Is the Micron HBM4 Launch the start of a durable AI memory supercycle or just the last euphoric leg before margins crack?

Is Micron redefining the AI memory cycle?

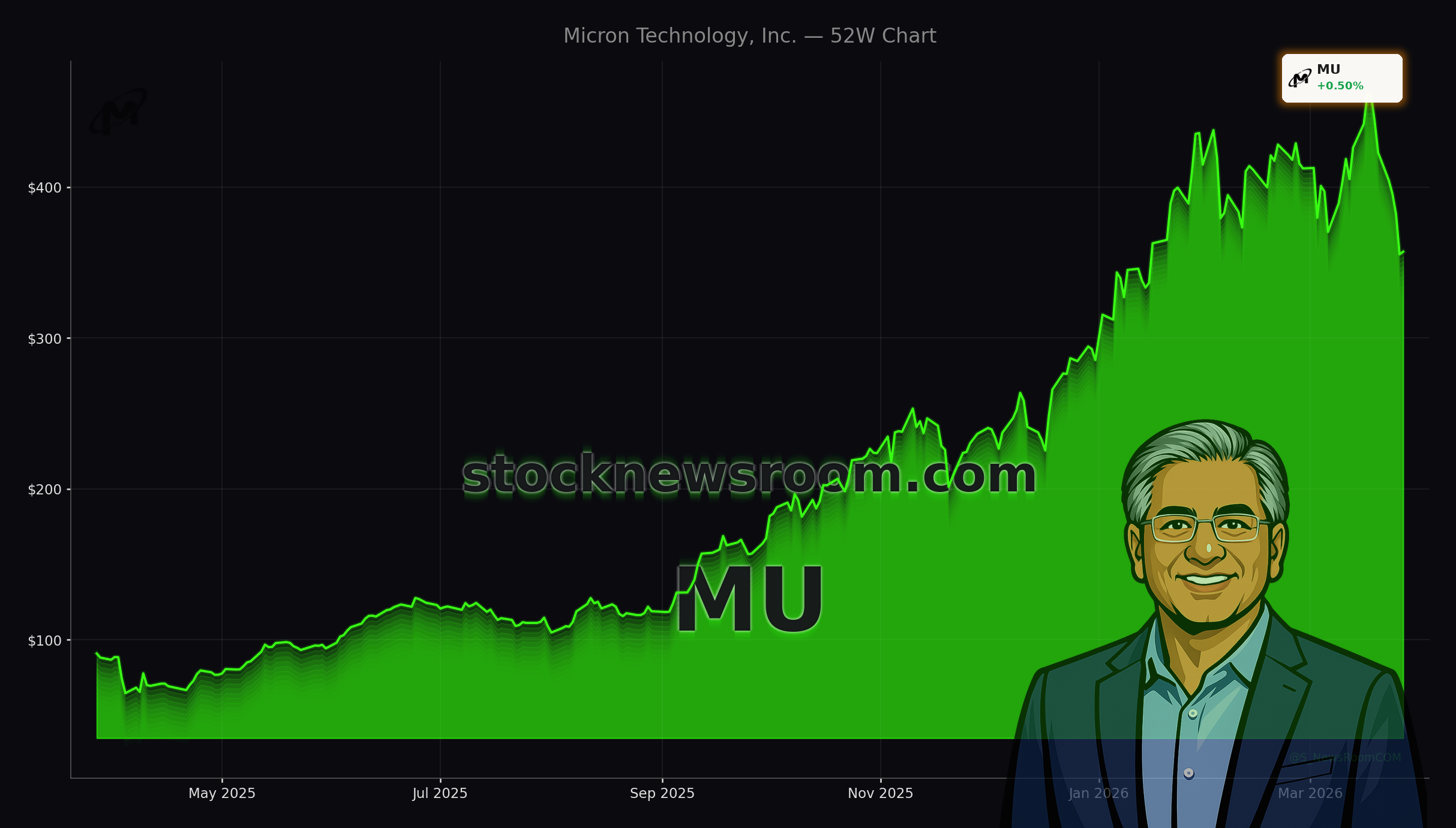

The Micron HBM4 Launch into mass production for NVIDIA’s Vera Rubin platform marks a strategic break from Micron’s past role as a technology follower. Its 36GB 12‑Hi HBM4 delivers more than double the bandwidth of HBM3 and roughly 20% better power efficiency, a critical edge as operators fight soaring AI energy bills. Management says current DRAM and NAND capacity can satisfy only about 50%–66% of customer demand, helping push gross margins from roughly 75% to around 81% in a single quarter.

That step‑function jump reflects how tight supply has become across AI accelerators, traditional servers and storage. Memory is now the bottleneck, not the GPU. Micron’s CFO Mark Murphy argues memory has been “recast as a defining strategic asset in the AI era,” signaling confidence that the Micron HBM4 Launch is more than a short‑lived spike.

How does Micron stack up against TSMC and peers?

While Taiwan Semiconductor Manufacturing has doubled over the past year, Micron’s stock has nearly quadrupled as DRAM and NAND pricing soared amid the AI build‑out. Yet Micron still trades at about 6.5x forward earnings and under 4x fiscal 2027 EPS estimates, in line with past peak‑cycle multiples. That leaves upside only if the Micron HBM4 Launch and AI demand extend the earnings peak beyond what most models assume for 2028–2029.

Competitively, Micron now ships HBM4 in lockstep with Samsung and SK Hynix instead of lagging them. Beyond HBM4, it is supplying PCIe Gen6 SSDs and advanced memory modules for Nvidia’s Rubin ecosystem, deepening a relationship that likely underpins its first‑ever five‑year strategic supply agreement. Institutional investors have noticed: firms like Wolff Wiese Magana and Q Fund Management Hong Kong recently boosted positions, even as others trimmed or rebalanced.

What risks do investors face after the Micron HBM4 Launch?

Bears argue memory remains fundamentally a commodity, and history shows that once new fabs ramp and HBM4E arrives around 2027, pricing power typically erodes. Analysts at firms including Goldman Sachs and Morgan Stanley still see Micron as a top AI beneficiary, but valuation depends on how long today’s extraordinary margins can hold before the next down‑cycle. Short‑term, AI‑driven demand, binding contracts and one of the tightest supply environments in Micron’s history support the bull case; longer term, a reversion toward mid‑cycle earnings cannot be ruled out.

Related Coverage

For a deeper dive into Micron’s AI upcycle and how it might end, see Micron AI Memory Cycle -3.4%: Record Boom Meets Crash Fears, which examines whether today’s super‑profits signal an approaching peak. Investors tracking broader AI software valuations can also read Adobe Earnings -2.5%: Can AI Growth Offset the Valuation Crash? for context on how other tech leaders are repricing in this environment.

The Micron HBM4 Launch cements Micron Technology as a core enabler of AI infrastructure rather than just a cyclical memory supplier. For U.S. portfolios, the stock is now a leveraged bet that AI demand and tight supply can keep margins near record levels longer than the market expects. The next few quarters of HBM4 ramp‑up, contract wins and pricing data will show whether Micron can sustain this new status or slip back into its old commodity pattern.