Can the Micron AI storage boom, with sold-out HBM and record margins, permanently break the brutal memory cycle?

Micron Technology: How Strong is the AI Business?

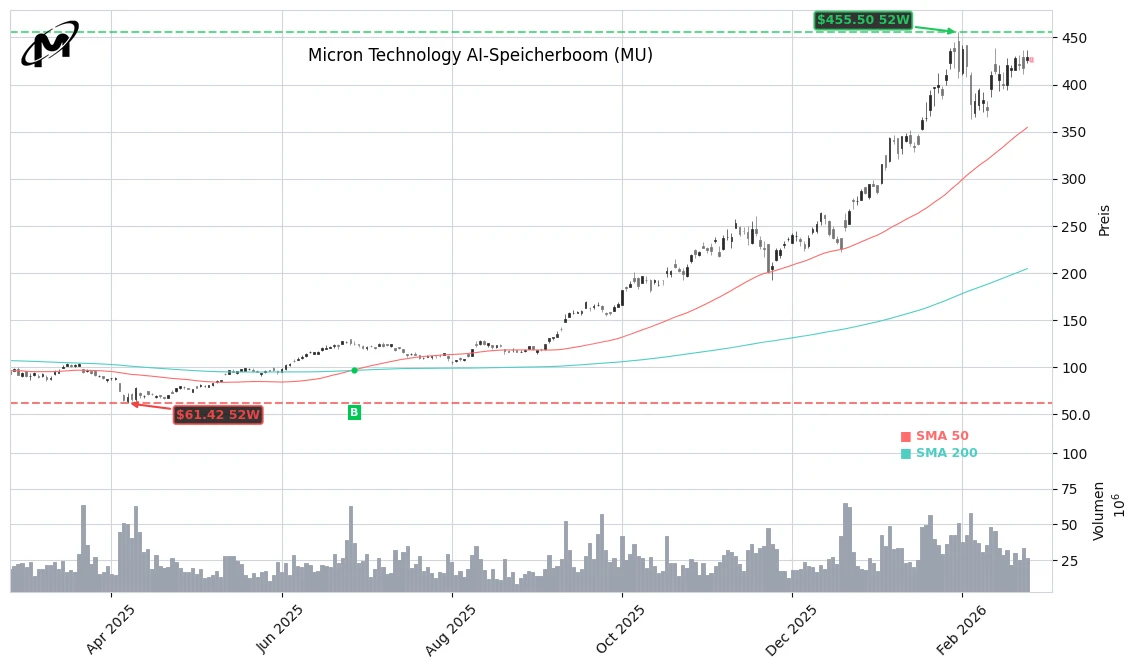

Micron Technology is among the hottest AI stocks as we enter 2026. After a gain of around 239% in 2025, the performance in 2026 is already about 50%. The closing price of $429.00 (previous day: $418.01, +2.63%) indicates that investors continue to bet on Micron AI storage. In after-hours trading, the shares dipped slightly to $423.47.

Fundamentally, Micron is benefiting from a massive demand boom in its core markets, DRAM and NAND. Approximately 80% of revenue comes from DRAM, with the remainder primarily from NAND flash. Both segments are now experiencing supply shortages again, after memory prices initially collapsed post-pandemic. The market for High-Bandwidth Memory (HBM), which is directly linked to GPUs like those from Nvidia to support AI models with extremely high data rates, is growing particularly dynamically.

Micron’s HBM capacity for this year is considered fully sold out. The company is negotiating multi-year supply contracts and significantly expanding its capacities to meet an expected annual demand increase of around 40% by 2028. The Micron AI storage is thus becoming a central component of the global AI infrastructure.

Micron Technology: Margin Jump through HBM and NAND

The AI boom is clearly reflected in the numbers. In the most recent quarter, revenue surged by 57%, while the gross margin jumped from 38.4% to 56%. Micron also generated a robust free cash flow of $3.9 billion—a significant turnaround from the deep memory crisis of recent years.

The reasons lie not only in the Micron AI storage segment HBM but also in the significant recovery of the NAND business. After flash memory was in such oversupply post-pandemic that it had to be sold below production costs, major manufacturers drastically cut their capacities. Now, the construction of massive AI data centers is driving demand for high-capacity SSDs—and thus prices—up again.

Additionally, memory manufacturers are focusing on HBM, which requires about three times the wafer capacity of standard DRAM and displaces other products due to larger chip areas. This tightening of supply supports prices across the entire DRAM market. For Micron AI storage, this means better mix effects, long-term contracts, and structurally higher margins, which at least mitigates the classic cyclical nature of the business.

Micron AI Storage: How is the Stock Valued?

Despite the price surge, Micron appears moderately valued based on earnings estimates. The stock is trading at a forward P/E ratio of around 12.5 for the fiscal year 2026 and about 9.5 for 2027 according to consensus. For many investors, Micron AI storage thus serves as a lever on the continued growth of AI infrastructure without having to pay Nvidia-like valuation premiums.

However, valuation models present a mixed picture: While some market participants derive a fair value of over $500 per share based on high growth assumptions, more conservative discounted cash flow analyses yield significantly lower fair value estimates of around $190 at the current $429. This range illustrates how much the assessment of the Micron AI storage business depends on the duration and intensity of the AI boom.

Meanwhile, Micron is advancing its U.S. manufacturing with an expansion estimated at around $50 billion at its Boise site. The new fabs are expected to deliver their first memory chips starting in 2027 and aim to meet the growing AI demand with domestic production—supported by funding from the CHIPS and Science Act. This not only strengthens the company’s technological position but also reduces geopolitical risks in the supply chain.

Micron Technology: What Does This Mean for Investors?

The recent strength of Micron’s stock coincides with a general rally in AI infrastructure stocks. Numerous chip producers and equipment suppliers are experiencing similar movements, while the market eagerly awaits Nvidia’s next numbers, which are considered a bellwether for the entire industry. Positive signals from the GPU market would further support the sales of Micron AI storage.

For investors, the central question remains whether the current record margins and extremely tight supply situation will establish themselves as a structural trend or revert to a classic memory cycle in the medium term. However, the combination of sold-out HBM, rising NAND prices, massive U.S. investments, and a historically moderate valuation makes Micron one of the most exciting beneficiaries of the AI infrastructure boom.

Bottom Line

Micron AI storage has become the centerpiece of global AI expansion. The stock benefits from full order books, high margins, and ambitious capacity expansions. For investors who believe in a long AI supercycle, Micron remains a promising opportunity to participate directly in the growth of data centers and storage infrastructure.

Related Sources

- Micron Technology, Inc. (MU) Stock Overview (Yahoo Finance)

- Assessing Micron Technology Valuation As AI Demand Drives Fully Booked HBM Capacity (Simply Wall St)

- This Under-the-Radar AI Stock Is Already Up 50% in 2026 (The Motley Fool)

- Everything you need to know about Micron’s massive Boise manufacturing expansion (Idaho News 6)