Are Meta Social Media Lawsuits turning a routine legal risk into a structural threat that could permanently re-rate the stock?

Why are Meta shares sliding again?

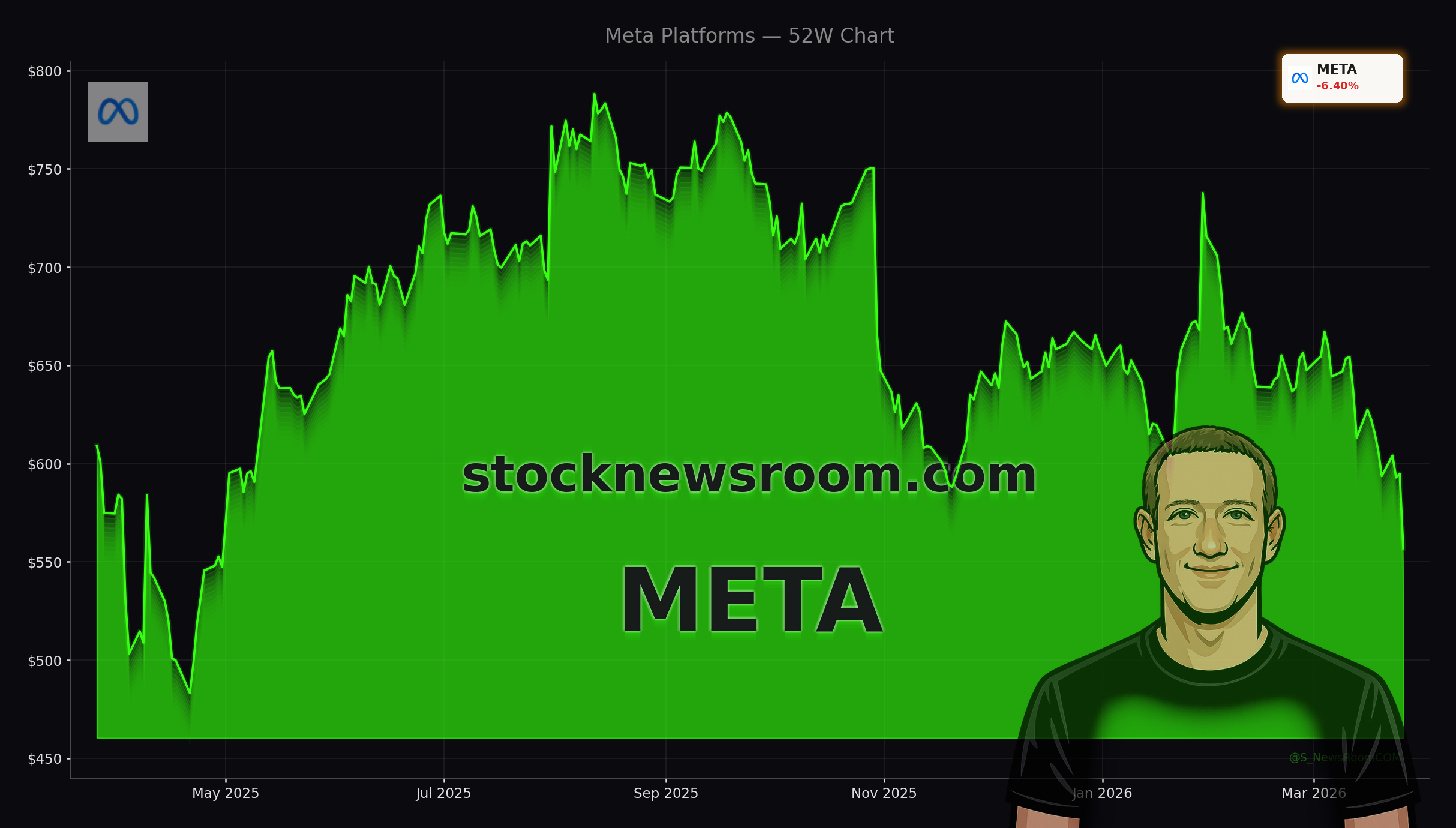

Meta stock is down nearly 29% from its all-time closing high of $790 in August 2025 and roughly 15% year-to-date, making it one of the weaker mega-cap tech names in Q1 2026. Thursday’s drop follows a pair of courtroom setbacks that sharpen the focus on the Meta Social Media Lawsuits and the company’s core engagement-based advertising model. The latest move puts the stock only about 1% above the April 2025 support area around $549, which technical traders are watching as a potential line in the sand.

Beyond legal headlines, traders also point to broader risk-off sentiment on the NASDAQ, rising energy prices and investor unease about higher AI capital expenditures. Some portfolio managers have recently rotated out of Meta into other growth stories, echoing similar shifts seen when high-multiple favorites like NVIDIA or Tesla became crowded trades. With Meta now trading well below its 52-week high but still above last year’s lows, the stock is caught between those buying the dip and those seeing a longer de-rating ahead.

