Are Micron Technology Earnings signaling the start of a lasting AI memory supercycle or the peak before another brutal chip downturn?

How did Micron Technology Earnings shock Wall Street?

Micron Technology posted a fiscal second quarter that can only be described as historic. Revenue soared to roughly $23.9 billion, up about 196% year over year and 75% sequentially, driven primarily by demand for high‑bandwidth memory (HBM) and DRAM tied to AI data centers. Adjusted earnings per share jumped from roughly $1.41 a year ago to around $12.20, while adjusted free cash flow climbed to $6.9 billion from just $857 million in the prior‑year period.

Gross margin exploded to roughly 74%, reflecting tight supply, aggressive pricing and a shift toward higher‑value AI products. Management guided for another record quarter ahead, with fiscal Q3 revenue targeted at about $33.5 billion and earnings per share expected to climb toward the high‑teens. CEO Sanjay Mehrotra emphasized that Micron is still only able to serve roughly two‑thirds of the medium‑term demand of some key customers, underlining just how constrained premium AI memory remains in 2026.

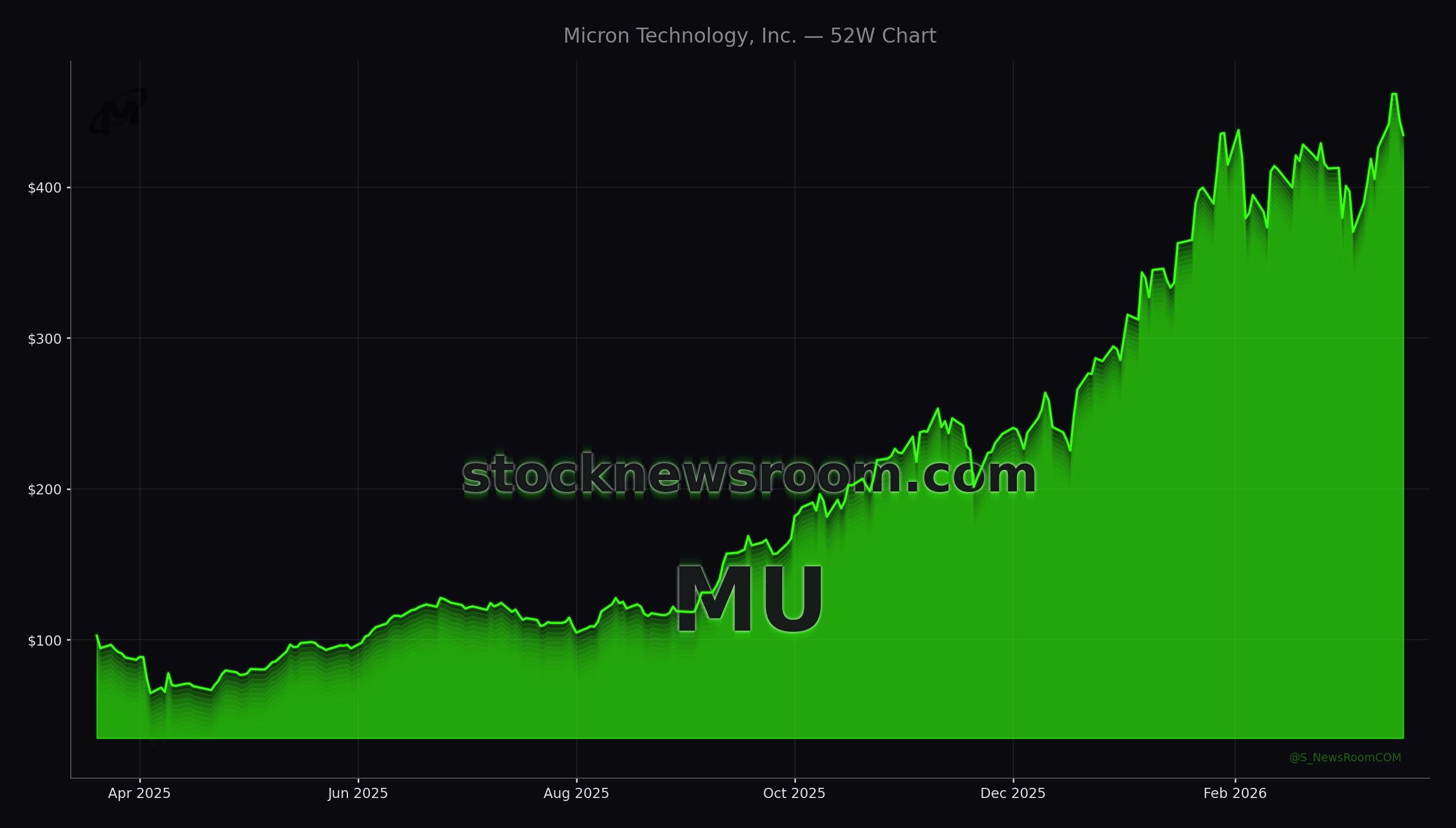

Yet despite these blockbuster Micron Technology Earnings, shares fell roughly 3%–4% after the report and are trading about 1.6% lower today at $437.12, as traders lock in gains after a more than 300% 12‑month rally and focus on what could go wrong in 2027 and beyond.

