Is Meta Platforms Muse Spark the AI catalyst that can turn heavy capex into a fresh leg higher for the stock?

How is Meta’s AI push moving the stock?

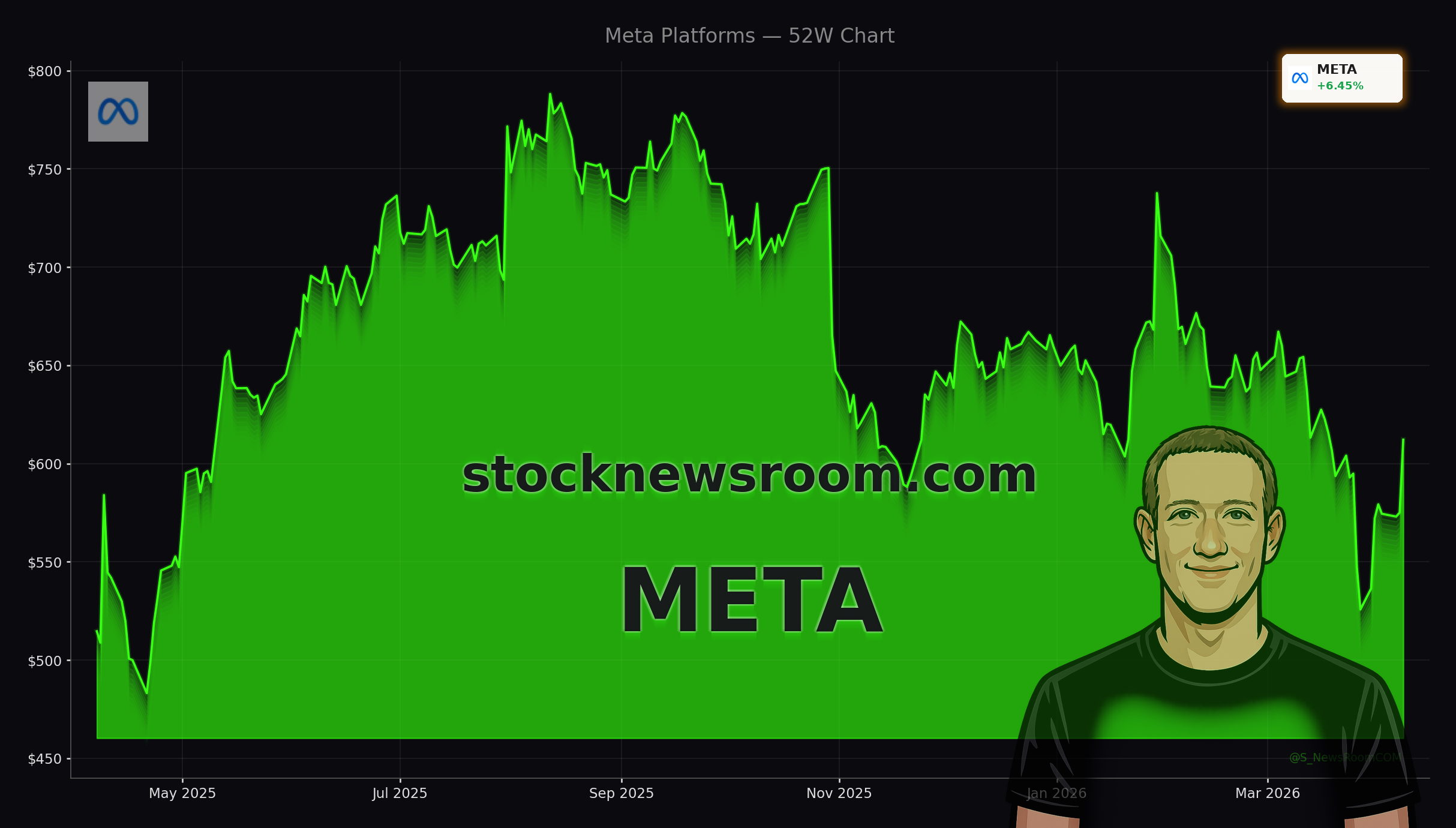

Meta shares climbed to $610.44 on Wednesday, a gain of 6.15% from the prior close of $596.70, as investors rotated back into large‑cap tech following a geopolitical ceasefire that eased oil and inflation worries. The rally puts Meta among the best performers in the Mag 7 group on the day, even though the stock remains roughly 27% below its 52‑week high, leaving room for recovery if sentiment around its AI strategy continues to improve.

The latest leg higher follows Meta’s unveiling of its new AI model, Meta Platforms Muse Spark, and a broader shift in focus from metaverse ambitions toward monetizable AI. Hedge funds have treated recent weakness as an entry point: roughly 90% of covering analysts now rate the stock a Buy, with a consensus price target around $850 implying close to 50% upside from current levels, according to recent Wall Street research. That valuation case rests heavily on Meta’s ability to turn AI capex into operating leverage and new revenue streams.

At the index level, Meta’s rally helped power the NASDAQ higher, with the tech‑heavy benchmark now trading less than 3% below its all‑time highs. Large‑cap growth, once pressured by rising yields during the conflict, is again leading as investors favor scalable AI platforms such as Meta, NVIDIA, Alphabet and Apple.

