Is Micron’s AI memory super-cycle just beginning, or is the market already pricing in a painful downshift?

Micron Technology Forecast: What is the market pricing in?

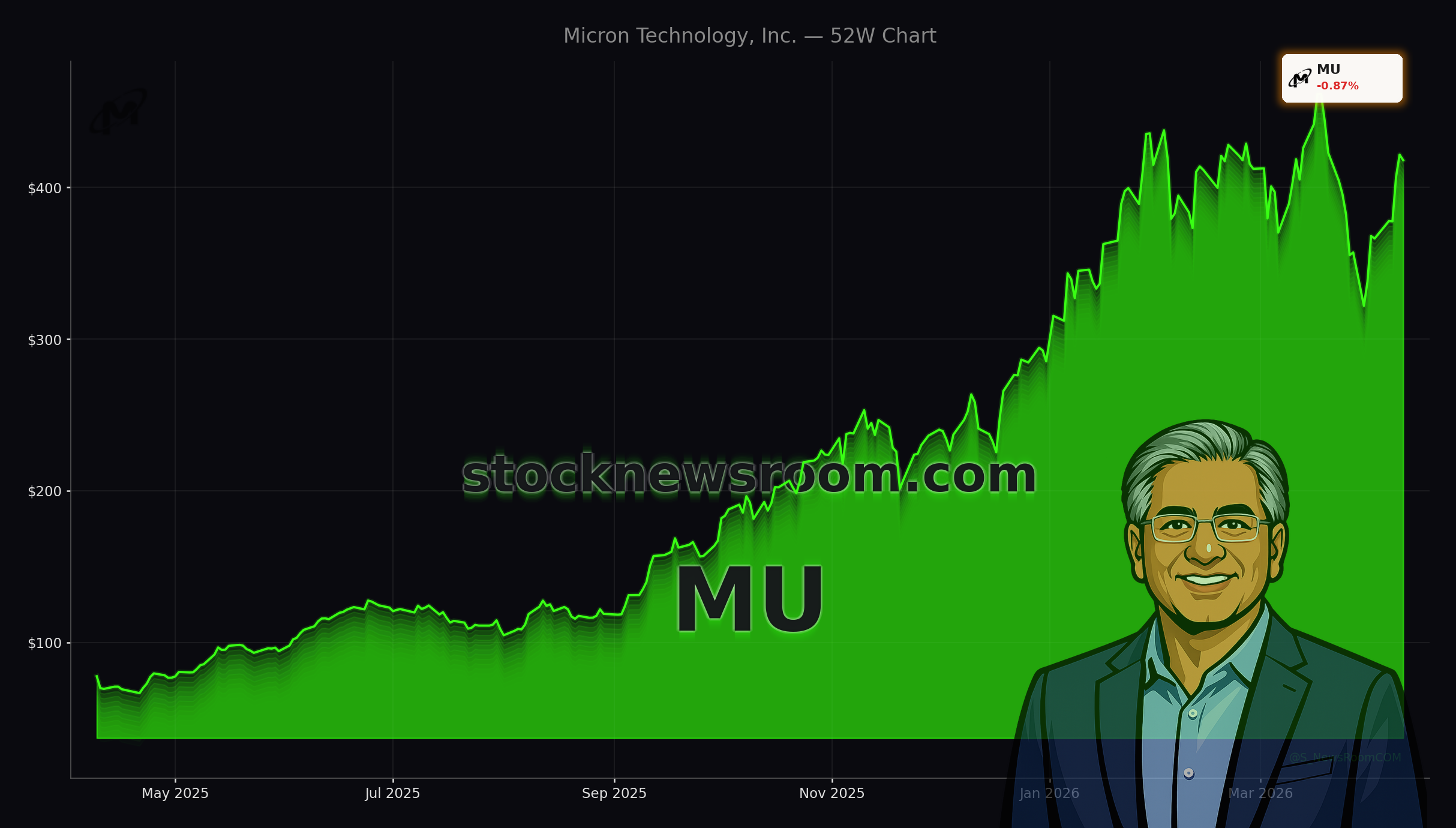

Micron Technology, Inc. has become one of the most polarizing names on the NASDAQ. The stock has climbed roughly 485% year over year, from the low‑$60s to above $400, and still trades about 10–20% below its 52‑week high near $471. Yet its forward P/E sits near 6x, a level usually reserved for deep‑cyclical names, not for companies guiding to record revenue and margins.

In fiscal Q1 2026 Micron delivered non‑GAAP EPS of $4.78 versus expectations of $3.94, on revenue of $13.64 billion, up 56.7% year over year. Guidance for Q2 FY26 is even more aggressive: $18.7 billion in revenue and non‑GAAP EPS of $8.42 with gross margin expected around 68%. Those numbers underpin the bullish Micron Technology Forecast that sees AI‑driven demand reshaping what used to be a classic commodity memory cycle.

