Is the Micron AI Memory Cycle a once-in-a-decade profit boom—or the top of a classic chip cycle about to crack?

Why is Micron falling after record results?

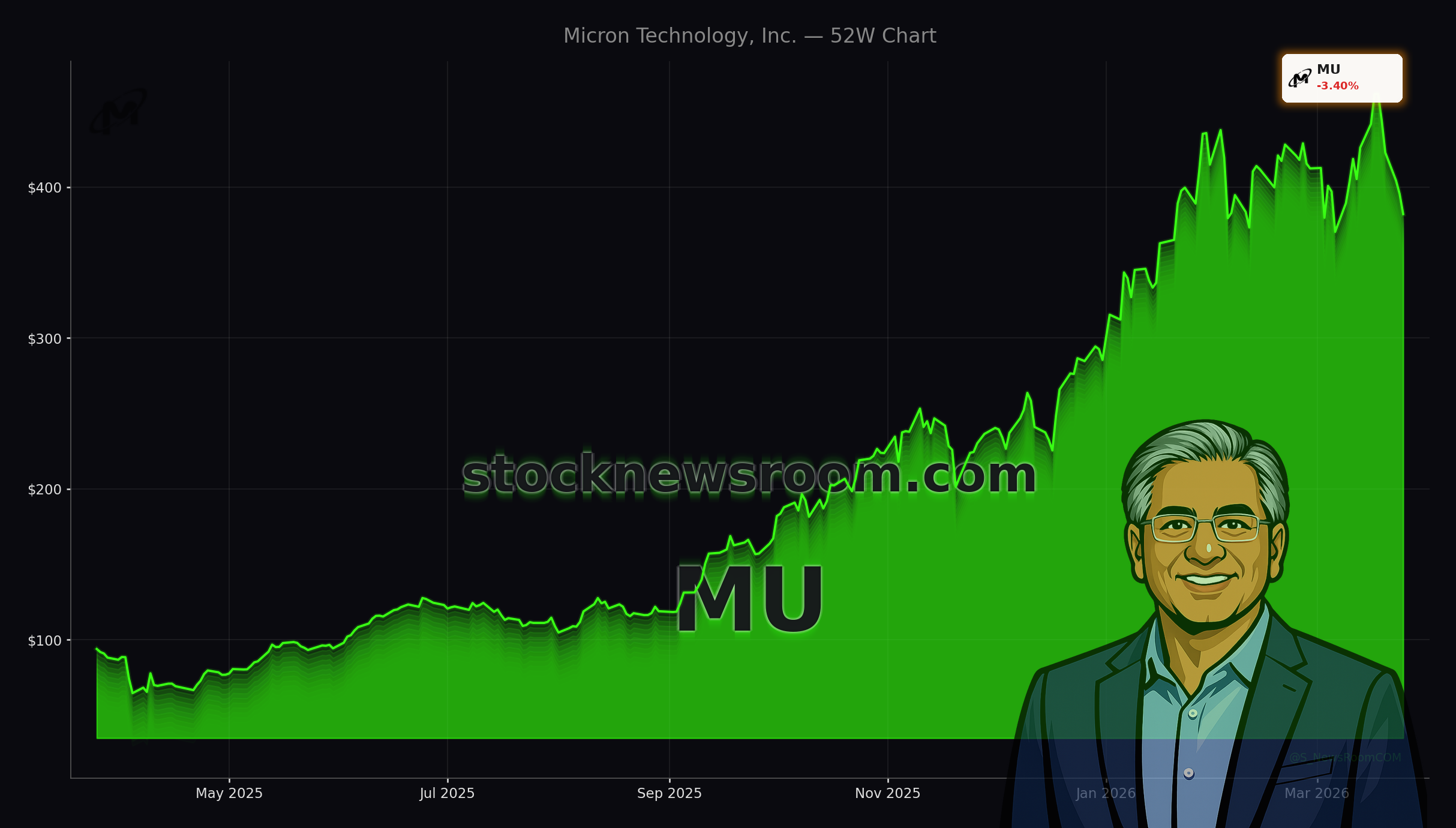

Micron Technology, Inc. stunned the market with fiscal Q2 2026 revenue of about $23.9 billion, up 196% year over year, and adjusted EPS of $12.20. Gross margin surged to roughly 74%, nearly doubling from a year earlier, as prices for DRAM and high‑bandwidth memory (HBM) soared. Management guided for an even stronger fiscal Q3, targeting around $33.5 billion in sales and gross margins approaching the low‑80% range.

Despite those numbers, the stock dropped sharply after earnings and remains volatile. At about $382.09 per share (pre‑market indications slightly lower), Micron trades well below recent highs, even after a roughly 300% gain over the last twelve months. The immediate trigger for the pullback is not the Micron AI Memory Cycle itself, but mounting concerns that extraordinary AI‑driven demand could normalize faster than bulls expect.