What exactly is Meta Platforms Muse Spark?

Meta Platforms Muse Spark is the first model in a new Muse series built by Meta Superintelligence Labs, the AI unit led by Scale AI founder Alexandr Wang after Meta committed roughly $14.3 billion to a strategic partnership with Scale. Internally codenamed “Avocado,” Muse Spark is designed as a smaller, faster model that still delivers competitive performance in multimodal perception, reasoning and health‑related tasks.

Meta rebuilt its AI stack over the past nine months to support this launch, aiming to match the capabilities of prior midsize Llama variants with an order of magnitude less compute. Unlike the open‑source Llama family, this first Muse Spark model is proprietary. Meta has indicated it may open‑source future versions once it has established a performance and monetization baseline.

The model now powers the company’s Meta AI assistant across a standalone app, web interface and soon directly inside Facebook, Instagram, WhatsApp and Messenger. It is also slated to run on Ray‑Ban Meta smart glasses and eventually on Vibes AI video features that currently depend on third‑party models. For users, Muse Spark enables different modes—quick responses, deeper analysis for legal or nutritional questions, and a “Contemplating” mode that orchestrates a squad of agents to compete with the extreme‑reasoning modes of frontier models like Gemini Deep Think and GPT Pro.

How does Muse Spark fit into Meta’s AI economics?

For investors, the key question is how Meta Platforms Muse Spark links to cash flows. Meta’s ad business remains the core profit engine: 2025 revenue reached about $201 billion, up more than 22% year over year, with Q4 2025 ad revenue of $58.14 billion growing 24%. Ad impressions rose 18% while price per ad climbed 6%, a combination management attributes to AI‑driven targeting, better Reels monetization, and increasing use of AI to optimize campaigns.

Muse Spark sits atop a rapidly expanding AI infrastructure stack. Meta expects 2026 capital expenditures of $115–$135 billion, almost double last year, largely for data centers, custom chips and networking. It is boosting investment in its El Paso, Texas AI data center to $10 billion, targeting 1‑gigawatt capacity by 2028, and has also partnered with Corning on an up‑to‑$6 billion optical cable expansion in North Carolina to feed next‑generation AI data centers. Management still guides for higher operating income in 2026 versus 2025 despite this spending ramp, assuming AI‑enabled productivity and ad monetization offset Reality Labs losses, which totaled roughly $19.2 billion in 2025.

On the revenue side, Meta is experimenting with a new stream by offering API access to Muse Spark. The model is in private preview with select developers, with plans for paid access at scale later. That approach mirrors strategies from OpenAI and Anthropic, giving Meta a potential foothold in the broader model‑as‑a‑service market rather than relying solely on advertising uplift.

Where does Meta stand versus AI rivals?

Despite the strategic pivot, Meta is still playing catch‑up in headline AI mindshare. OpenAI and Anthropic together carry valuations north of $1 trillion, and Google’s Gemini stack has gained traction with consumers and enterprises. Meta’s prior open‑source launches failed to fully capture developers’ attention, prompting Mark Zuckerberg to concentrate resources in Meta Superintelligence Labs and tilt the company away from a pure metaverse narrative.

On Wall Street, some strategists argue that, relative to pure‑play AI server vendors like Super Micro Computer, Meta offers a smoother, more liquid way to gain AI exposure—less cyclical hardware risk, more embedded AI across a massive user base. Others remain skeptical about Mag 7 outperformance from here, warning that capex intensity and regulatory overhangs could cap multiples even if products like Meta Platforms Muse Spark perform well. In Europe, tougher rules on personalized ads and youth‑safety litigation in the U.S. are key watchpoints.

Still, the stock’s current valuation—around 19x forward earnings by some estimates—looks modest compared with its ad growth and AI optionality, leading banks such as Morgan Stanley and Goldman Sachs to keep Overweight or Buy‑equivalent ratings in place. Q1 2026 earnings on April 29, with revenue guidance of $53.5–$56.5 billion, will be the next checkpoint for whether Muse Spark and the broader AI offensive are translating into sustained growth.

Related Coverage

Investors focused on legal and regulatory risk around Meta’s AI strategy should read Meta AI Regulation Warning: Court Losses And AI Shock, which examines how mounting lawsuits and aggressive AI spending could weigh on long‑term returns. For a broader sector perspective on AI infrastructure, Taiwan Semiconductor AI Expansion Fuels +6.1% Rally looks at how TSMC’s capacity build‑out is powering another key pillar of the global AI supply chain and what that might mean for hyperscalers like Meta and Tesla as they scale compute demand.

In the end, Meta Platforms Muse Spark is less about one model than about proving that Meta’s massive AI capex can deliver faster products, stronger ad economics and new revenue streams. For U.S. portfolios seeking AI exposure without betting solely on hardware or start‑ups, Meta remains a central, liquid vehicle. The upcoming earnings report and the broader rollout of Muse Spark across apps and devices will show whether this AI offensive can sustain the latest rally and keep Meta among Wall Street’s core AI winners.