Are Micron’s record earnings the start of a new AI memory era or just the top of another brutal chip cycle?

How are Micron Earnings driving the stock today?

The latest Micron Earnings backdrop is unusually mixed for a stock that has roughly doubled over the past year. On the one hand, the company’s most recent reported quarter, fiscal Q2 2026 (ended February), showed what many on Wall Street view as peak‑cycle metrics: revenue soared 196% year over year to $23.8 billion, while non‑GAAP earnings surged 682% to $12.20 per diluted share. CEO Sanjay Mehrotra highlighted record sales across DRAM, high‑bandwidth memory (HBM), and NAND, and signaled expectations for “significant records” again in the current quarter.

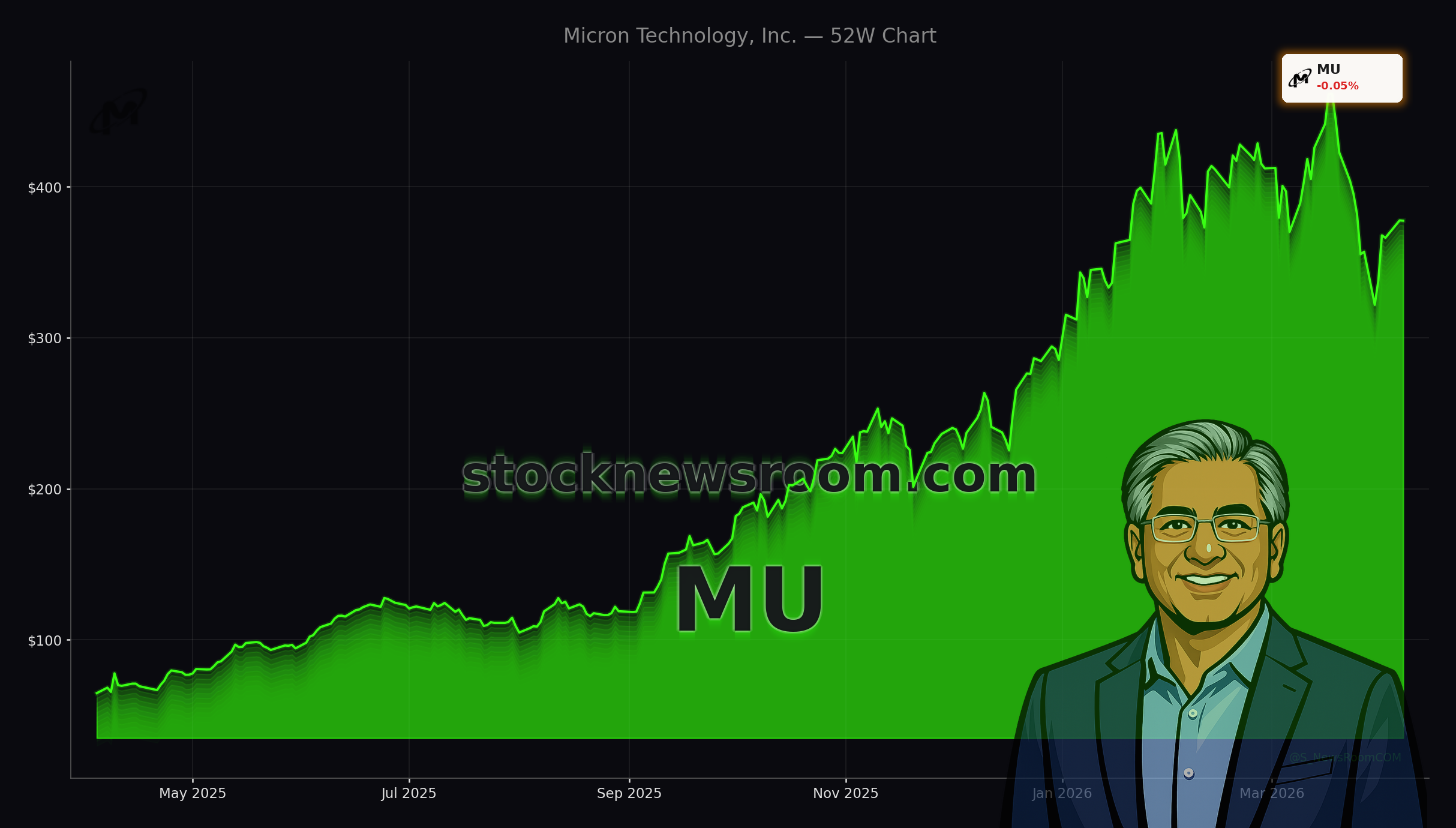

Despite those stellar Micron Earnings, MU has been under pressure. The stock closed Tuesday at $377.58, slightly below the prior close of $401.50, though pre‑market indications near $410 suggest buyers are stepping back in. The move comes after a more than 20% slide from March 17, as investors reassess how long AI‑driven pricing strength can last and how much capital Micron will need to sustain that growth.

Why are analysts split on Micron Technology now?

