Is the Micron Forecast signaling an AI memory supercycle still in motion, or the first cracks in a classic chip downturn?

How fragile is Micron’s AI-driven rally?

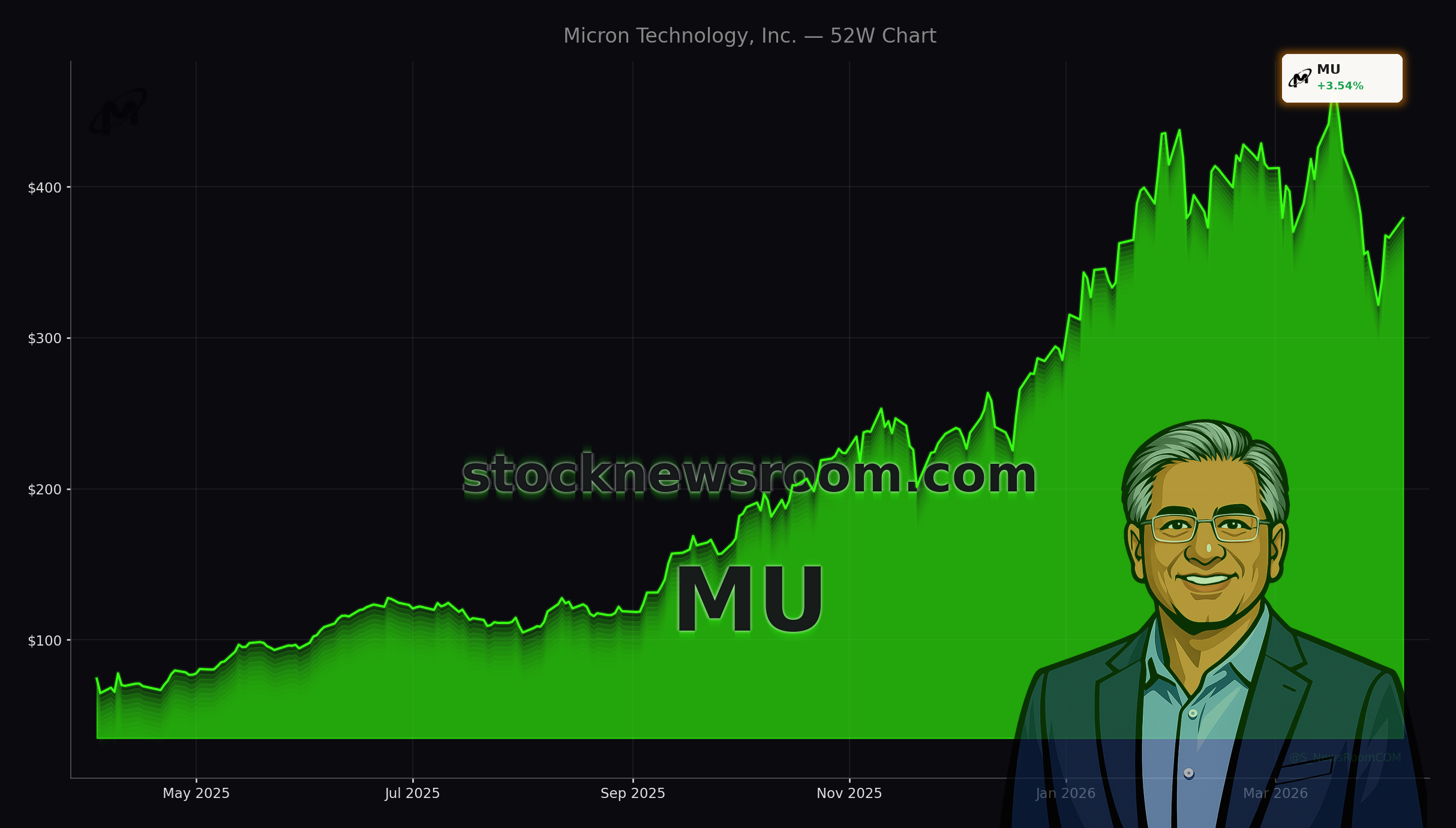

Over the past 12 months, Micron Technology, Inc. has more than quadrupled in value, fueled by a surge in demand for DRAM and NAND used in AI data centers, cloud infrastructure and high-end PCs. In its most recent quarter (ended Feb. 26), revenue soared to roughly $23.9 billion, nearly triple the prior-year period, while net income surged to about $13.8 billion. Those numbers put Micron among the fastest-growing large-cap tech names on Wall Street and have turned it into a key indirect play on the data-center expansion of leaders like NVIDIA and Apple.

