Can Micron Technology Earnings keep powering the AI memory boom even as the stock suddenly reverses after record results?

How are Micron Technology Earnings reshaping the AI trade?

Micron Technology has emerged as one of the most important behind‑the‑scenes winners of the AI infrastructure build‑out. In its fiscal 2026 second quarter (ended Feb. 26), the company delivered record revenue of $23.8 billion, up 196% year over year, powered by explosive demand for HBM used alongside GPUs from leaders like NVIDIA and Advanced Micro Devices. GAAP earnings surged 756% to $12.07 per share as tight supply and AI‑driven pricing power pushed profitability to some of the highest levels in memory industry history.

The cloud segment, which includes HBM for AI data centers, generated $7.7 billion in revenue, up 163% from a year earlier. Micron’s mobile and client segment – PCs and smartphones – also posted $7.7 billion, but with even faster 245% growth as device makers added more DRAM to enable on‑device and agentic AI features. These Micron Technology Earnings underscore how AI is lifting not only data center silicon but also end‑user hardware demand for memory.

What is driving Micron’s HBM3E and HBM4 momentum?

At the heart of the story is Micron’s technical lead in HBM. Its HBM3E product offers roughly 50% more capacity than competing solutions while using about 30% less energy, an attractive proposition for hyperscale cloud and AI customers that are constrained by power and space. Micron is now ramping HBM4, which targets an additional 60% capacity increase over HBM3E and about 20% better energy efficiency.

Key partners are already baking HBM4 into their roadmaps. NVIDIA’s latest Vera Rubin GPUs, designed for state‑of‑the‑art AI training, are expected to leverage Micron’s HBM4 stacks to keep data flowing to thousands of cores without bottlenecks. That design win reinforces Micron’s role in the AI hardware stack and helps explain why the company has indicated that its HBM capacity is effectively sold out through 2026. For U.S. tech portfolios concentrated in GPU names, Micron provides a more pure‑play way to monetize the memory side of the AI build‑out.

Why did the stock fall after blowout Micron Technology Earnings?