Analyst sentiment around Micron Earnings has turned more polarized in early April. Erste Group cut its rating on Micron from “Buy” to “Hold,” citing concerns about heavy capital expenditures in fiscal 2026 and 2027 and the long‑term sustainability of the current memory upcycle. The bank argued that rising investment needs could weigh on free cash flow just as the memory cycle may begin to normalize.

By contrast, other firms remain firmly in the bull camp. Argus recently raised its price target on Micron from $320 to $540 while maintaining a “Buy” rating, underscoring what it sees as exceptional growth powered by AI server demand. Earlier, Mizuho Securities also leaned positive on the broader memory complex, calling recent “peak memory” fears overblown and pointing to continued demand for AI infrastructure as a structural driver rather than a temporary spike.

Consensus estimates reflect that optimism. Over the last 90 days, Wall Street’s forecast for Micron’s current fiscal‑year adjusted earnings per share jumped about 70% to roughly $57.11, implying nearly sixfold growth from the prior year. Yet with Micron trading at about 16 times those adjusted earnings, the stock no longer looks cheap on a pure cyclical basis, especially if profits normalize to a slower 13% annual growth rate through fiscal 2029.

Can Micron Technology sustain the AI memory boom?

Micron’s investment case rests on its role at the heart of the AI infrastructure build‑out. The company is a key supplier of DRAM, NAND, and especially HBM, the ultra‑fast memory used alongside accelerators from players like NVIDIA. Supply of HBM remains extremely tight, and industry capacity constraints—such as limited chip‑on‑wafer‑on‑substrate throughput at Taiwan Semiconductor Manufacturing—have driven HBM pricing sharply higher.

That dynamic not only supported the recent Micron Earnings surge but also led many investors to question how long such favorable pricing can endure before the traditional memory cycle reasserts itself. History suggests that today’s shortage could eventually flip to a glut as rivals like Samsung and SK Hynix ramp capacity, pressuring margins across the sector. Recent headlines about Google’s TurboQuant compression and efficiency gains in AI models spooked memory stocks by raising the prospect that future models may require fewer chips.

However, several analysts argue that improvements in algorithmic efficiency typically expand the total addressable market rather than shrink it. If AI models become cheaper and faster to operate, more workloads move on‑chain and into the cloud, which may ultimately drive higher aggregate demand for both DRAM and NAND. That scenario would support a more durable earnings base for Micron than in prior cycles, even if current pricing is unsustainably high.

What does the New York megafab mean for Micron?

Beyond the Micron Earnings trajectory, long‑term investors are watching the company’s massive manufacturing expansion in the United States. Micron plans a multibillion‑dollar megafab project in Clay, New York, positioned as a cornerstone of domestic memory production under the broader onshoring trend. The factory is expected to create up to 50,000 jobs when fully built out, anchoring a regional ecosystem that ties into federal and state incentives.

As part of that effort, Micron recently announced about $35.5 million in community investments in Central New York, targeting housing, transportation, childcare, and education. These funds align with the Green CHIPS Community Investment Fund, which aims to deploy $500 million in total, with $250 million from Micron itself, $100 million from New York State, and $150 million from additional partners. This social‑infrastructure push is designed to ensure the workforce and regional capacity needed for the megafab to operate at scale.

For shareholders, the New York build‑out underscores why free cash flow may be pressured just as Micron Earnings are peaking. The capex burden is substantial, but if AI‑related demand proves durable, the company could emerge with a strategically advantaged, CHIPS Act‑aligned domestic footprint that competitors will find hard to match.

How does Micron compare to other tech leaders?

Micron’s latest run has occurred in the context of a broader AI hardware boom that has lifted names from NVIDIA to Samsung, while platform giants like Apple and AI‑exposed disrupters such as Tesla battle for investor attention. While Samsung just reported its own massive profit rebound on the back of AI memory demand, Micron offers US investors a purer‑play bet on DRAM, NAND, and HBM without the consumer‑electronics exposure that defines some Asian peers.

Micron also benefits from rising usage of advanced memory in edge devices, data center servers, and emerging categories like humanoid robots, where its chips are cited as key enablers of on‑device AI “brains.” For US portfolios heavily tilted toward mega‑cap platforms, adding a cyclical, high‑beta name like Micron can change the risk profile—potentially amplifying both upside in an AI acceleration scenario and downside if the memory cycle turns faster than expected.

Related Coverage

For a deeper dive into where the stock might head next, including valuation scenarios and potential catalysts, see Micron Forecast +3.8% Rally: AI Memory Boom or Pause Ahead?. If you are tracking broader AI infrastructure themes beyond chips, the recent partnership between Cloudflare and GoDaddy offers another angle on monetizing AI traffic; details are available in Cloudflare GoDaddy Partnership +2.1% Surge Shakes Up AI Traffic.

Micron Earnings now sit at the crossroads of explosive AI‑driven growth, heavy US manufacturing investments, and an inevitably cyclical memory market. For Wall Street, the key question is whether today’s record profits and ambitious New York megafab will translate into a more resilient earnings base over the next decade. The next few quarters of Micron Earnings will be crucial in showing whether this AI supercycle can outrun the classic chip downcycle, making the stock a pivotal name for growth‑oriented, risk‑tolerant investors.