Is the Micron Technology Outlook broken by Google’s TurboQuant shock, or did the AI memory supercycle just get even bigger?

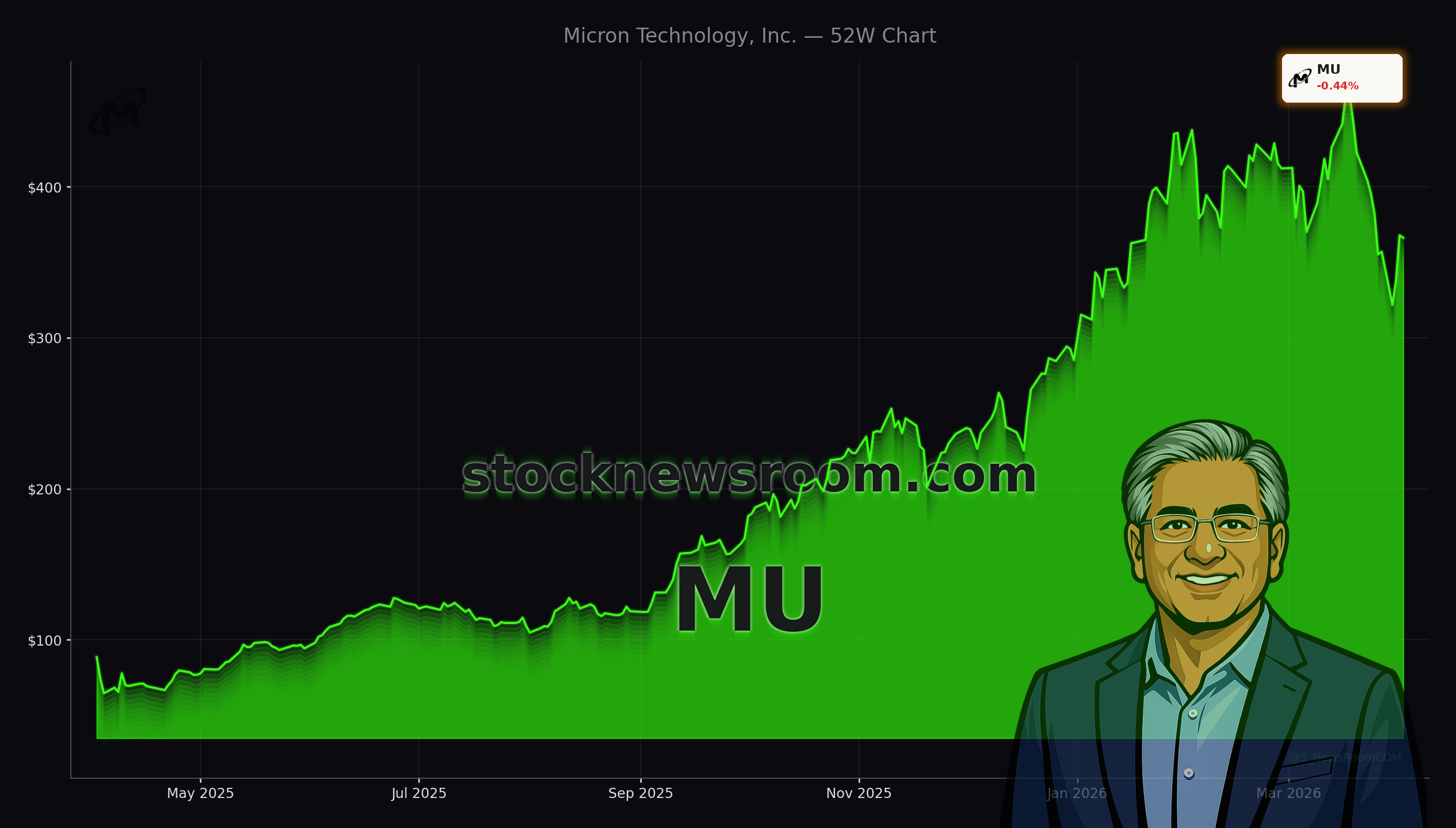

Why did Micron plunge after record results?

Micron’s March correction came immediately after some of the strongest numbers the memory industry has ever seen. For its fiscal Q2 2026 (ended Feb. 26), the company reported revenue of $23.9 billion, up 196% year over year and 75% sequentially. Adjusted EPS surged to $12.20, a 682% jump, as gross margin more than doubled to 74.4% from 36.8% a year earlier. Those figures crushed Wall Street expectations of roughly $20 billion in revenue and $9.31 in EPS and reflected extreme tightness in high‑bandwidth memory (HBM) and other AI‑critical products.

Yet shares were “taken to the woodshed” in late March, falling more than 18% during the month and nearly 30% from their high. The sell‑off was driven by fears that the pricing peak is in, that Micron’s heavy investment plans will compress free cash flow, and that new AI efficiency technologies could structurally cut demand for memory. With MU now down modestly today at $366.24 (-0.44%), the Micron Technology Outlook is being reset from perfection to skepticism.

How serious is the Google TurboQuant threat?

The sharpest blow to sentiment came from Alphabet’s Google unveiling its TurboQuant algorithm on March 24. The technique applies advanced quantization to large language models and vector search, enabling memory compression of at least 6x and up to an 8x speedup with no accuracy loss. In theory, this could reduce the physical memory needed to run cutting‑edge AI models by roughly 83%, directly challenging a key bottleneck that had been driving windfall profits for Micron and GPU leaders like NVIDIA.