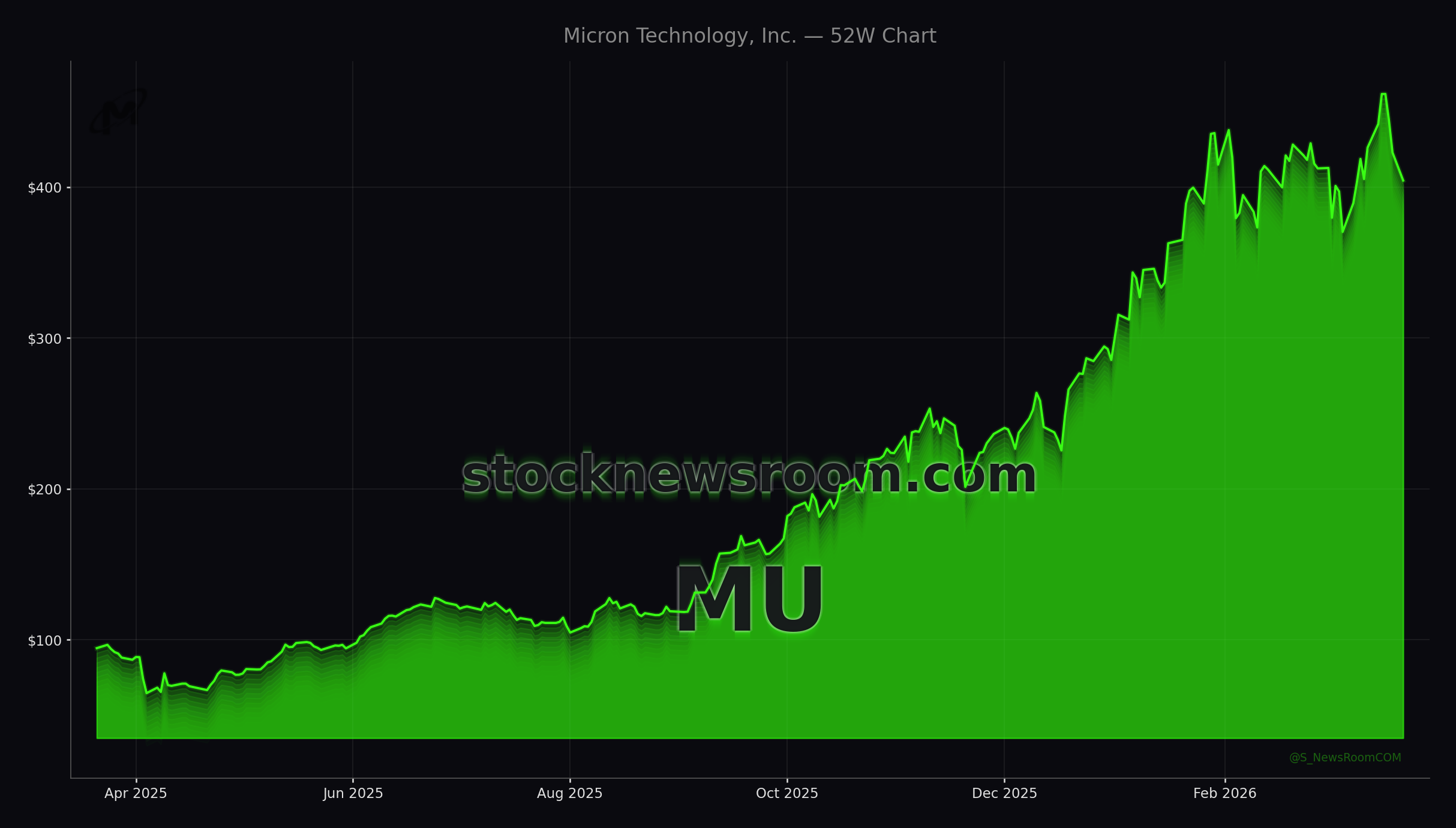

Despite these stellar Micron Technology Earnings, MU has sold off since the report. The stock is down about 13% from levels immediately before the release, and it is trading near $404 today with modest pre‑market pressure. The pullback has less to do with the quarter itself and more with what it will take to sustain this performance.

Management has outlined a sharp ramp in capital expenditures, guiding fiscal 2026 capex above $25 billion versus roughly $13.8 billion in fiscal 2025 as it builds advanced packaging capacity and aligns with leading‑edge foundries for the logic base dies in HBM4. That spending is essential to maintain leadership, but it weighs on near‑term free cash flow and raises the risk that future supply growth could erode pricing and margins. Some investors are also watching renewed aggression from Samsung and SK Hynix in HBM, a reminder that memory cycles can normalize quickly once all players spend heavily.

How do valuation and analyst views stack up?

Even after a 330% gain over the last 12 months, Micron’s valuation still looks reasonable by large‑cap tech standards. Based on a recent price near $444.27 and trailing 12‑month earnings of $21.18 per share, Micron traded at about 20.9 times earnings – below the S&P 500 at roughly 24 and the Nasdaq‑100 around 30. It also sits at a discount to Apple and GPU giant NVIDIA, which command richer multiples for arguably less direct exposure to memory‑specific upside.

Forward‑looking numbers tied to Micron Technology Earnings are even more striking. Wall Street consensus points to roughly $36.67 in EPS for fiscal 2026 and $57.31 for fiscal 2027, implying forward P/E ratios in the low‑teens and high‑single digits, respectively, at recent prices. Research shops highlighted by Benzinga continue to project upside, and bullish fundamental models on platforms like Seeking Alpha see scope for 25%–35% annualized returns through 2030 if AI memory demand stays tight. Major U.S. brokerages such as Morgan Stanley and Goldman Sachs have broadly positive stances on AI memory beneficiaries, even as they warn about the risks tied to capex intensity and competition.

What risks do Samsung and SK Hynix pose for Micron?

Competitive dynamics are front and center for investors trying to gauge the durability of the current Micron Technology Earnings power. Samsung is pursuing a vertically integrated AI strategy, designing logic, fabricating base dies on advanced nodes, and stacking its own HBM in‑house. That model could give it structural cost advantages and allow bundled deals with custom AI chip designers. SK Hynix, meanwhile, is making substantial investments in leading‑edge memory equipment, a development that supports demand for toolmakers like ASML but may also indicate a more aggressive push in HBM capacity that could pressure pricing later in the decade.

For long‑only U.S. portfolios, the upshot is clear: Micron is no longer just a cyclical DRAM name; it is a core lever on AI infrastructure. But the same forces that make the upside so compelling – unprecedented demand, multi‑year customer agreements, and massive fab expansions – also increase the stakes if the cycle turns.

Related Coverage

For a deeper dive into whether Micron’s record quarter signals a lasting super‑cycle or a classic memory peak, readers can explore Micron Earnings Record: AI Memory Boom Meets Capex Warning, which examines capex risks, competitive threats and margin sustainability in detail. Investors interested in how downstream device demand could support memory growth should also read Apple Foldable Forecast Boom: 2026 Demand Shock for iPhone, analyzing how a potential foldable upgrade cycle at Apple may intersect with the broader AI hardware refresh.

Ultimately, Micron Technology Earnings highlight how central specialized memory has become to AI, putting the stock at the crossroads of massive HBM demand and equally massive investment needs. For U.S. investors willing to tolerate volatility and monitor capex, competition from Samsung and SK Hynix, and the broader AI spending cycle, Micron remains one of the most direct – and still reasonably valued – ways to participate in the next phase of the AI infrastructure boom.