Part of the pressure is sector‑wide: memory and storage names such as SanDisk, Western Digital, Seagate, and Lam Research also sold off this week. That reflects profit‑taking after a massive run‑up, but also a reassessment of how sustainable current pricing power really is.

How fragile is the Micron AI Memory Cycle?

The heart of the Micron AI Memory Cycle is a historic squeeze in DRAM and especially HBM. Micron is one of three global DRAM giants, alongside Samsung and SK Hynix, and roughly 80% of its revenue still comes from DRAM. The rapid build‑out of AI data centers, powered by GPUs from players like NVIDIA, has pushed HBM demand “through the roof.” HBM is more complex to manufacture and can consume up to three times the wafer capacity of standard DRAM, leaving the broader DRAM market structurally undersupplied.

Analysts such as Wedbush estimate DRAM prices will be 130%–150% higher in the first half of the year versus last year’s Q4 levels. That pricing backdrop explains Micron’s near‑tripling of revenue and margin expansion from the mid‑30% range to the mid‑70s. Yet in classic semiconductor fashion, today’s tight supply and supernormal profits sow the seeds of tomorrow’s downturn as capacity ramps across the industry.

Adding a new twist, Google has unveiled an AI efficiency breakthrough dubbed “TurboQuant,” a quantization and compression technology that can shrink key‑value memory requirements for large language models by at least 6x without major accuracy loss. If widely adopted, such algorithms could significantly reduce DRAM and HBM needs per AI workload, potentially shortening the Micron AI Memory Cycle or flattening its peak.

What are analysts saying about Micron now?

Opinion on Micron is splitting more sharply after the recent slide. Bullish houses like Zacks Investment Research argue the 14% post‑earnings drop looks more like an opportunity than a warning, highlighting Micron’s record results and still‑low valuation versus AI peers. On some longer‑term estimates, the stock trades near 4–8 times forward earnings, far below premium AI names.

More cautious voices are also getting louder. A downgrade from Seeking Alpha’s coverage to “Hold” emphasized that AI‑driven DRAM demand may be fully priced in after the 300%+ rally and pointed to order‑book risks. One concern is potential overordering by hyperscalers and AI leaders: OpenAI alone is estimated to account for a large share of global DRAM orders, increasing the risk of future cancellations if demand or funding falls short.

While major Wall Street banks like Goldman Sachs, Morgan Stanley, and Citigroup have previously highlighted Micron as a key AI beneficiary, the latest moves show that sentiment is becoming more nuanced. Some analysts now stress that a low P/E in memory often signals not a bargain, but an earnings peak ahead of a downcycle.

How does Micron stack up against other AI plays?

Compared with IP and design‑centric players like Arm Holdings, Micron sits in a very different risk bucket. Arm recently jumped after unveiling plans to design its own AI chip, and it trades at a forward P/E multiple reportedly in the 70s. Micron’s single‑digit multiple underscores both its capital intensity and its exposure to commodity‑like pricing swings.

For U.S. investors balancing AI exposure, Micron offers direct leverage to infrastructure build‑out rather than to application‑layer growth. That makes it more cyclical than software names or platform giants such as Apple and cloud hyperscalers like Alphabet and Microsoft. At the same time, it is less exposed to consumer cyclicality than EV players like Tesla.

Equipment makers including Lam Research, Applied Materials, and KLA are also indirect beneficiaries. Micron has lifted its FY26 capex guidance to around $25 billion, helping drive demand for wafer‑fab tools and cleanroom expansions. A prolonged Micron AI Memory Cycle would likely reinforce that spending, while a sharp demand reset could hit both memory makers and their suppliers.

Related Coverage

For a deeper dive into how Micron’s latest quarter set the stage for the current sell‑off, including the impact of Google’s TurboQuant announcement, see Micron Earnings -3.5%: Record AI Boom Meets TurboQuant Shock. That piece explores whether record margins can coexist with structural AI memory compression. To understand the broader AI infrastructure backdrop driving Micron’s boom, including massive cloud capex plans, read Alphabet AI Strategy Boom: $185B Capex Shock for Cloud, which analyzes how Alphabet’s spending wave could sustain memory demand even as efficiency gains accelerate.

In the end, the Micron AI Memory Cycle captures both the promise and peril of betting on AI infrastructure. For aggressive investors, the recent pullback may be a chance to accumulate a pivotal chip name at a cyclical discount; for more cautious portfolios, the rising risk of algorithmic efficiency and classic overcapacity argues for position sizing discipline. The next few quarters of pricing data and AI workload trends will determine whether Micron’s current surge marks the start of a longer supercycle or simply the top of another powerful, but temporary, wave.