Can Micron’s record-shattering AI earnings really justify a fresh sell-off in one of Wall Street’s hottest chip names?

Why do record Micron Earnings meet red on the screen?

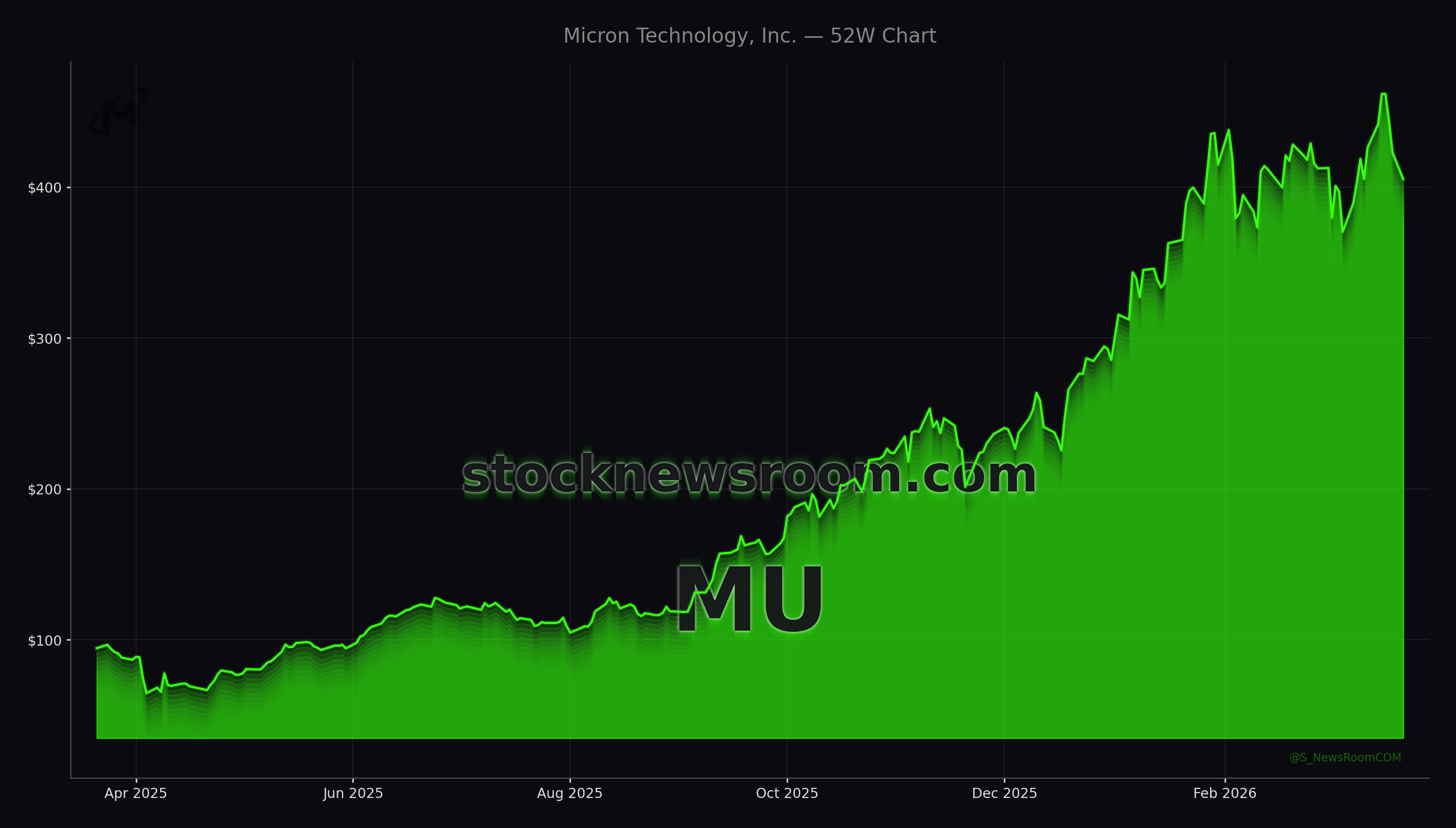

Micron Technology, Inc. has become a focal point of the AI infrastructure trade on Wall Street. After a powerful run that left MU up roughly 48% year to date before today’s pullback, the stock is giving back ground even as fundamentals accelerate. Monday’s close around $406.71, versus a prior close of $425.50, leaves the stock down about 3.8% on the day and more than 4% below recent peaks, mirroring a broader shakeout in chip and AI hardware names.

The irony: the latest Micron earnings were exceptional. One recent quarter showed revenue of $13.64 billion, up 57% year over year, with non‑GAAP EPS of $4.78 beating estimates by roughly 21%. More recently, Micron reported another blockbuster period with quarterly revenue of $24 billion, up about 195% year over year, and net income surging from $1.6 billion to $14 billion. Guidance has been equally aggressive, with management outlining a path toward record revenue, gross margin, EPS and free cash flow through fiscal 2026, anchored by AI‑driven memory demand.

