Is Micron AI Infrastructure still a long-term winner after today’s sharp sell-off, or is the AI hardware trade finally overheating?

Micron Technology and the AI infrastructure rotation on Wall Street

Micron Technology sits at the epicenter of a monumental capital rotation in 2026. Big institutional investors have been reducing exposure to high‑multiple Software‑as‑a‑Service names and reallocating into the physical infrastructure required to run large AI models: GPUs, CPUs, networking, and—crucially—memory and storage. In that context, Micron AI Infrastructure has emerged as a core beneficiary alongside competitors such as SK Hynix, Samsung and U.S. peers in NAND and DRAM.

While the SaaS complex has seen double‑digit percentage drawdowns, memory‑centric hardware names have attracted what some managers describe as “non‑stop money.” Capital is flowing toward the companies providing the bandwidth and capacity needed to train and serve large language models, recommendation engines, and other AI workloads. Micron’s focus on high‑bandwidth memory (HBM) for accelerators and low‑power DRAM for data center CPUs positions the company as a structural winner in this shift.

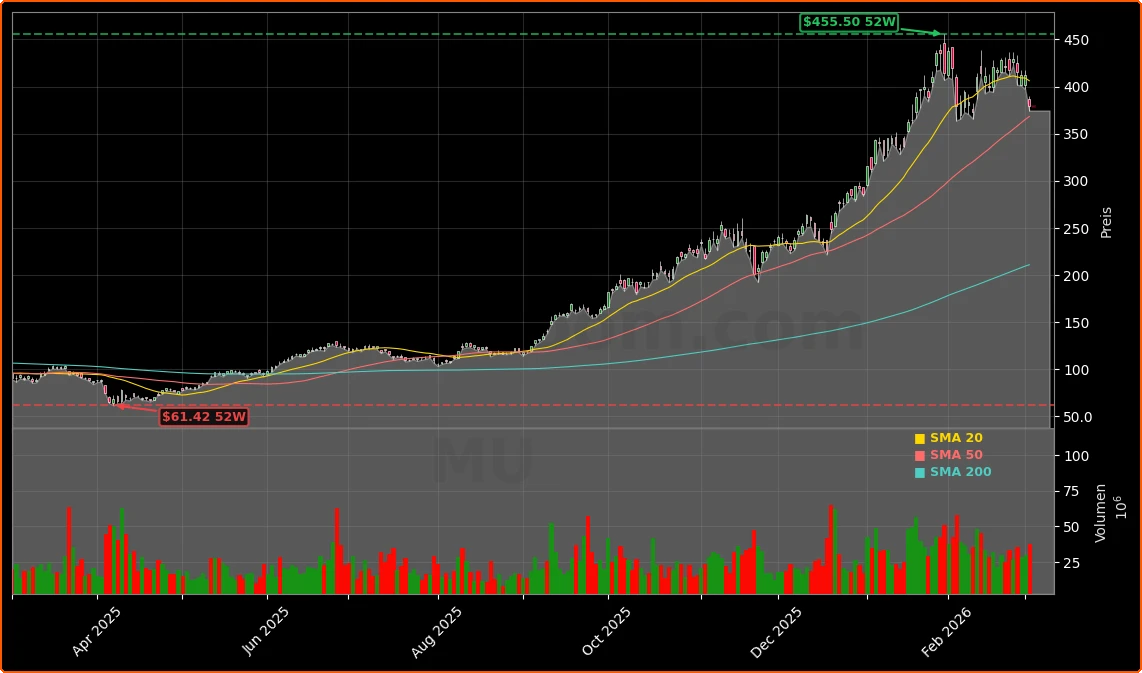

However, that success has driven Micron’s share price far ahead of its long‑term trend lines. With the stock recently trading more than 100% above its 200‑day moving average and now dropping nearly 8% in a single session to about $379.68, the risk of a deeper technical correction has risen sharply. For U.S. investors, the question is no longer whether Micron AI Infrastructure is strategically important—it clearly is—but whether the current entry point compensates for geopolitical, cyclical, and valuation risks.

Micron AI Infrastructure: Is the new 256GB LPDRAM module a game changer?

On the fundamental side, Micron just delivered a significant product milestone for Micron AI Infrastructure: it has begun shipping customer samples of its 256GB SOCAMM2 LPDRAM module for AI and high‑performance computing servers. This is currently the industry’s highest‑capacity LPDRAM module, enabled by the first monolithic 32Gb LPDDR5X design. For hyperscale data centers running AI inference and training, this product directly addresses three constraints: memory capacity per socket, power consumption, and physical footprint.

