lack similar scale.

For now, the stock’s pullback reflects understandable concerns that the company may be front‑loading too much risk into a single investment cycle. But Wall Street’s bullish consensus suggests that many institutional investors view this as a rare chance to own a core NASDAQ AI platform before the infrastructure bet fully pays off.

Related Coverage

Investors looking for a deeper dive into the strategic trade‑offs behind this spending wave can explore how Meta’s broader AI pivot is reshaping its business model in Meta Platforms AI Strategy: -1.9% Shock and Metaverse Pivot. For a sector contrast, Apple Maps Advertising Record Boom as Services Surge examines how Apple is monetizing AI through services and advertising with far lower infrastructure intensity, highlighting the different risk‑reward profiles facing big‑cap tech investors.

In sum, Meta Platforms AI infrastructure is rapidly becoming one of the most ambitious capital projects in Silicon Valley, pairing Arm’s new AGI CPU with massive GPU clusters, custom accelerators and multi‑billion‑dollar cloud capacity deals. For U.S. investors, the stock now represents a high‑beta wager that this hardware foundation will translate into faster AI product innovation and sustained ad pricing power. The next few quarters of CapEx deployment and Llama adoption will be critical in proving whether this bold infrastructure gamble deserves a larger place in long‑term growth portfolios.