Despite that backdrop, MU has now sold off more than once immediately after strong Micron earnings, reinforcing the idea that traders are selling into good news rather than chasing it.

How crucial is HBM to Micron Technology’s AI story?

The engine behind the latest Micron earnings is clear: high‑bandwidth memory (HBM). Micron is one of only a handful of suppliers capable of producing cutting‑edge HBM for AI accelerators used by customers such as NVIDIA and major cloud hyperscalers. Management has indicated that Micron’s HBM production is effectively sold out through 2026, with order books stretching into 2027, giving rare multi‑year visibility in what has traditionally been a highly cyclical memory business.

That demand is translating into premium pricing and exceptional profitability. In one recent quarter, Micron’s cloud memory business generated $5.28 billion in revenue at a 66% gross margin, while company‑wide non‑GAAP gross margin guidance has been pegged as high as 68%. Those are levels investors typically associate with high‑end logic players, not commodity memory, and they underpin the bull thesis that this AI wave is structurally different from past cycles.

For U.S. investors comparing AI infrastructure options, that puts Micron in the same strategic conversation as NVIDIA, Broadcom and other backbone suppliers to next‑gen data centers, rather than legacy PC‑DRAM vendors.

What’s spooking investors after strong Micron Earnings?

Even so, the market reaction to the latest Micron earnings shows that investors are no longer willing to overlook balance‑sheet and macro risks. One key concern is capital expenditure. Micron has outlined plans to spend around $25 billion on capex in fiscal 2026 alone, a huge commitment for a company with roughly $14.5 billion in liquidity. Bulls argue that these investments are necessary to lock in AI‑driven growth; bears warn that cash burn, execution risk and the possibility of an eventual memory down‑cycle could pressure returns.

Broader risk sentiment isn’t helping. An Iran‑related war scare and worries about Middle East supply disruptions have triggered a broad de‑risking in chip and AI infrastructure names. On Friday, multiple storage and semiconductor peers sold off sharply, and Monday’s session again saw MU diverge negatively from a rising NASDAQ 100 as geopolitical headlines and profit‑taking weighed on high‑beta winners.

Valuation plays a part as well. After a roughly 340% gain over the past year, Micron now trades around 21 times earnings, which is still modest versus some AI high‑flyers but rich compared with its own history as a cyclical memory name. That multiple assumes that HBM demand remains strong and that gross margins can stay elevated even as capacity ramps.

How does Micron stack up against other AI leaders?

From a portfolio‑construction standpoint, U.S. investors now have to decide where Micron sits in the AI stack relative to names like NVIDIA, Tesla and Apple. While Apple and Tesla lean on AI more at the application layer, Micron’s leverage is squarely in the picks‑and‑shovels layer: DRAM, NAND and HBM that power data centers, autonomous systems and edge devices.

Unlike GPU vendors that may face rapid competitive entries, the HBM market remains capacity‑constrained and technically demanding. That has allowed Micron to capture a growing share in AI‑optimized memory even as valuation‑sensitive investors debate how much of that future demand is already in the price. Factor‑based ETFs underscore this tension: for example, one large value‑tilted fund recently allowed Micron’s weight to drift to about 10% of assets, raising concentration and momentum concerns even as its overall P/E remains relatively low.

On the positive side, growth‑oriented research shops like Zacks have highlighted Micron as a candidate for outperformance, citing above‑average revenue and earnings momentum. Other buy‑the‑dip commentary has grouped Micron with quality AI infrastructure plays that might benefit once macro jitters and profit‑taking subside. While there are no fresh price‑target headlines today from bulge‑bracket firms like Goldman Sachs, Citigroup or RBC Capital, the tone of recent research has generally framed MU as a high‑beta way to express a constructive multi‑year AI view.

Related coverage on StockNewsroom

For a deeper dive into whether the latest Micron earnings mark the start of a durable AI memory super‑cycle or simply another setup for a classic semiconductor boom‑and‑bust, read “Micron Earnings Record: AI Memory Boom Meets Capex Warning”. That piece dissects Micron’s guidance, capital spending plans and the historical behavior of memory cycles in more detail.

Investors looking to broaden their AI hardware research beyond memory and GPUs should also look at Broadcom’s push into AI‑driven cybersecurity. Our recent sector piece “Broadcom Symantec CBX +4.9% Rally: AI Security Bet” explores how Broadcom is using its Symantec CBX platform to turn AI‑enhanced security into a new growth driver, offering another angle on infrastructure exposure inside tech‑heavy portfolios.

Ultimately, the latest Micron earnings confirm that AI‑driven memory demand is real, scaled and highly profitable, even if MU’s share price is currently digesting a massive run and rising capex. For long‑term investors, the key question is whether today’s pullback represents healthy consolidation in a secular winner or an early warning that expectations have run too far ahead of execution. The next set of results and updated guidance will show whether Micron can keep translating its sold‑out HBM pipeline into sustained margin strength and further upside for patient shareholders.