Traditional RDIMMs in CPU servers consume substantial power, which becomes a bottleneck when operators are already running energy‑intensive GPU clusters from partners like NVIDIA. Micron’s new 256GB SOCAMM2 module is designed to use roughly one‑third of the power of equivalent RDIMM solutions while delivering higher capacity in a smaller form factor. That combination allows data centers to support larger context windows and model sizes per CPU node, or to increase server density within existing power budgets.

The company already offers best‑in‑class HBM solutions for accelerators used in AI training, and the expansion into ultra‑high‑capacity, low‑power LPDRAM for CPUs broadens the Micron AI Infrastructure stack. If future AI architectures lean more heavily on CPU‑centric inference or mixed CPU‑GPU topologies, this LPDRAM line could become a major incremental growth driver. The early sampling phase also tends to be a leading indicator: once key hyperscalers qualify the product, volumes can ramp rapidly across multiple generations of server designs.

Micron Technology: How are analysts reacting to the surge and pullback?

Wall Street’s fundamental view of Micron remains constructive, even as the stock corrects. A notable move came from Goldman Sachs, which recently raised its price target on Micron from $235 to $360 per share while maintaining a Neutral rating. The target lift acknowledges Micron’s stronger earnings power in an AI‑driven upcycle and the strategic positioning of Micron AI Infrastructure in data centers worldwide.

Goldman’s new target sits slightly below the current market price after today’s sell‑off, effectively signaling that the stock has moved into the upper band of what the bank considers fair value in the near term. Other institutions have been voting with their wallets: Strive Asset Management, for example, initiated a position worth roughly $3.35 million, reflecting ongoing institutional accumulation despite elevated volatility. Across Wall Street, Micron has garnered a Strong Buy designation from several ranking systems that focus on earnings revisions and estimate momentum, suggesting that profit expectations continue to trend higher.

At the same time, the sharper day‑to‑day moves reflect growing disagreement about the appropriate multiple for a cyclical memory business in an AI super‑cycle. Some short sellers are expressing their skepticism through vehicles like bear‑oriented Micron ETFs, while options activity has picked up around downside protection. Investors need to reconcile bullish long‑term estimates with the reality that Micron’s earnings remain exposed to memory pricing cycles and macro shocks.

Micron Technology: Geopolitics, energy prices and the memory stock sell‑off

The immediate catalyst for Micron’s latest leg down is not company‑specific. Heightened fears around the U.S. and Israel’s war with Iran, combined with a spike in oil prices and shipping risk through the Strait of Hormuz, have rattled AI‑linked technology stocks across the board. Higher energy costs and potential disruptions to global supply chains raise the prospect of persistent inflation, which in turn could force interest rates to stay higher for longer. Growth‑dependent and capital‑intensive sectors like semiconductors tend to de‑rate under such scenarios.

Memory names have been hit particularly hard. Large overnight declines in South Korean giants SK Hynix and Samsung spilled over into U.S. trading, triggering a broad sell‑off in the memory ecosystem including Micron, Seagate, Western Digital and SanDisk. Investors are also reassessing the cost structure of Asian fabs, where liquefied natural gas prices and electricity costs are key inputs. While Micron’s manufacturing footprint differs, sector‑wide de‑risking rarely distinguishes between individual operators in the heat of a macro‑driven downdraft.

This environment tests the durability of the Micron AI Infrastructure thesis. On one side is secular demand for more memory per AI accelerator and CPU socket; on the other is macro uncertainty that can alter discount rates, lower valuations, and delay some capex decisions at hyperscalers. For U.S. portfolios concentrated in high‑beta AI plays, the memory segment’s recent weakness underscores the importance of position sizing and risk management around geopolitical headlines.

Micron Technology vs. AI peers: How does the risk/reward stack up?

In the AI value chain, Micron plays a very different role than compute‑centric leaders like NVIDIA. GPUs and specialized accelerators capture much of the narrative and margin, but they cannot deliver value without sufficient high‑bandwidth and low‑latency memory. That makes Micron AI Infrastructure a foundational layer rather than the star of the show. For investors, this translates into a different risk and return profile.

Compared with GPU vendors, Micron’s business remains more heavily exposed to commodity‑like DRAM and NAND pricing. This cyclicality has historically produced boom‑and‑bust earnings patterns, even when the long‑term capacity trend points upward. By contrast, hyperscale operators and platform companies like Apple or Tesla have more diversified revenue streams and brand‑driven ecosystems, which can cushion volatility from any single hardware cycle. On the other hand, Micron’s valuation multiple has typically been lower than those of fabless GPU designers or megacap platform stocks, leaving more room for earnings surprises to drive upside in an upcycle.

