Are Micron Technology AI Earnings signaling a short-lived peak or the start of a powerful new AI memory supercycle?

Is Micron peaking or just getting started?

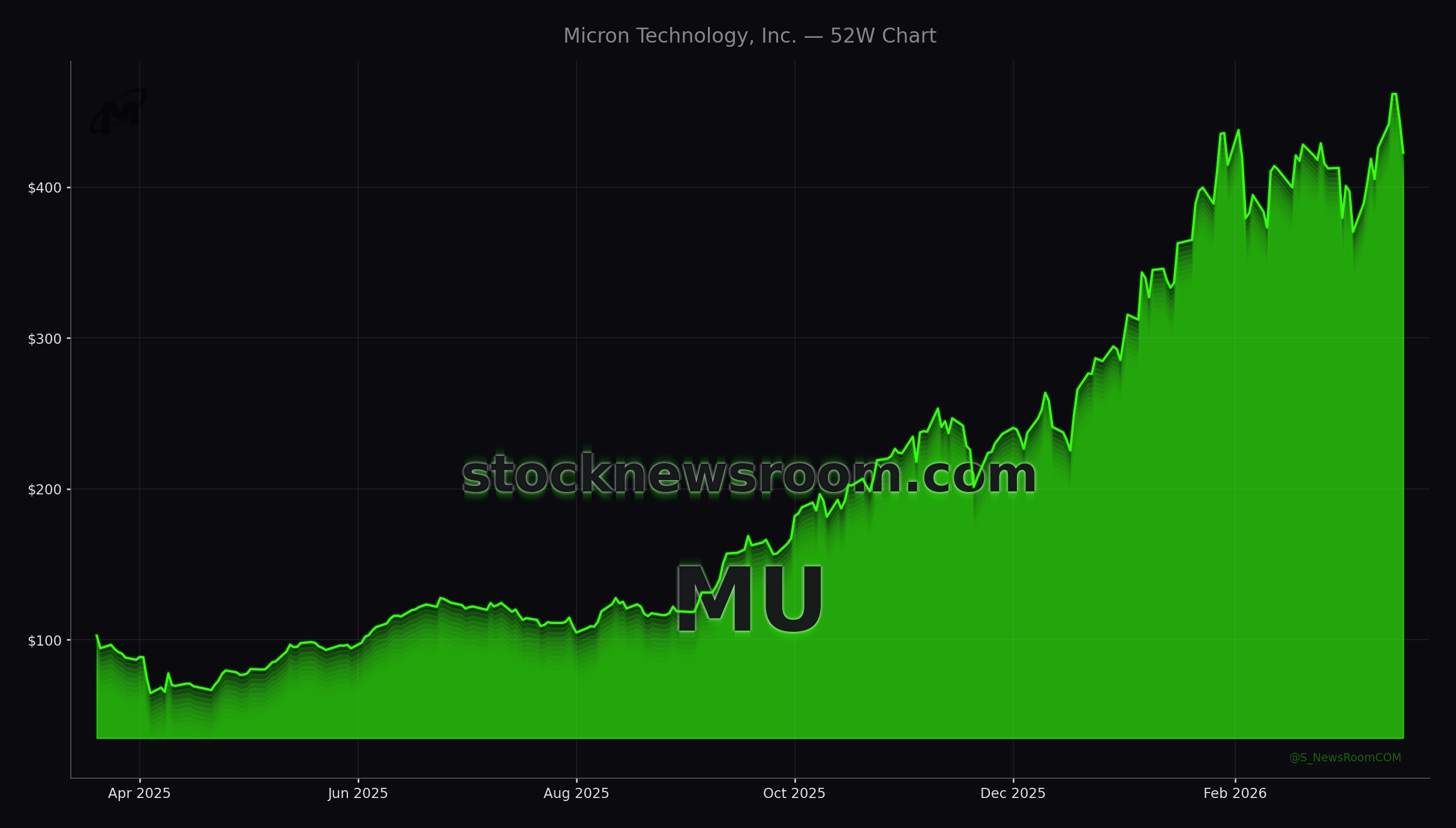

For US investors, Micron now sits at the center of the AI hardware stack, right alongside NVIDIA and other data‑center leaders in the NASDAQ and S&P 500. The latest Micron Technology AI Earnings showed one of the strongest quarters ever for a US memory maker: fiscal Q2 revenue surged from $8.05 billion a year earlier to $23.86 billion, far above Wall Street expectations around $20 billion. Adjusted earnings per share jumped from $1.56 to $12.20, underscoring how rapidly AI demand has flipped memory pricing power back to suppliers.