Why are investors nervous about record margins and capex?

The main concern after Micron Technology Earnings is that gross margins may be near a cyclical peak. With non‑GAAP gross margin in the high‑60s to mid‑70s percent range and AI memory sold out for years at premium prices, skeptics worry that any future capacity additions from Micron, Samsung and SK Hynix could tip the market into oversupply and pressure prices.

Micron reinforced those worries by lifting its full‑year capital expenditure forecast to about $25 billion, well above the roughly $22.4 billion many on Wall Street had penciled in. Management also flagged a “meaningful step‑up” in 2027 capex to expand HBM and DRAM capacity, including more than $10 billion year‑over‑year in construction‑related investments as it builds new fabs in the US and Asia.

These spending plans are strategically aimed at locking in Micron’s role as the only US‑based scaled memory producer for AI infrastructure, a key consideration for hyperscalers and government customers focused on supply‑chain security. But they also raise the classic semiconductor question: is today’s shortage sowing the seeds of tomorrow’s glut?

How do Micron Technology Earnings fit the AI supercycle story?

Analysts covering Micron Technology increasingly describe the current phase as a structural “memory supercycle” rather than a simple post‑downturn rebound. AI servers from NVIDIA’s GPU platforms to x86 and custom accelerators are far more memory‑intensive than traditional workloads, and architectures are shifting to pack in more HBM and high‑performance DRAM per compute node.

Mehrotra has argued that AI has “fundamentally recast memory as a defining strategic asset in the AI era” rather than a pure commodity. That thesis is supported by multi‑year supply agreements — including a recent five‑year deal — that lock in volume and pricing, and by capacity that is effectively sold out through at least 2027 for some HBM products. With 2026 set up as a seller’s market, no major new capacity is expected to hit until 2027, giving Micron unusual pricing power for a memory cycle.

On the valuation side, TD Cowen’s Krish Sankar raised his price target from $435 to $550 and boosted his 2027 EPS estimate from $90 to $110, arguing that even a conservative 5x multiple on that earnings power supports upside from current levels. MarketWatch has likewise highlighted that Micron’s stock screens as “spectacularly cheap” on forward earnings and free‑cash‑flow metrics given its growth trajectory and AI leverage.

What are analysts saying about Micron versus AI peers?

Wall Street sentiment remains broadly positive despite the post‑earnings pullback. TipRanks data cited by The Globe and Mail shows a Strong Buy consensus on Micron, including a fresh Buy rating from Rosenblatt Securities. Multiple firms have raised price targets following the latest Micron Technology Earnings, with bullish analysts pointing to the company’s unique US manufacturing footprint, tight AI supply and rising dividend — recently increased by 30% — as drivers of long‑term total return.

Compared with broader AI plays, Micron trades at a steep discount. While NVIDIA commands a premium multiple on its GPU dominance and hyperscale exposure, Micron changes hands at an earnings multiple in the high single digits based on ramping forward EPS. That discount persists even as Micron’s revenue growth briefly outpaces many high‑profile AI beneficiaries, and as its HBM and DRAM are mission‑critical inputs for AI systems sold by names such as Apple and major cloud providers.

From a macro perspective, some investors are trimming exposure to high‑beta tech due to the Middle East conflict and elevated energy prices. Commentary from value‑focused outlets notes that Micron, together with energy majors like Exxon Mobil, could help hedge some geopolitical risks thanks to tangible assets, strong cash generation and, in Micron’s case, a central role in digital infrastructure.

Related Coverage

For a deeper dive into whether the latest Micron Technology Earnings mark the start of a durable AI memory supercycle or a potential capex‑driven trap, readers can explore “Micron Earnings Record: AI Memory Boom Meets Capex Warning”, which dissects margin dynamics, capacity plans and long‑term demand scenarios. Investors looking beyond pure memory plays may also want to read “Dell AI Servers Surge +5.7% as Supermicro Stumbles”, examining how Dell’s server strategy is emerging as an alternative way to gain exposure to the same AI infrastructure wave that is powering Micron’s growth.

AI has not just increased demand for memory; it has fundamentally recast memory as a defining strategic asset in the AI era.— Sanjay Mehrotra, CEO of Micron Technology

In summary, Micron Technology Earnings underscore how central AI memory has become to the next leg of the tech cycle, even as record margins and a $25 billion capex plan revive old fears of oversupply. For diversified US investors, Micron now offers a rare mix of hyper‑growth, strong cash flow and a still‑reasonable valuation, but with classic cyclical risks that must be managed carefully. The next few quarters will show whether management can thread the needle between maximizing today’s AI windfall and avoiding tomorrow’s glut, making upcoming Micron Technology Earnings a key event on every Wall Street calendar.