Is the Micron forecast still intact after a record AI quarter, a brutal sell-off and fresh fears over memory demand?

Why did Micron plunge after record earnings?

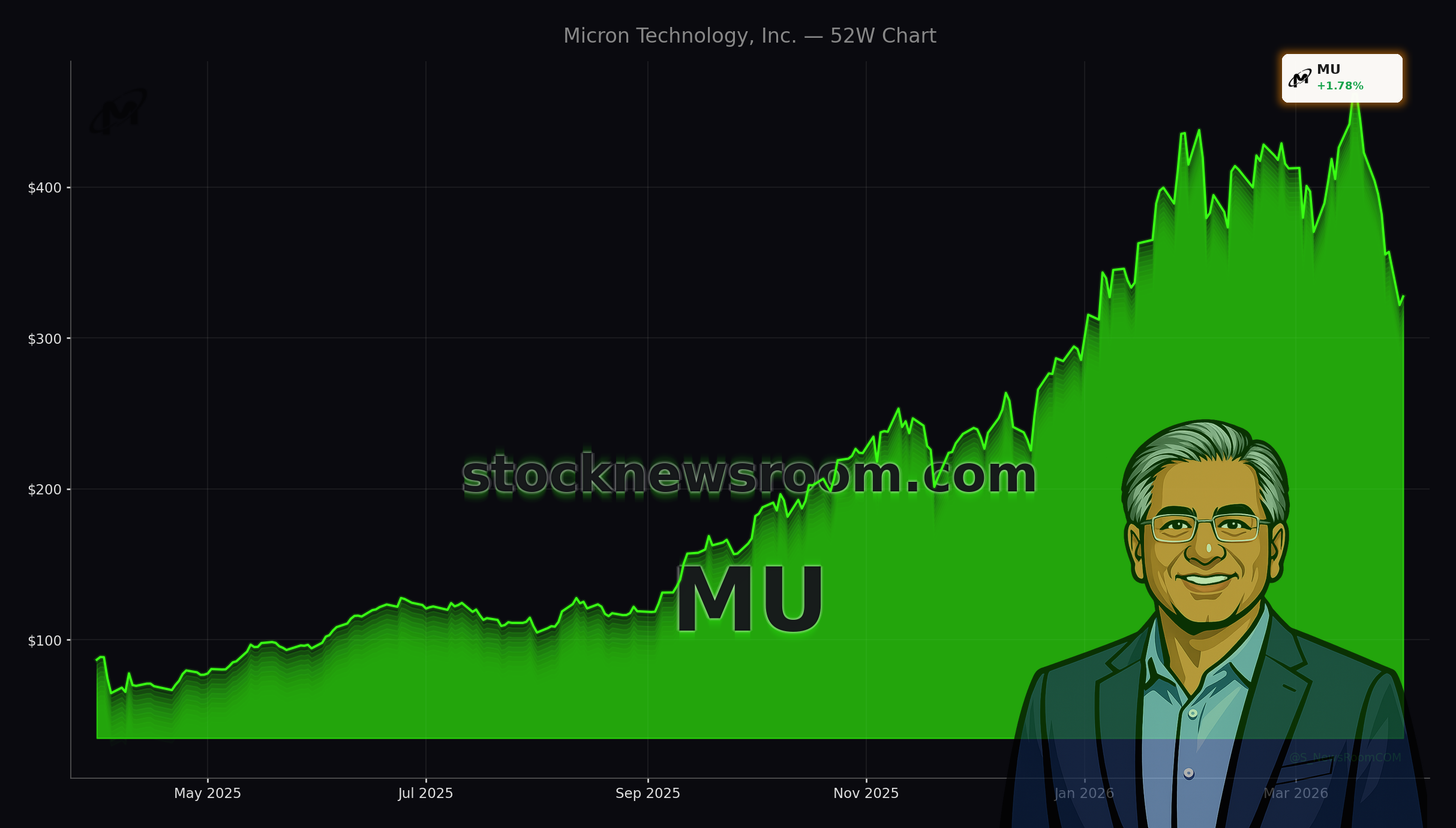

Micron’s latest numbers looked more like a fast-growing AI platform than a traditional memory name. Quarterly revenue surged to roughly $23.9 billion, up about 196% year over year, while earnings per share jumped to $12.20, beating consensus by more than a third. Management guided the next quarter to revenue of about $33.5 billion, implying that the AI-driven memory boom is still in full force. Yet the stock has been in free fall, with a one-day slide near 10% and a drawdown of roughly 20%–30% from its peak, making Micron one of the biggest March losers in the S&P 500.

The immediate pressure came from profit-taking after a 260%–plus 12‑month rally and fresh worries about memory pricing. DRAM and NAND have a long history of boom‑bust cycles, and Micron has also announced aggressive capital expenditures – more than $25 billion this fiscal year and a long‑term plan to invest up to $100 billion in New York – to expand capacity. For short‑term traders, that combination of huge gains, higher capex and macro uncertainty was enough to hit the sell button despite a still‑bullish Micron forecast from management.