Micron shares, however, sold off after the print in a classic “sell‑the‑news” move, sliding more than 4% in a broader chip correction that also hit names like Seagate, Intel and equipment makers. With the stock still up triple digits over 12 months, many US portfolio managers are asking whether these Micron Technology AI Earnings represent peak conditions or a multi‑year reset higher for profitability.

How strong was Micron’s AI memory quarter?

The quarter was a clean sweep of record metrics. DRAM, which makes up nearly 80% of Micron’s revenue, more than tripled to $18.8 billion, while NAND revenue climbed more than 2.5x to about $5 billion. By end‑market, cloud memory revenue surged 163% to $7.75 billion, core data center rose 211% to $5.69 billion, mobile soared 245% to $7.71 billion, and automotive & embedded grew 162% to $2.71 billion.

Crucially for the AI story, high‑bandwidth memory (HBM) – packaged alongside GPUs in advanced accelerators – remains in severe shortage. HBM consumes roughly three times the wafer capacity of standard DRAM, tightening supply even as AI hyperscalers ramp deployments. Management has signaled that its HBM3E and upcoming HBM4 generations are essentially sold out for 2026, allowing Micron to charge premium prices and expand margins across its broader DRAM and NAND portfolio.

That dynamic pushed gross margin to 74.4%, up from 36.8% a year ago and 56% in the prior quarter, putting Micron’s profitability temporarily in the same league as NVIDIA’s GPU franchise. For many US investors, that margin profile is the clearest proof that AI memory is now as strategic – and as profitable – as compute.

What does guidance say about the AI supercycle?

Micron’s outlook keeps the bull case for a KI‑Superzyklus firmly on the table. The company guided fiscal Q3 revenue to a range of $32.75 billion to $34.25 billion, with gross margin around 81% and adjusted EPS between $18.75 and $19.55. That compares with prior analyst expectations closer to $24.3 billion in revenue and about $12 in EPS.

Beyond the single quarter, Micron Technology AI Earnings over the last year show an earnings power reset. The company generated $7.59 in EPS in fiscal 2025; in just the first six months of fiscal 2026, EPS has already reached $16.68. Some Wall Street forecasts now model EPS in the $95–$115 range by fiscal 2028–2029 if AI infrastructure spending continues at a high trajectory, implying potential share prices several times current levels if historical price‑to‑earnings multiples hold.

Yet management is also clear about the constraints: CEO Sanjay Mehrotra has stated that key customers are getting only about half to two‑thirds of the HBM supply they would like. To close that gap, Micron plans more than $25 billion in capital expenditures in fiscal 2026 alone, a bet that AI memory demand remains structurally elevated rather than purely cyclical.

How do rivals and Wall Street view the stock?

From a US tech‑sector perspective, Micron is now one of the must‑watch AI infrastructure names alongside NVIDIA, Tesla (through its in‑house AI and robotics compute build‑out) and Apple with its device‑driven demand for advanced memory. Equipment partner Applied Materials has highlighted joint work with Micron on next‑generation DRAM, HBM and packaging, reinforcing the view that memory technology is co‑evolving with AI workloads.

On Wall Street, Micron Technology AI Earnings have triggered a wave of bullish research. MarketBeat data show a consensus “Buy” rating and a string of price target hikes after the Q2 beat, with firms such as Citigroup, Goldman Sachs and Morgan Stanley pointing to Micron’s leverage to AI data centers and its still‑modest forward P/E versus projected growth. At the same time, more cautious takes – including from some analysts at The Motley Fool’s research arm – stress that much of the current windfall is driven by a supply shortage, not yet by an unassailable competitive moat.

For diversified US equity portfolios, that split view is the key risk: if HBM and DRAM capacity from rivals ramps faster than demand, pricing and margins could normalize, pulling Micron’s valuation back toward historical cycle averages.

Related Coverage

For a deeper dive into whether this boom can truly evolve into a multi‑year supercycle, readers can explore Micron Earnings Record: AI Memory Boom Meets Capex Warning, which dissects the trade‑off between today’s record margins and tomorrow’s massive spending plans. Investors interested in how AI enthusiasm is affecting valuations beyond semiconductors can also read Palantir Maven Program -3.2%: Pentagon AI Rally Warning, analyzing whether premium AI multiples in software can be justified by government contracts.

HBM has become just as integral in the AI data center build‑out as GPUs.— Sanjay Mehrotra, CEO of Micron Technology

In the end, Micron Technology AI Earnings highlight both the upside and the fragility of the current AI memory boom. The company is printing record revenue, margins and cash flow, yet is simultaneously racing to spend tens of billions to keep up with demand and ahead of competitors. For long‑term investors in US markets, Micron now stands as a core AI infrastructure play whose next few quarters will show whether this KI‑Superzyklus is a lasting secular shift or just the most profitable phase of the classic chip cycle.