In the short term, investors fear that hyperscalers could need fewer DRAM and NAND units per AI workload, particularly pressuring segments like NAND that account for about 21% of Micron’s revenue. That fear was strong enough to break the stock’s momentum even after record earnings. However, there are trade‑offs: early technical commentary points to potential downsides for effective latency and power consumption at the system level, suggesting that TurboQuant may be best suited for certain workloads rather than an across‑the‑board replacement for today’s high‑memory architectures.

Importantly for the Micron Technology Outlook, a number of strategists have invoked Jevons Paradox: when a resource becomes more efficient and cheaper to use, total consumption often rises. If TurboQuant makes AI inference radically cheaper, enterprises may scale up model sizes, usage intensity and the number of deployed applications. In that scenario, total HBM and DRAM demand could still grow rapidly even if memory per model instance falls.

Micron Technology Outlook: is AI memory still a supercycle?

Despite the recent shock, Micron’s own guidance and long‑term framing remain aggressively bullish. Management expects the HBM market to expand from around $35 billion in 2025 to $100 billion by 2028, implying a multi‑year compound growth runway even as capacity ramps. The company has signaled that supply‑demand conditions in AI‑related memory are likely to stay tight at least into calendar 2027, supporting elevated margins relative to prior cycles.

This backdrop underpins speculation that Micron could eventually join trillion‑dollar heavyweights like Apple and semiconductor peers such as NVIDIA and Taiwan Semiconductor. With a current market cap near $410 billion and a forward P/E under 7, bulls argue that consensus still underestimates the durability of AI‑driven earnings. A key pillar of the Micron Technology Outlook is the notion that AI has raised the floor of the memory cycle: even when pricing normalizes, data center, edge AI and emerging categories like humanoid robots — where investors see Micron as a critical future supplier to platforms such as Tesla’s robotics efforts — may prevent a return to the deep busts seen in earlier decades.

What is Wall Street saying now?

Analyst opinion has begun to diverge as the stock whipsaws. Erste Group recently downgraded Micron from Buy to Hold, warning that the company’s “high investments” to expand production could weigh on free cash flow and add risk if AI demand disappoints. That more cautious stance contrasts with a still‑bullish broader sell‑side consensus: the average analyst price target sits around $547.12, roughly 50%–70% above the current share price, and the majority of major U.S. brokers continue to rate the stock as a Buy or Strong Buy.

Valuation is central to that optimism. Even if Micron’s extraordinary 74.4% gross margin and 67.6% operating margin retreat as more capacity hits the market, a forward P/E near 6–7 suggests that a sizeable margin reset is already priced in. Firms including Cantor Fitzgerald highlight the potential for “very aggressive” share buybacks beginning in December once CHIPS Act‑related restrictions expire, positioning Micron to retire meaningful equity at what bulls see as discounted levels. For U.S. investors benchmarked against the NASDAQ and S&P 500, that combination of low multiple, high current profitability and structural AI demand keeps the Micron Technology Outlook compelling despite near‑term volatility.

How does Micron fit in the broader AI arms race?

Micron’s trajectory is tightly bound to hyperscaler capex and the broader AI infrastructure build‑out. Data center spending from mega‑caps like Microsoft, Alphabet and Meta is exploding, with Microsoft recently shocking the market by outlining a roughly $64 billion AI capex run‑rate for Azure. As compute clusters scale, each incremental GPU or custom accelerator typically requires more high‑bandwidth memory capacity, sustaining demand for Micron’s HBM and advanced DRAM even as efficiency improvements roll out.

Memory also sits at the heart of emerging AI applications beyond cloud data centers. Automotive and robotics platforms, including next‑generation driver‑assistance systems and humanoid robots, are memory‑intensive and latency‑sensitive, aligning with Micron’s strengths. If these markets develop at scale later this decade, they could extend the AI memory cycle well beyond the current hyperscaler build‑out and reinforce the positive Micron Technology Outlook that long‑term bulls are betting on.

Related Coverage

For a deeper dive into Micron’s capital allocation and balance‑sheet strategy, including its latest repurchase moves, readers can review Micron Tender Offer +9.1% Surge as AI Cash Flows Build, which examines whether the company’s tender offer is simple housekeeping or a high‑conviction bet on an extended AI memory supercycle. To understand the demand side of Micron’s equation, especially hyperscaler appetite for AI infrastructure, see Microsoft AI Strategy Boom: $64B Capex Shock for Azure, which details how Microsoft’s massive AI investments could sustain elevated memory and HBM demand for years.

The step-up in our results and outlook are the outcome of an increase in memory demand driven by AI, structural supply constraints, and Micron’s strong execution across the board.— Sanjay Mehrotra, CEO of Micron Technology, Inc.

In sum, the Micron Technology Outlook has shifted from unbridled optimism to a more complex, debate‑driven story where TurboQuant, capex risk and cycle fears clash with record earnings and a still‑explosive AI roadmap. For U.S. investors willing to stomach volatility, Micron remains a leveraged play on whether AI infrastructure spending and memory intensity stay higher for longer. The next few quarters of pricing data, hyperscaler orders and buyback activity will be crucial in deciding whether today’s pullback marks a buying opportunity or the start of a longer consolidation.