Yet the strength of this rally has also raised cyclical red flags. Memory is a notoriously boom-bust industry, and some early stress signals are emerging: spot prices for mainstream DDR5 DRAM have slipped about 6% since Micron’s last earnings report, and March was one of the stock’s worst months in roughly four years. MU is still up sharply year-on-year, but the recent drawdown has forced investors to revisit their own Micron Forecast for the rest of 2026 and beyond.

What are Wall Street analysts saying about the Micron Forecast?

Despite the correction, the Street remains overwhelmingly bullish. There are roughly 47 buy ratings on Micron, six holds and no sell ratings. KeyBanc Capital Markets analyst John Venn reiterates an “Overweight” rating and recently lifted his earnings estimates, maintaining a bold $600 price target, implying substantial upside from current levels. Zacks Investment Research also highlights Micron on its Focus List, emphasizing the rare combination of powerful earnings momentum and price strength.

Citigroup remains constructive as well, keeping its Buy recommendation while trimming its price target from $510 to $425 to reflect the latest dip in DRAM spot prices. Analyst Atif Malik notes that Micron and peers are negotiating three- to five-year strategic supply agreements with hyperscale cloud customers, locking in base volumes, prepayments and quarterly pricing floors tied to market conditions. In his view, those contracts should support contract pricing even if spot markets wobble, an important pillar of the current Micron Forecast.

Does pricing power make this downturn different for Micron?

The core of today’s Micron bull case is that this memory upcycle is being driven less by inventory games and more by structural AI demand. In the last quarter, DRAM revenue rose more than 200%, driven primarily by a mid-110% jump in average selling prices (ASPs), while unit shipments increased by a more modest mid-40%. NAND showed a similar pattern, with ASPs more than doubling. That dynamic underscores Micron’s current pricing power, but also why any reversal in ASPs poses a major risk.

Mizuho’s Vijay Rakesh, who rates Micron “Outperform,” argues the roughly 20% pullback from the recent high is overdone. He contends that Micron and other memory players still retain significant pricing leverage as AI, cloud and edge-computing demand keep absorbing capacity. His Micron Forecast centers on quarterly memory-price increases that may moderate but remain positive, especially as long-term hyperscaler contracts introduce price floors and capacity prepayments. KeyBanc’s Venn similarly expects DRAM and NAND prices to keep rising at a more moderate but still robust 30%–50% pace quarter-over-quarter in the near term.

How does competition and SK Hynix’s U.S. listing risk affect Micron?

Micron is currently the only pure-play DRAM leader listed in the U.S., giving it a visibility and valuation premium over larger Korean rivals such as Samsung and SK Hynix. That premium may be tested if SK Hynix proceeds with a planned ADR listing in New York, which would offer U.S. ETFs and mutual funds another direct route into AI memory. Bloomberg has reported growing expectations of such a move, and some investors fear that a second U.S.-listed DRAM heavyweight could dilute flows into MU.

At the same time, Micron’s role as the main domestic DRAM supplier for AI infrastructure still resonates with U.S. portfolio managers focused on reshoring and supply-chain resilience. Barron’s notes that both Micron and Intel stand to benefit from persistent CPU and memory shortages, while MarketBeat highlights Micron and Seagate as prime beneficiaries of a data-center memory bottleneck that could support earnings into 2026. For investors already positioned in AI leaders like NVIDIA or high-growth names such as Tesla, Micron offers a complementary way to play the same structural theme through the memory layer of the stack.

Related Coverage

For a deeper dive into how the AI memory supercycle intersects with Google’s TurboQuant developments and what that means for the medium-term Micron Forecast, readers can explore “Micron Technology Outlook After Record Boom and TurboQuant Shock”. The analysis examines whether recent turbulence signals a peak or an acceleration in AI-driven memory demand.

Investors who want to understand the broader ecosystem around Micron’s data-center exposure can also look at “NVIDIA AI Strategy Boom: Inside the $1T Data Center Shock”. That piece outlines how NVIDIA’s aggressive AI roadmap is reshaping global compute demand, with direct implications for memory suppliers and the overall Micron Forecast over the next several years.

In the end, the Micron Forecast hinges on whether today’s AI-driven shortage morphs into a more balanced but still undersupplied market or slips back into a classic memory glut. Wall Street’s current stance remains positive, backed by robust earnings, long-term hyperscaler contracts and tight data-center capacity. For U.S. investors, the next few quarters of pricing data and contract wins will be crucial in determining whether Micron’s recent 20% correction was a buying opportunity or the first step down from a cyclical peak.