How does TurboQuant change the Micron forecast?

Google’s TurboQuant compression algorithm is at the center of the current narrative shock. By shrinking key‑value (KV) caches in large language models, TurboQuant promises to make some AI inference workloads more memory‑efficient. That triggered fears that hyperscalers could do more with less high‑bandwidth memory (HBM), undermining the Micron forecast for years of structurally tight supply.

Citigroup moved quickly to address those concerns. The bank cut its Micron price target from $510 to $425 but reiterated a Buy rating, emphasizing that the recent 6% pullback in mainstream DDR5 DRAM prices, and the TurboQuant headline, do not amount to a broken investment thesis. Historically, more efficient computing has led to more total demand, not less – cheaper or better technology expands use cases, especially in semiconductors.

Morgan Stanley struck a similar tone, keeping an Overweight stance on memory stocks while stressing that there is “no indication that demand for memory or storage is going down.” The firm argues that memory remains the best way to play growth in general‑purpose and AI servers, as agentic AI tasks will require ever‑larger and faster memory pools. In other words, the Micron forecast for rising HBM and DRAM demand may get dented at the edges, but not derailed.

What are analysts really pricing into Micron?

Despite the recent turmoil, Wall Street remains broadly constructive on Micron. Out of 40‑plus covering analysts, the overwhelming majority rate the stock a Buy, with only a handful of Sells. Citigroup’s lowered $425 target still implies meaningful upside from the current ~$331 share price, and it now sits below the roughly $525 average Street target – reflecting caution on near‑term pricing while keeping a bullish medium‑term Micron forecast firmly in place.

Valuation is central to that stance. On 2027 estimates, Micron trades at a forward P/E as low as 3.5–6x, with some models assuming earnings growth of roughly 90% a year over the next five years as AI capex continues. Management says its DRAM – including HBM – and NAND capacity is sold out through at least the end of the year, with some customers only getting half to two‑thirds of what they want. That supply‑demand imbalance, plus a shift to multi‑year HBM contracts, underpins bullish expectations that Micron can keep gross margins elevated and smooth out the classic memory cycle.

Still, investors are wrestling with sequencing risk: if AI spending pauses, geopolitics flare or capex overshoots, even a robust Micron forecast could get discounted quickly, as the last few weeks have shown.

How does Micron compare with NVIDIA and Big Tech?

For diversified U.S. investors, a key question is whether to own memory directly through Micron or indirectly via broader AI leaders like NVIDIA, Apple or Tesla. Nvidia’s accelerators currently anchor the AI data‑center build‑out, and Micron is a major HBM supplier into Nvidia’s Blackwell and upcoming Rubin architectures. That makes Micron a leveraged derivative on Nvidia’s growth, but at a fraction of Nvidia’s earnings multiple.

Unlike platform giants that monetize AI via software, ads or devices, Micron’s exposure is concentrated in commodity‑like components whose pricing has historically been more volatile. On the other hand, some value investors now see Micron as one of the cheapest ways to play the AI infrastructure stack in the S&P 500, especially compared with higher‑multiple chip designers and mega‑cap platforms. If the bullish Micron forecast proves accurate and AI capex stays strong, the stock’s risk‑reward could remain attractive even after a 12‑month run‑up.

What should U.S. investors watch next?

For now, the technical setup mirrors the fundamental debate. Traders see resistance in the $350–$360 area and support in a wide $250–$280 zone, where some are waiting to add long positions if the current bounce fails. On the macro side, any easing of geopolitical tensions – particularly in the Middle East – could unlock delayed capex from cloud and enterprise customers and further validate the Micron forecast for constrained capacity into 2027.

Long‑only allocators are also monitoring how quickly new fabs ramp and how aggressively rivals like Samsung and SK hynix bring HBM capacity online. If supply catches up faster than expected, pricing power could fade earlier than the Street currently models. Conversely, if AI workloads and emerging agentic AI use cases scale in line with today’s more optimistic projections, Micron’s multi‑year contracts and massive New York investment could give it a durable competitive edge within the global memory oligopoly.

Related Coverage

For a deeper dive into how the TurboQuant debate first hit sentiment, including the initial 5.2% drop and valuation reset, see “Micron Technology AI Memory Boom: -5.2% TurboQuant Shock”, which analyzes whether that move was an overreaction or an early warning. To put Micron’s capex surge into the broader AI infrastructure race, read “Microsoft AI Investment Boom: $1B Thailand Bet Explained”, which looks at how hyperscalers’ global expansion plans are shaping demand for chips and memory across regions.

In the end, the Micron forecast still points to tight AI memory markets, robust earnings and a valuation that prices in plenty of bad news after a brutal sell‑off. For U.S. investors, the stock remains a high‑beta way to express conviction in the AI data‑center build‑out, while the next few quarters will show whether TurboQuant and rising capex are temporary distractions or real headwinds to an otherwise powerful secular story.