Within memory and storage specifically, Micron competes with a mix of U.S. and Asian players. SanDisk—now a key standalone name after its separation from Western Digital—has surged more than 160% year‑to‑date, significantly outpacing Micron’s gains before today’s correction. That outperformance reflects market enthusiasm for NAND and storage solutions linked to AI data lakes and enterprise storage, but it also raises questions about relative value. For investors seeking exposure to the memory leg of the AI build‑out, Micron’s current pullback may narrow the valuation gap versus some peers while offering more diversified exposure across DRAM, HBM, and LPDRAM products.

Micron Technology: Technical setup and correction risk for U.S. investors

From a technical perspective, Micron’s chart is flashing both opportunity and caution. The stock remains dramatically extended versus its 200‑day moving average—recently over 125% above that long‑term trend line—despite the latest drop. Historically, such extreme deviations in cyclical semiconductor names have been followed by meaningful consolidations or corrections, especially when combined with rising volatility indicators such as a VIX reading in the mid‑20s or higher.

Shorter‑term, Micron is testing its 50‑day moving average, a level that has consistently acted as support throughout the current rally. A decisive close below this line that is not quickly bought back could signal the start of a more robust unwind, as trend‑following strategies and leveraged long positions are forced to de‑risk. The appearance of bear‑oriented Micron products on institutional scanners, as well as increased put buying, points to a growing constituency betting on further downside in the near term.

For active U.S. traders, this environment favors tactical flexibility. Some may look to fade sharp intraday bounces toward prior lows to establish short‑term bearish positions, while longer‑term investors might prefer to scale in gradually on weakness rather than trying to pick an exact bottom. The key is to separate the structural Micron AI Infrastructure story—which remains compelling—from the shorter‑term technical and macro forces that can drive 20–30% swings even in high‑quality names.

Micron AI Infrastructure: What’s priced in and what isn’t?

Despite the recent volatility, the Micron AI Infrastructure narrative is still in the early innings. AI models are becoming larger and more memory‑intensive, inference workloads are moving into production across industries, and data centers are under pressure to reduce energy consumption per workload. Micron’s HBM offerings for accelerators and its new 256GB SOCAMM2 LPDRAM module for CPUs directly target these trends, and the company has been working closely with ecosystem partners such as NVIDIA to align product roadmaps with forthcoming AI platforms.

The market has already priced in a significant portion of this upside, as reflected in Micron’s rapid share‑price appreciation, premium to historical valuation ranges, and optimistic earnings revisions. What may not be fully discounted are the potential speed bumps: geopolitical shocks that impact energy and supply chains, a possible pause or delay in hyperscaler capex if macro conditions worsen, and the ever‑present risk of oversupply in commodity memory if the industry overbuilds capacity. On the positive side, what could still surprise to the upside is the breadth of AI adoption beyond big tech—into industrial, automotive, and edge computing applications—where Micron’s portfolio could capture incremental demand.

For diversified American investors, the decision is less about whether Micron will remain central to AI infrastructure—it likely will—and more about how to size that exposure relative to higher‑margin compute names, diversified tech platforms, and non‑tech assets that can hedge macro and rate risk. In that portfolio context, Micron AI Infrastructure can serve as a targeted, high‑beta play on the memory and bandwidth constraints of AI, ideally balanced with steadier cash‑flow generators elsewhere in the S&P 500 and Nasdaq.

Conclusion

In summary, Micron offers a powerful combination of strategic relevance, cutting‑edge products, and strong institutional support. Yet those same strengths have driven the stock into technically stretched territory just as macro risks are rising. Investors who believe in the long‑term AI build‑out but respect the cyclicality of memory may find the best risk/reward in patiently accumulating on deeper pullbacks rather than chasing post‑news spikes. Micron AI Infrastructure is likely to remain a cornerstone of the AI hardware stack for years to come—but the path of the share price could be considerably bumpier than the smooth exponential curves often implied by AI hype.

Further Reading

- Micron Technology, Inc. (MU) Stock Price, News, Quote & History (Yahoo Finance)

- Micron Ships 256GB SOCAMM2 Customer Samples for AI and HPC Servers (HPCwire)

- Micron 256GB AI server memory uses one-third the power of RDIMMs (Stock Titan)

- Investors Heavily Search Micron Technology, Inc. (MU): Here is What You Need to Know (Yahoo Finance Singapore)