What do the Meta Social Media Lawsuits change?

The immediate catalyst is a landmark California jury verdict that found Meta and Alphabet’s YouTube negligent for designing social platforms that were addictive and harmful to children and teens, and for failing to warn about those risks. Jurors awarded a total of $6 million to a 20-year-old plaintiff, split between compensatory and punitive damages, assigning 70% of the responsibility to Meta. Crucially for investors, the case turned on product design and recommendation mechanics rather than user-generated content, sidestepping the broad protections of Section 230 that tech firms have relied on for decades.

Separately, a New Mexico jury ruled that Meta failed to adequately protect young people from solicitation, explicit content and trafficking-related dangers on its platforms. Together, these decisions are viewed by legal analysts as a watershed moment that could open the door to thousands of similar Meta Social Media Lawsuits across the U.S. Even if most cases settle or are dismissed, the prospect of years of litigation, discovery and potential product redesign raises the regulatory and financial overhang on Meta, Google parent Alphabet and, by extension, other social platforms like TikTok and Snap.

How big is the litigation and regulatory risk?

So far, the dollar amounts involved — single-digit millions per case — are trivial for a company generating tens of billions in annual free cash flow with an operating margin near 41%. The market concern is not today’s $6 million bill, but the precedent. If more juries find that engagement-boosting features are intentionally addictive, Meta and peers could face a future similar to tobacco or opioid settlements, where cumulative payouts and mandated product changes run into the tens of billions.

Regulators in the U.S. and Europe are already tightening rules around data privacy, youth protections and algorithmic transparency. The Meta Social Media Lawsuits give lawmakers fresh ammunition to push for age verification, default time limits, stricter parental controls and limits on targeted ads to minors. Any sustained hit to usage time or ad targeting efficiency would directly affect Meta’s revenue and margin profile, undercutting part of the bull case that still sees the stock as undervalued relative to its growth outlook.

What else is pressuring sentiment on Meta?

At the same time the lawsuits flare up, Meta is restructuring again. Management confirmed that several hundred employees — roughly into the low four digits when including international teams — will be cut across sales, recruiting, global operations and the Reality Labs hardware division. Some roles may be relocated, but the net effect is another wave of job losses on top of the “year of efficiency” cuts in 2023, signaling continued cost discipline but also raising questions about execution in virtual reality and metaverse hardware.

Investors are also digesting a new executive incentive program that ties substantial stock awards to an extraordinarily ambitious long-term valuation target. Meta has floated internal benchmarks that imply a potential several-hundred-percent share price increase by the early 2030s, effectively betting that its AI-driven ad engine, messaging and metaverse initiatives can support a multi-trillion-dollar market capitalization. Skeptics argue that unlike Apple selling premium hardware or cloud giants monetizing AI models directly, Meta still relies heavily on ad impressions and user attention — precisely the areas under scrutiny in court.

How do Wall Street analysts view the stock now?

Despite the drawdown, many major brokerages remain constructive. Trading platforms tracking consensus show that firms such as Goldman Sachs, Morgan Stanley, and RBC Capital Markets still rate Meta as a “Buy” or “Overweight,” with average 12‑month price targets implying upside of roughly 50% from current levels. Some houses, including Citigroup and JPMorgan, emphasize Meta’s strong balance sheet, robust ad demand and AI recommendation engine as key reasons the stock looks undervalued versus other mega-cap growth names.

More cautious voices, as highlighted in several recent downgrades, focus on rising AI capex, potential margin compression and the expanding litigation cloud. Quant-focused shops note that Meta’s factor profile has shifted from high-momentum to value-plus-quality, similar to the evolution earlier seen in NVIDIA when AI euphoria paused. For diversified U.S. investors, the decision now is whether to treat Meta as a structurally challenged ad platform or as a temporarily out-of-favor cash machine that can absorb litigation costs and still compound earnings.

Related Coverage

For a deeper dive into how Meta’s aggressive AI spending and sky-high long-term valuation goals intersect with today’s legal and regulatory risks, see Meta AI Strategy $9T Boom Target and -1.9% Stock Warning, which dissects whether the company’s ambitious pay packages and growth targets are realistic. To understand the broader AI hardware backdrop that indirectly affects Meta’s data center and infrastructure spending, read Micron AI Memory Cycle -3.4%: Record Boom Meets Crash Fears, examining whether today’s chip boom can sustain or risks a classic downcycle.

Meta remains a dominant force in global social networking and digital advertising, but the growing wave of Meta Social Media Lawsuits adds a new layer of uncertainty that markets can no longer ignore. For long-term U.S. investors, the stock now sits at the crossroads of powerful AI-driven earnings potential and a rising litigation and regulatory bill. The next quarters — including any appeals, new verdicts and product changes — will show whether Meta can turn its legal headwinds into a manageable cost of doing business or whether this marks a structural shift in how social media is allowed to operate.