However, a quantitative model from 24/7 Wall St. projects a 12‑month price target of $318.89, implying meaningful downside from recent levels and assigning a 90% probability that the stock trades below current prices in its horizon. That bearish Micron Technology Forecast leans heavily on Micron’s low forward multiple, high beta of about 1.6, and signs of momentum fatigue after the parabolic move.

Is Micron Technology or the bears right on AI memory?

Bulls argue that Micron is not just a cyclical DRAM and NAND producer anymore but a core beneficiary of the AI compute stack. CEO Sanjay Mehrotra has highlighted that Micron’s entire 2026 HBM supply, including next‑gen HBM4, is already contracted, with order visibility stretching into 2027. He also projects the HBM total addressable market to grow from roughly $35 billion in 2025 to about $100 billion in 2028, a ~40% CAGR. That backdrop supports aggressive upside scenarios, including 1‑year bull‑case targets around $495 and analyst consensus near $525.

UBS recently raised its Micron price target from $510 to $535 while reiterating a Buy rating, citing a memory “super‑cycle” in DRAM, NAND and especially HBM for AI workloads. UBS models EPS of about $135 in 2027 and $120 in 2028, well ahead of many on Wall Street, and sees long‑term supply agreements making earnings less volatile than in past cycles. Trefis likewise argues Micron offers better growth and value than Analog Devices, pointing to stronger revenue and operating income trends coupled with a lower valuation multiple.

On the other side, skeptics note that memory has never escaped cyclicality for long. The low forward P/E and persistent net insider selling – with multiple executives selling shares between roughly $388 and $431 – suggest management and institutions are hedging against a potential downshift once today’s tight supply loosens.

How does Micron compare with NVIDIA and other AI leaders?

For US investors, the Micron Technology Forecast must be seen in the context of the broader AI hardware trade led by names like NVIDIA. While NVIDIA’s data‑center GPUs capture most headlines, Micron’s HBM, DDR5 and LPDDR solutions address a different but increasingly critical bottleneck: memory bandwidth and capacity across training, inference and edge deployments.

Unlike GPU vendors, Micron sits deeper in the supply chain and competes directly with Samsung and SK hynix. That competitive intensity is a key risk: both Asian rivals are expanding HBM capacity aggressively, and a future oversupply could compress the 60%+ gross margins Micron is currently guiding for. Still, as long as AI data‑center capex remains elevated and edge use cases like autonomous vehicles or smart manufacturing scale, Micron’s diversified portfolio positions it as a core beneficiary alongside ecosystem players such as Apple in devices and hyperscalers building custom accelerators.

Applied Materials and Lam Research, which supply critical wafer‑fab equipment to Micron and its peers, are also signaling confidence in sustained AI‑related demand. Applied Materials has highlighted strong DRAM‑related tool demand tied to transitions to advanced nodes, while Lam Research has cited robust AI‑driven orders despite some margin concerns. That upstream strength indirectly supports the bullish case that the AI memory cycle still has legs.

Micron, CapEx and the path to 2030

Looking further out, some long‑range models envision Micron’s earnings compounding 20–30% annually into the early 2030s as AI inference and edge workloads proliferate. In these scenarios, Micron’s market cap could potentially approach multi‑trillion‑dollar territory if its forward P/E rerates toward 15–20x, in line with leading AI chip designers. The Micron Technology Forecast in that camp sees today’s fears about cyclicality as outdated in the face of structural AI demand.

To capture that upside, Micron is leaning into heavy investment. Management has lifted FY26 capex guidance to roughly $20 billion, up from $18 billion, to fund new fabs and advanced process nodes. Q1 FY26 free cash flow of $3.9 billion is solid but well below that capex pace, meaning investors must accept a period of intense reinvestment and potentially choppy near‑term cash returns. With the stock’s beta above 1.6, any NASDAQ or S&P 500 correction is likely to hit Micron disproportionately hard.

For now, Wall Street remains overwhelmingly positive: roughly 38 Buy and 10 Strong Buy ratings have been reported, with no formal Sell calls, and institutions like UBS continue to move targets higher rather than lower. At the same time, more defensive vehicles such as structured notes from JPMorgan Chase linked to Micron share performance show that demand for yield‑enhancing, risk‑managed exposure is rising as volatility expectations increase.

Related Coverage

Investors looking for more context on the durability of Micron’s current run can dive deeper into record results and guidance in Micron Earnings Record: Can the AI Memory Boom Last?, which examines whether recent quarters mark a new era or just another peak in a familiar cycle. For a broader AI hardware lens, NVIDIA AI Strategy +2.6%: Can the Data Center Boom Last? analyzes how NVIDIA’s data‑center ambitions intersect with power constraints, competition and regulation – key forces that will also influence long‑term memory demand.

In sum, the Micron Technology Forecast sits at the crossroads of extraordinary AI‑driven growth and classic semiconductor cyclicality. For long‑term US investors, the stock offers rare exposure to the memory side of the AI super‑cycle, but position sizing and risk tolerance are crucial as volatility and valuation debates intensify ahead of the next earnings and into 2030.