Is the aggressive Meta Platforms AI Strategy building a future superintelligence moat or setting investors up for an expensive disappointment?

Is Meta’s AI bet changing the stock story?

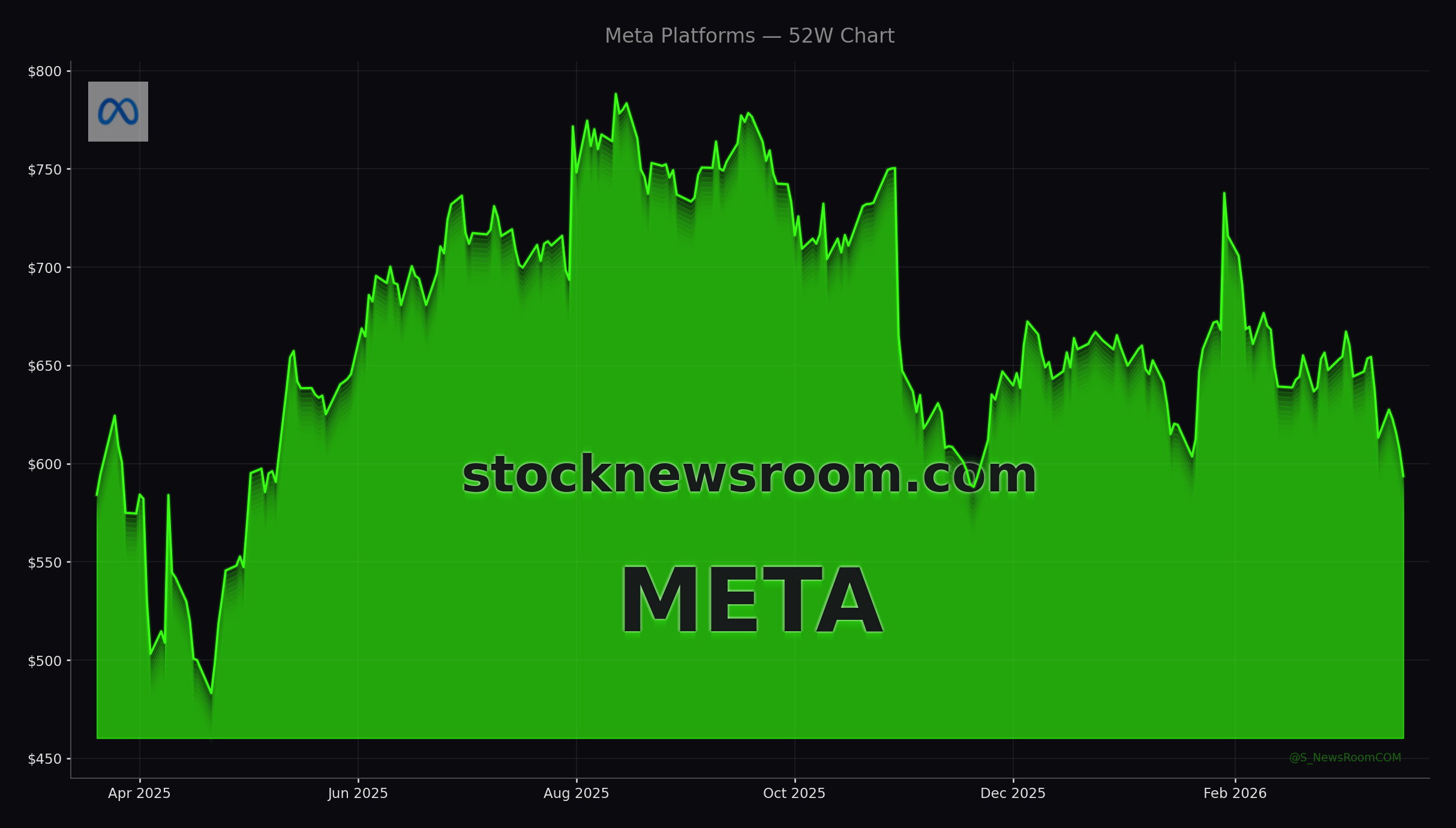

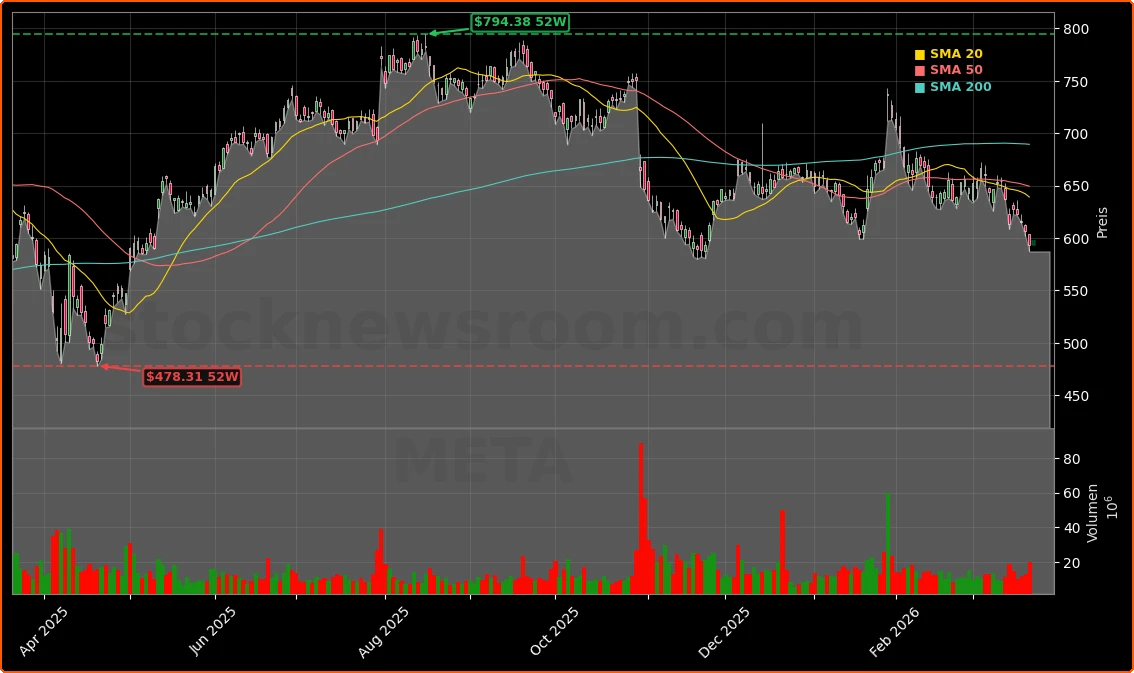

Meta Platforms, Inc. sits near the top of the S&P 500 and NASDAQ in market cap, yet it trades around 20–26 times forward earnings, below many other mega‑cap AI leaders. After a recent pullback to $593.66, the stock is off its highs even as analysts project earnings growth of roughly 20%+ annually over the next three years. The core of the Meta Platforms AI Strategy is simple but expensive: build one of the largest AI infrastructure footprints in the world, then use it to deepen engagement across Facebook, Instagram, WhatsApp and Threads while automating and enhancing its core digital ad business.

Meta’s management has guided to staggering capital expenditures, with 2026 capex expected in the $115 billion to $135 billion range as it builds AI data centers, custom accelerators and networking capacity. Combined with Alphabet’s plans, the two companies are on track to deploy more than $300 billion in capex in 2026 alone, making them central players in the global AI build‑out alongside infrastructure beneficiaries like NVIDIA and Arista Networks.

How is Meta using AI in ads and engagement?

The most visible layer of the Meta Platforms AI Strategy is in the news feeds and ad units that drive revenue today. Meta reported 3.58 billion daily active users across its family of apps in Q4 2025. AI recommendation systems now rank posts, Reels and ads to maximize relevance, with CFO Susan Li highlighting a 7% lift in views of organic feed and video posts on Facebook in Q4 and the largest quarterly revenue impact from Facebook product launches in two years. The average price per ad rose 6% year over year, helped by better targeting and higher advertiser demand.

For advertisers, Meta is rolling out AI‑powered tools that move beyond simple campaign optimization. The company is testing a Meta AI business assistant designed to take a budget and objective and then automate creative generation, audience selection and bid strategy – effectively turning AI into a full‑funnel campaign manager. This approach mirrors, and competes directly with, the automation efforts of Alphabet’s Performance Max in Google Ads, reinforcing that Meta’s AI roadmap is primarily commercial rather than purely research‑driven.

What makes the Meta Platforms AI Strategy unique?

Where the Meta Platforms AI Strategy diverges from rivals is in its long‑term vision for personal superintelligence. CEO Mark Zuckerberg has laid out a plan to build AI assistants that are tailored to individuals, understand their preferences, interact with the physical and digital environment, and help users pursue goals across work, social life and entertainment. Unlike generalized chatbots, this is meant to be persistent, personal and deeply integrated into Meta’s apps and devices.

Smart glasses are a major pillar of that plan. Meta already dominates the nascent smart‑glasses market, with estimates suggesting it holds more than 70% share. Management sees a future where AI‑infused glasses act as always‑on, voice‑driven companions, overlaying information and capturing data to continuously train models. This is also where Meta’s open‑source Llama models and projects like its Diplomacy‑playing AI Cicero fit in: by seeding an ecosystem of AI tools and research, Meta aims to make its platforms indispensable to both users and developers, in contrast to the more closed approaches from Apple and others.

Can profits keep up with $100B+ capex?

The main bear case centers on whether this spending spree will dilute returns. On Schwab Network, analyst David Trainer recently argued that Oracle (ORCL) is the “first canary in the coal mine” for an AI capex bubble and flagged Meta as another mega‑cap whose profit trajectory could be weighed down by infrastructure outlays and rich AI talent costs. Meta is reportedly offering AI engineers compensation packages in the hundreds of millions of dollars over multiple years, underscoring how intensely it is competing with Tesla, NVIDIA and cloud leaders for scarce expertise.

Yet Meta enters this cycle from a position of strength. The company remains highly profitable with a robust balance sheet and a core ad franchise that continues to grow. Some on Wall Street view the current valuation as overly punitive given Meta’s dual role as both AI user and AI infrastructure buyer. Several research desks, including major firms like Goldman Sachs and Morgan Stanley, have highlighted Meta as a relative bargain among the so‑called “Magnificent Seven,” and commentary from multiple banks points to upside toward a consensus price target in the $800s, implying substantial appreciation potential from current levels.

How does Meta compare to other AI leaders?

For U.S. investors seeking AI exposure, the key decision is how to balance pure infrastructure plays with application‑layer platforms. Meta’s capex ramp directly benefits chipmakers, foundries and networking vendors, from NVIDIA to ARM and Arista Networks, but Meta itself is a consumer‑facing AI platform with an adtech backbone. Unlike cloud‑heavy hyperscalers, Meta is not renting out vast amounts of compute; instead, it is deploying it internally to enhance engagement, advertising efficiency and next‑generation hardware like VR headsets and smart glasses.

Recent coverage from The Motley Fool has repeatedly flagged Meta as one of five “Magnificent Seven” stocks that still look attractive after the recent sell‑off, emphasizing that Meta is among the cohort’s fastest growers while trading at one of the lowest earnings multiples. Billionaire investor Bill Ackman has made Meta an 11% position in Pershing Square, framing it as the second‑largest adtech platform globally and a clear winner in AI‑driven ad optimization. That kind of concentrated hedge fund conviction stands in contrast to the more cautious tone from skeptics focused on capex and regulatory risk.

Related Coverage

For a deeper dive into how this spending wave fits into Meta’s recent volatility, investors can read “Meta Platforms AI Strategy: -1.9% Shock and Metaverse Pivot”, which explores whether the company’s AI and metaverse focus marks a visionary shift or a risky reset. To understand how cyclicality in adjacent hardware markets might influence sentiment around AI infrastructure spending, see “SanDisk Earnings -8.1% Plunge After Blockbuster AI Quarter”, which looks at whether a recent earnings drop is a blip or an early warning sign for the broader AI supply chain.

Meta is an essential platform for businesses seeking to maximize their return on ad spend, and its AI innovation is only deepening that advantage.— Bill Ackman, CEO, Pershing Square Capital Management

The Meta Platforms AI Strategy is reshaping the company from a social‑media ad giant into a vertically integrated AI and hardware ecosystem, with capex and superintelligence ambitions at its core. For U.S. investors, the stock offers leveraged exposure to AI applications and infrastructure, but with greater sensitivity to advertising cycles and execution risk than pure‑play chip names. The next few quarters of user engagement, ad pricing and capex efficiency will be critical in determining whether Meta’s AI gamble simply compresses margins or unlocks the kind of durable growth that long‑term portfolios seek.